Unstoppable

India's UPI real-time payments system turns 10 this week

This week marks the 10th anniversary of the launch of India’s Universal Payments System (UPI) on 11 Apr 2016.

Since then, UPI has processed 728bn payments, currently at the rate of 23bn per month, around 86% of all electronic payments in India. It continues to grow at almost 30% annually.

I have covered UPI twice before in previous articles1 but this milestone is significant and deserves recognition.

UPI Transactions

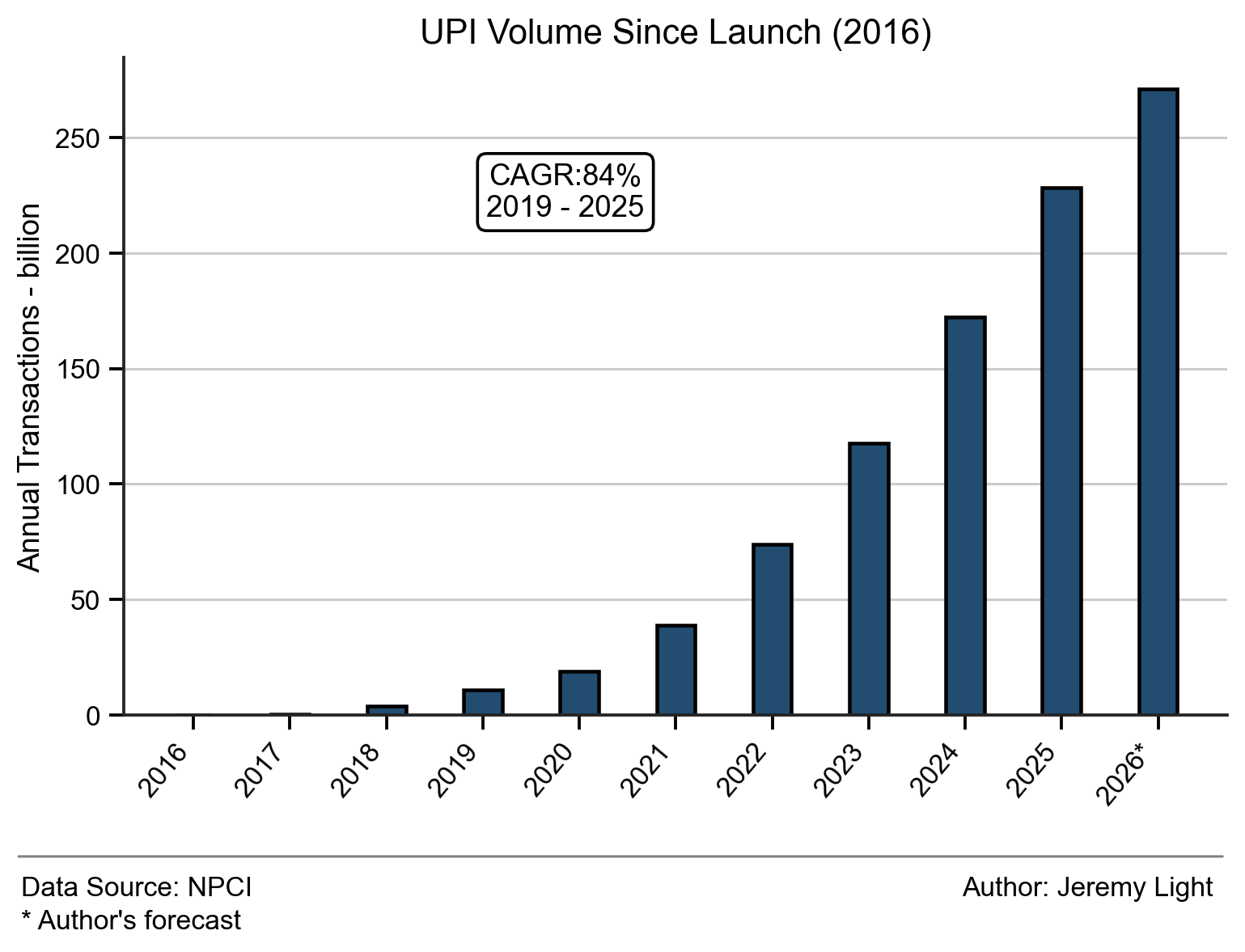

UPI processed 228bn payments in 2025, which equates to 156 payments per capita for the year. The full annual volume history is shown in Figure 1. The CAGR since 2019 is 84% (145% if calculated back to 2017, its first full year of operation). Conservatively, I forecast 271bn payments for 2026.

