Value Chain Gang

Comparing card and digital wallet value chains

In the late 1990s, at an offsite for the banking consulting practice where I worked, we were assessing future banking architectures. “mmm…, the mainframe” concluded the managing partner, famed for his shrewd wit and one-liners, “it’s dying but growing”.

The same can be said today of card payments.

Card payments achieved mass adoption in the 1960s and continue to grow strongly. Visa for example, processed 234bn card transactions globally in 2024, up 10% on 2023, valued at $13trn, up 7%1. Mastercard processed 159bn card transactions valued at $9trn in 2024, each up 11% on 20232. The ECB3 reported card payments within the euro area increased by 10% to 40 billion in the first half of 2024, compared with the first half of 2023, with a total value of €1.5 trillion, up 7%. Even in China, where digital wallets dominate, consumer card payments may have declined 2% in value at RMB134trn in 2024 but were up 16% by volume at 357bn payments4.

Card payments are big, very big and are growing still. However, it is also evident that card payments have meaningful competition. As described in previous articles Account-to-Account (A2A) real-time payments through digital wallets are in the ascendancy and outpacing card payments in many regions. Over time, it is inevitable that this type of payment will overtake card payments everywhere, as it has done already in countries such as Brazil, China and India.

Comparisons between card payments and A2A digital wallet payments are made usually in terms of cost and UX. However, examination of their value chains goes a long way in explaining why A2A digital wallet payments are superior to card payments, including card payments made in digital wallets such as Apple Pay.

Payment Value Chains

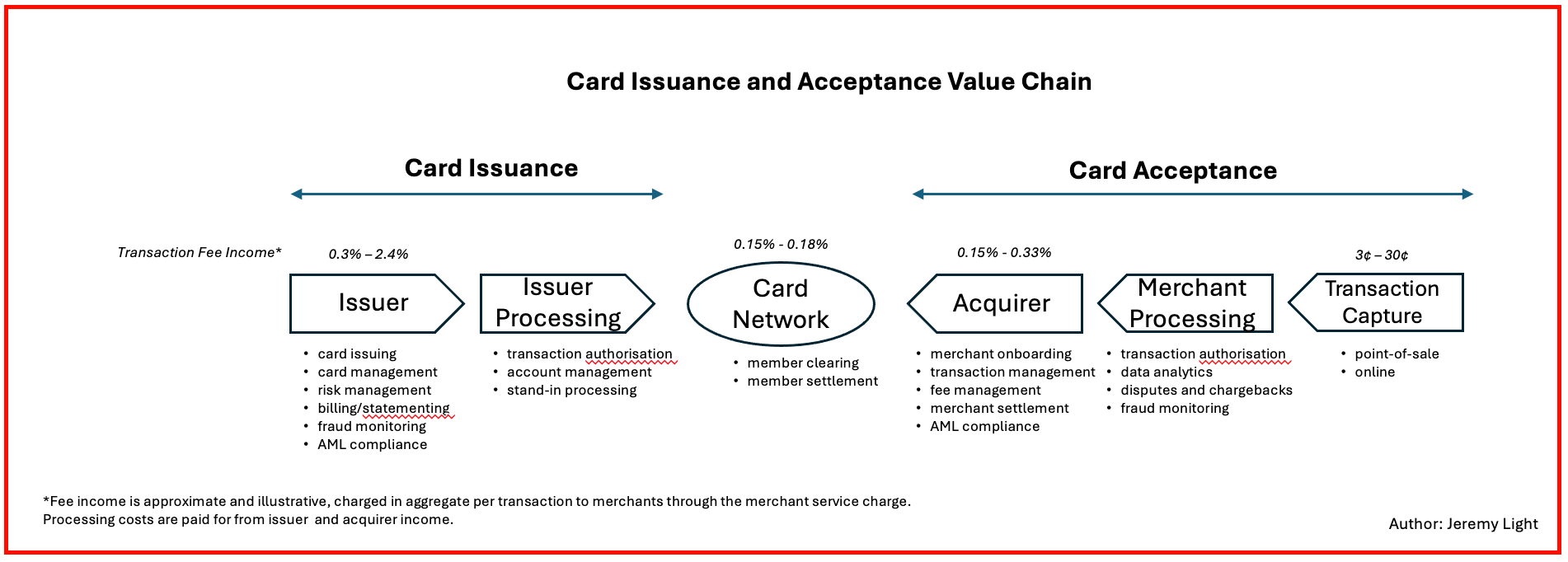

Figure 1 shows the cards value chain, very familiar to those in the cards industry. Its key feature is the separation between card issuance and card acceptance. This separation has allowed cards to be issued and accepted at scale, globally. It solved the connectivity problem that existed before the internet age between consumer and merchant, by using paper vouchers at point-of-sale and manual card authorisations made over the phone.