Figure 1 – UPI volumes since launch

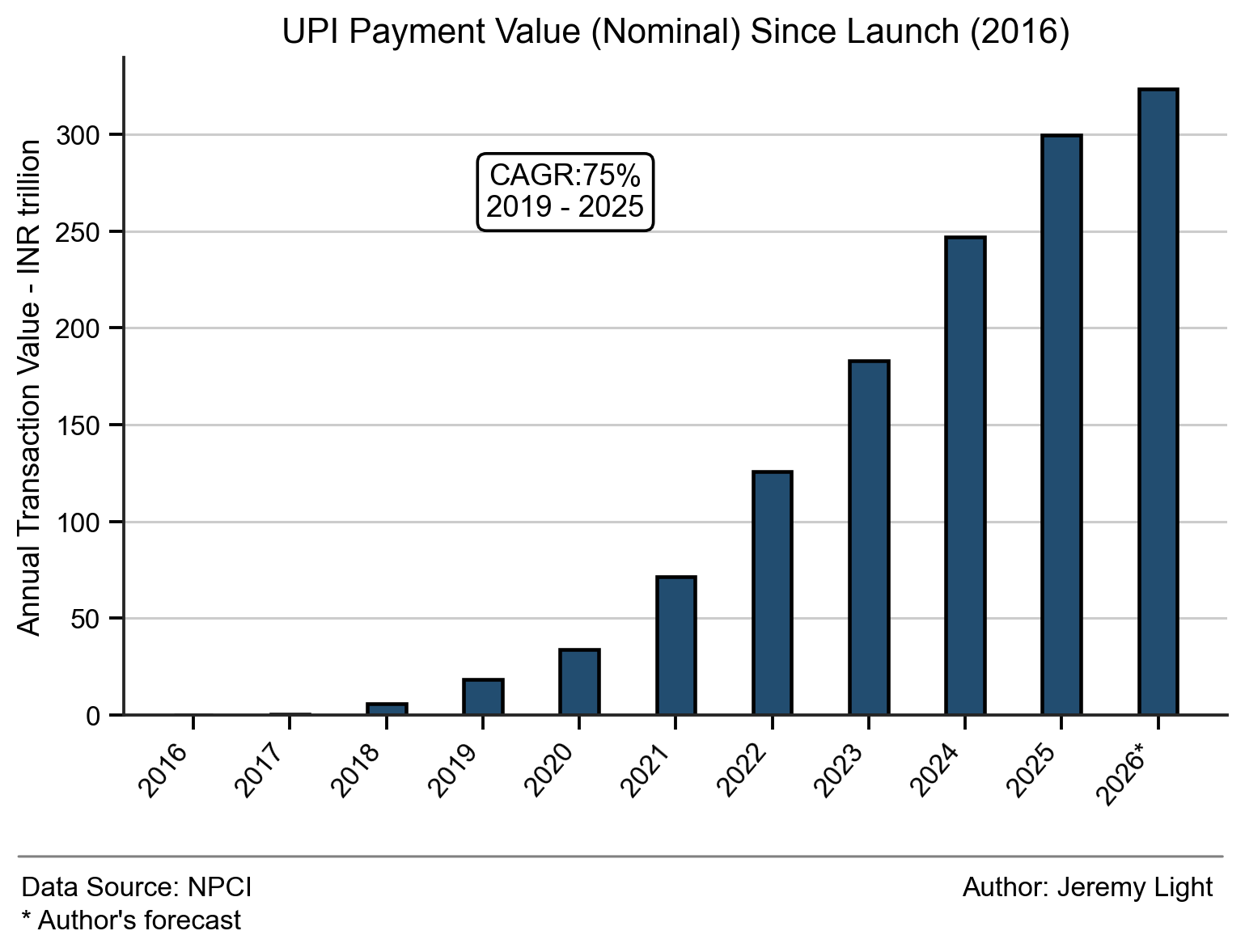

In value terms, UPI processed 300trn INR (3.2trn USD) in 2025, or 205,000 INR (2,200 USD) per capita for the year. The full annual value history is shown in Figure 2 (nominal value, unadjusted for inflation). The CAGR in nominal terms since 2019 is 75%. For 2026, I forecast 324trn INR (3.5 trn USD).

Figure 2 – UPI annual processed value in INR since launch

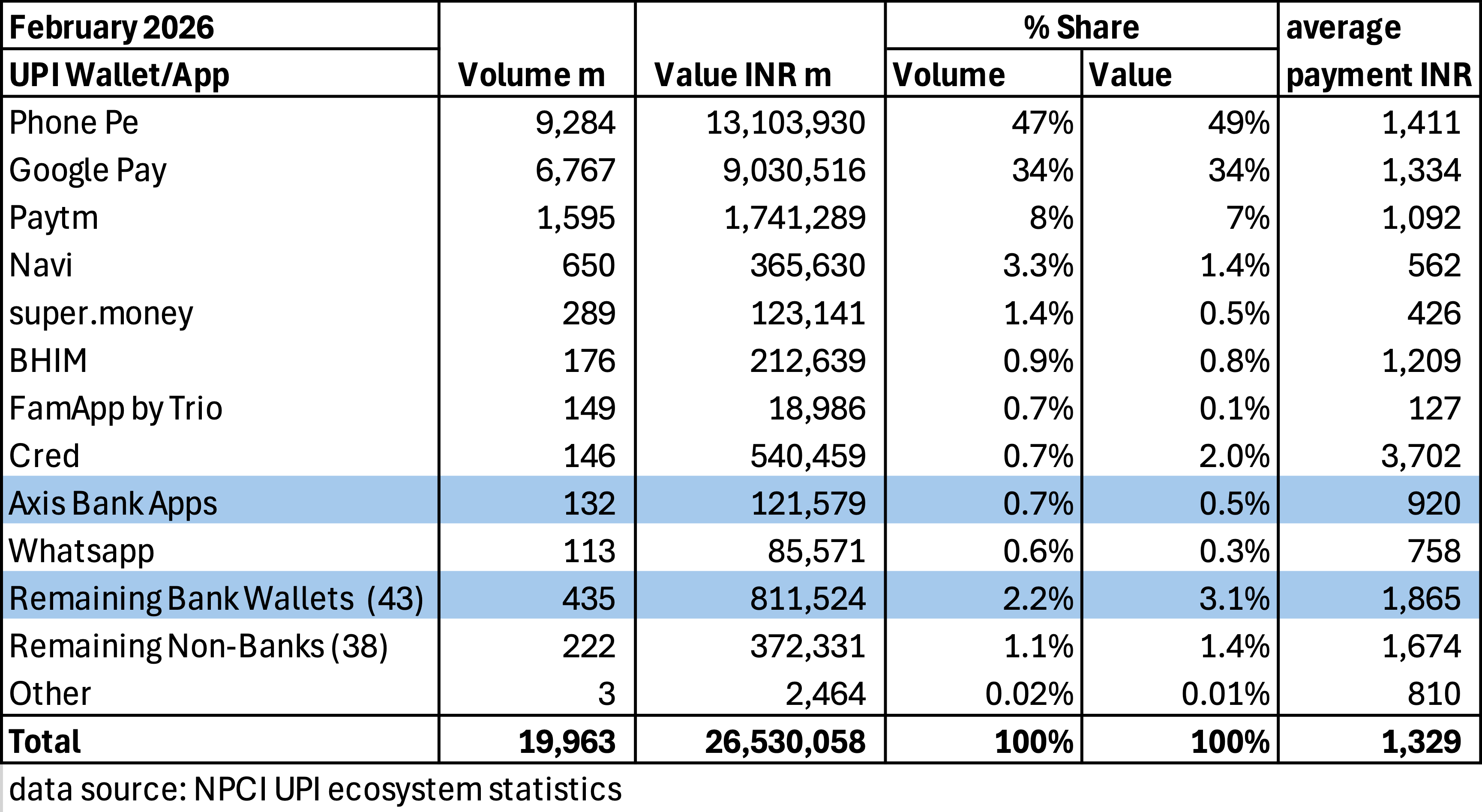

47% of UPI volume is initiated through the PhonePe wallet, part of the Flipkart e-commerce group in India, owned by Walmart in the USA. Another 34% is initiated through the Google Pay wallet.

In the top 10 wallets ranked by volume, there is only one bank wallet, which accounts for 0.7% of UPI volume. The rest are wallets from third party app providers (TPAPs). Overall, there are 47 TPAP wallets accounting for 97.1% of UPI volume and 44 bank wallets accounting for just 2.9% of volume. Figure 3 shows a table of the top wallets, using February 2026 data provided by NPCI, the operator of UPI (and other payment systems).

Figure 3 – UPI wallet providers, bank (shaded blue) and non-bank and market share

I published a similar table to Figure 3 as of December 2024 in my first article (footnote 1). Notable changes over the intervening 14 months are:

- Phone Pe and Google Pay remain the dominant leaders but their market shares have declined slightly – Phone Pe’s volume share has declined by 1.9% and Google Pay by 3.3% and both have dropped 1.6% market share of transacted value

- ICICI Bank and Amazon Pay have dropped out of the top 10 and BHIM, NPCI’s own UPI wallet and Whatsapp have entered the top 10

- Within the top 10, NPCI’s BHIM wallet has jumped the most in the volume rankings from 15th to 6th

- Navi has increased its market the most, by 2% to 3.3% of all UPI payments, almost tripling its share over the period

- The total number of wallets has increased from 82 to 91, with five new TPAP wallets and four new bank wallets.

It’s fair to say that even though Phone Pe and Google Pay have over 80% market share between them, with 91 UPI wallets in total, competition is strong. The size of the pie is huge and there are plenty of transactions to go round - Whatsapp, the 10th ranked processes 113m payments per month and Samsung Pay, at number 25 processes 10m payments per month.

To illustrate how the TPAPs differentiate their wallets to compete, Navi was the first wallet to offer biometric authentication with FaceId instead of requiring a PIN; super.money offers rewards and up to 3% cashback; FamApp focuses on personal finance education; and Cred allows UPI payments on credit.

NPCI has mandated2 that no TPAP can have greater than 30% market share by the end of 2026 – this suggests a major shift in market shares this year if Phone Pe and Google Pay are to comply with the deadline.