It has led to an ecosystem of businesses – card issuers (bank and non-bank), issuer processors, technology providers, independent service providers, merchant acquirers, merchant processors, point-of-sale terminal providers, independent sales organisations, online payment gateways and various other suppliers to the industry.

Figure 1 – Card Value Chain

Over the decades, the card ecosystem has evolved, with ecommerce adding online payment gateways and technology enabling new types of ecosystem players such as non-bank merchant processors (e.g. Adyen), Fintechs (e.g. Gocardless) and payment facilitators (e.g. Stripe).

However, the separation has drawbacks:

- the multiple organisations in a card payment result in high end-to-end costs

- connectivity through paper vouchers and phone authorisations has moved to electronic connectivity using multiple message types. These replace the paper and manual flows between merchants and issuers but each message type adds complexity and cost. Seemingly, there are only two message types – authorisation and settlement but in reality, a typical card network has 50 – 100 variations on these messages plus other message types such as for chargebacks

- cards are prone to fraud as the card Primary Account Number (PAN) is used for routing card payments and for authorising transactions, requiring the PAN to be shared between the issuing and merchant sides of the value chain, risking exposure for fraudsters to intercept5

- cards are for paying only, limiting their utility - there is no universal facility for two-way processing that combines paying and accepting, with some exceptions6.

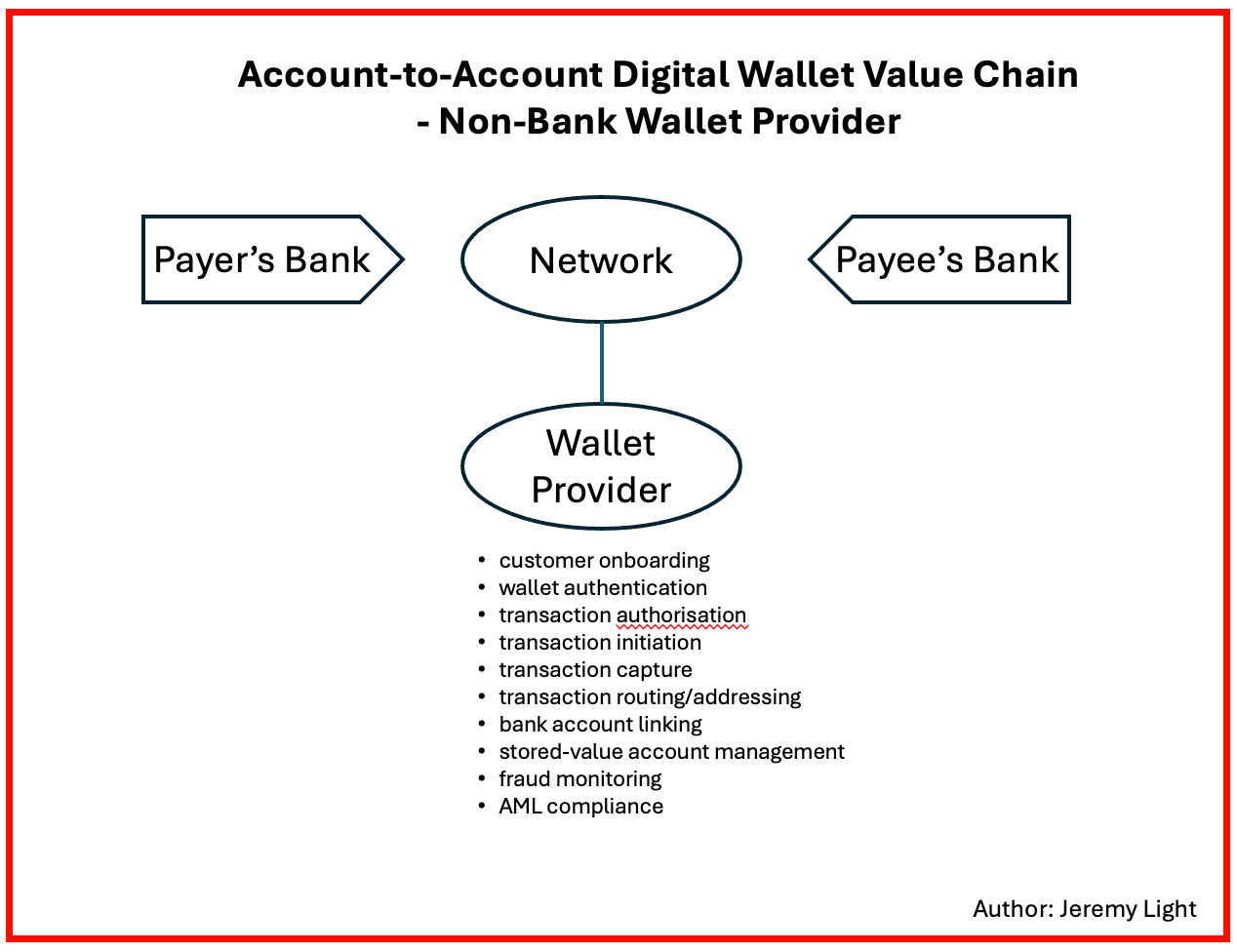

In contrast, the A2A digital wallet value chain is far simpler, giving it versatility without the drawbacks of the card value chain7, as shown in Figure 2.

Figure 2 – Account-to-Account Digital Wallet Value Chain

With an A2A digital wallet, typically a user downloads the wallet from the wallet provider, onboards themself by setting up their wallet address, linking their bank account to it and/or setting up a separate stored value account. The wallet is then ready to use for making and receiving payments.

There are far fewer organisations in the payment flow, at the most basic level just the wallet provider, far fewer message (and API) flows and the wallet can be used like cash for sending and receiving payments.

PayPal has proven this model for a long time, processing 26bn payments in 2024, about half in the USA. PayPal was developed for ecommerce and cross-border payments but now countries are adopting their own A2A digital wallets for everyday domestic use.

Examples include:

- UPI (India)

- PayNow (Singapore)

- M-PESA (Kenya)

- Alipay and WeChat Pay (China)

In India, UPI wallets are downloaded from banks or non-banks. The user chooses their wallet address to be a UPI ID, phone number, bank account number or a QR code (linked to a UPI ID or bank account). Authentication and authorisation are through a PIN registered on set up. The wallets in the other examples operate in a similar way.

In India, 500m merchants use their UPI wallets with QR codes to accept payments, mainly street vendors and small businesses8. In Thailand, when PromptPay launched QR codes in 2017 there were around 713k point-of-sale terminals (903k today) in stores accepting cards, while street traders and small businesses accepted cash only. Within two years, 6m small merchants were using PromptPay to accept A2A wallet payments using QR codes as an alternative to cash9.

These examples illustrate how A2A digital wallets are easier to use and more versatile than cards and are accessible by everyone to pay and get paid, even those without a bank account.

There are variations on the A2A digital wallet value chain, such as that shown in Figure 3.

Figure 3 – Account-to-Account Bank Digital Wallet Value Chain

Figure 3 is very similar to Figure 2 but without standalone digital wallets independent of banks. Wallets are available only through banks who design them with their own UX and features. Examples include Blik in Poland, Swish in Sweden and Zelle10 in the USA. Some networks support both the models in Figures 2 and 3 such as Pix and UPI. However, a single wallet that can be used by any consumer regardless of their bank is likely to have wider adoption than a bank wallet available only to their customers. This is the case with UPI in India where 97% of wallets are non-bank and can be linked to any bank in the UPI network.

The A2A digital wallet value chain collapses the card payment value chain, making A2A digital wallets cheaper and easier to use than cards. The simplicity of the A2A digital wallet value chain compared to the complexity of the cards value chain explains why A2A digital wallets are racing ahead of cards in countries where card penetration has been low. They are also making headway in countries with high card adoption such as Brazil and Poland and it is inevitable in time they will make progress in countries with very high card adoption such as the UK and USA.

Worldpay and Barclays

The impact of A2A digital wallets on cards will become apparent. Already, for example in Brazil, Fintech card acquirers such as Stoneco and Pagsecuro have seen their share prices drop 80% since Pix A2A digital wallet payments launched in 2020.

Here in the UK, cracks are starting to appear in the cards market with several recent deals showing a shakeout is underway. Global Payments is buying the Worldpay merchant business from GTRC and FIS11, who in turn is buying Global Payments’ issuing business. Meanwhile, Barclays is selling its merchant business to Brookfield12.

Both Global Payments and Brookfield have their work cut out. There was a time a decade or so ago when Barclays and Worldpay’s UK business had over 90% of the UK merchant acquiring and processing market between them. Competition from new entrants such as Stripe, Adyen, Dojo, Sum Up and others has reduced that market share. Now, both Barclays and Worldpay offer some of the lowest merchant service charges in the UK13, indicating they are competing mainly on price, lacking the modern capabilities of the new entrants. Both require substantial investments.

This is the fourth time Worldpay has been sold including its spin-out from RBS in 2010. It has been kicked around like a football between different owners, during which time it has increased its global revenue and processed transaction volume/value about 7 - 10x, due to acquisitions as well as organic growth. In the past, payment acceptance businesses have been highly attractive, particularly to private equity, with per transaction fee models, large and growing volumes and strong cashflows making them a financialisation dream to squeeze out value. However, today that opportunity is starting to disappear, with fees under pressure to maintain volumes and card volumes at risk from substitution from A2A digital wallets.

Twenty+ years ago an outsourcing boom saw a shakeout in cheque and paper processing in banks, with for example, IPSL in the UK, Postbank in Germany and Abn Amro in the Netherlands taking on processing from other banks at good margins. When volumes started to fall away, displaced by electronic payments, they were left with high fixed costs, reduced cashflows and an obsolescent business line. The same may happen eventually in cards processing, on both the issuing and acceptance side.

The deals announced last month are more about efficiency and survival than growth. They may be a “canary in a coal mine” signalling the cards value chain has had its day and is uncompetitive compared to A2A digital wallets, including in countries where they have yet to be adopted.

Conclusion

Value chain analysis is a great way to understand different payment methods. It explains why A2A digital wallet payments are gaining rapid adoption and why they are a threat to cards. The A2A digital wallet value chain shows how these payments are simpler to use and much closer to the cash experience through the ability to accept payments just as easily as making them.

In addition, value chain analysis helps understand the various types of digital wallets, which can be ambiguous. For example, many assume digital wallets to mean Apple Pay and Google Pay. These are indeed wallets and provide a very slick payments experience but they are typically cards-based, supporting the cards value chain in Figure 1, adding yet another organisation to the cards ecosystem and another mouth to feed. As such, they are very different to A2A digital wallets.

Digital asset and stablecoin wallets are another type of wallet as are cash-in/out wallets like M-PESA in Kenya (which is also an A2A wallet). I outlined a digital wallet taxonomy in a previous article14 and observed some of the best wallets are a hybrid of the different types, allowing them to work with cards, A2A payments, digital assets and cash, maximising their utility and relevance, enabling consumer choice and market forces to determine how they are used.

Decades ago, banks used to issue separate cards for guaranteeing cheques, ATM withdrawals and POS payments which evolved into a single card combining all three. The same will be the case for digital wallets supporting different payment methods and value chains.

The mainframe is still alive and well, indeed thriving. However, its market share is modest compared to cloud and distributed systems which have become ubiquitous. These are the backbones of computing today, powering the internet, digital services and enterprises of all sizes, having developed enormously over the past 25 years.

A2A digital wallet payments are likely to follow a similar path, spreading throughout the world with a growing market share for decades to come, in time, surpassing cards everywhere.

Visa annual report 2024: https://annualreport.visa.com/financials/default.aspx

Mastercard annual report 2024: https://s25.q4cdn.com/479285134/files/doc_financials/2024/ar/MA-12-31-2024-10-K-as-filed-with-exhibits.pdf

PBOC payment reports: http://www.pbc.gov.cn/en/3688110/3688259/3689026/3706133/4756451/5327700/index.html

Leading to higher costs and layers of complexity (such as PCC DSS, tokenisation) increasing card processing costs

Visa Direct and Mastercard Send allow payments to be accepted onto a card but they work online only and are less convenient to use than online/banking, limiting their use mainly to cross-border P2P, B2C and B2B payments.

Digital wallets still suffer fraud, criminals will always find a way, but digital wallets are less prone to fraud as payment addressing is separate from authentication/authorisation. Payments are “pushed” to the recipient under the payer’s control, reducing the opportunity for fraud, rather than “pulled” to the merchant under the merchant’s control, as happens with cards.

QR Code tiger 14 April 2025: https://www.qrcode-tiger.com/upi-qr-code

Thailand POS Terminals: https://www.bot.or.th/en/statistics/payment.html

Thailand PromptPay QR users (p24): https://fastpayments.worldbank.org/sites/default/files/2021-09/World_Bank_FPS_Thailand_PromptPay_Case_Study.pdf

Zelle used to have a standalone wallet but this was withdrawn in 2025 - each member bank incorporates Zelle into its mobile banking app/wallet

Finextra - Global Payments/Worldpay: https://www.finextra.com/newsarticle/45852/global-payments-to-buy-worldpay-for-227bn-sell-issuer-solutions-to-fis

Finextra - Barclays/Brookfield https://www.finextra.com/newsarticle/45853/barclays-strikes-deal-with-brookfield-to-offload-payments-business

For in-store retail debit cards, Barclays charge 0.6% + 3p, Worldpay 0.4% + 4.5p. These are published rates for small businesses, large retailers will have lower, negotiated rates.

Digital wallet taxonomy: https://jeremylight.substack.com/p/whats-going-on?r=axqgy

Thanks for this Jeremy, a very practical view on the market dynamics. I continue to be surprised that major merchants (eg, British Airways) don't offer me an A2A option with rewards, but perhaps the European dynamics will change as the digital identity wallets come online.