UPI Services and Features

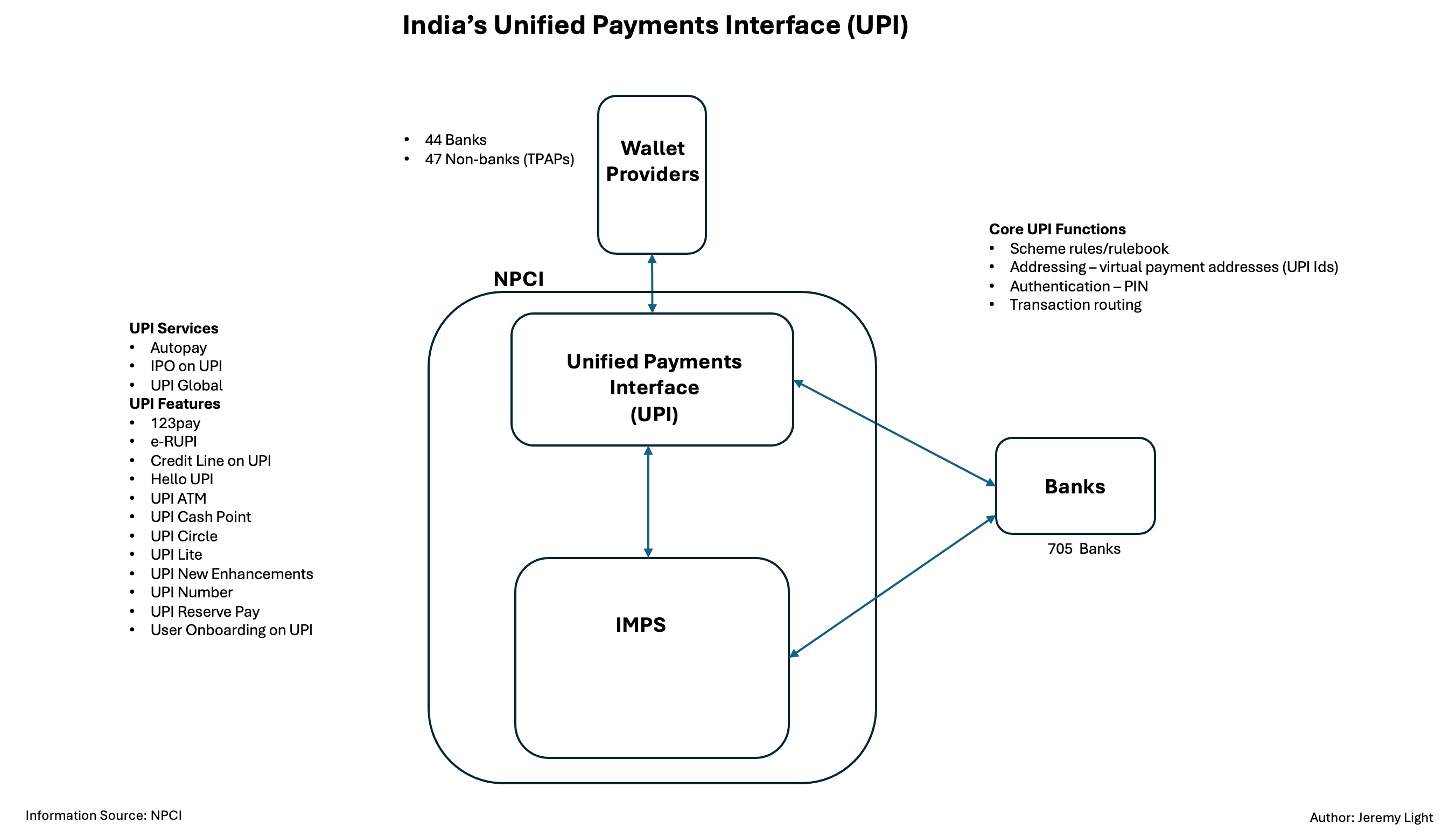

Figure 4 shows the UPI ecosystem of wallet providers and banks connected to NPCI. A description of UPI’s core services and how it works is in my original article (footnote 1).

Figure 4 – UPI ecosystem

In summary, the core UPI service holds a database of UPI id virtual addresses e.g. jeremy@paytm and routes payments between them. A user connects their bank account(s) to a UPI wallet of their choice (there is no need to use their own bank’s UPI wallet, if it has one) and creates a UPI Id and PIN. To send a payment, the user enters the destination UPI id (or captures it on a QR code), enters the amount and PIN and presses send. UPI resolves the user’s and receiver’s UPI Ids to their respective banks and triggers a real-time payment between the banks using the IMPS clearing and settlement system.

NPCI has built a rich set of UPI services and features around its core service. These are3:

UPI Services

• Autopay – set up e-mandates for recurring payments (bill payments, subscriptions, insurance etc)

• IPO on UPI – subscribe and buy shares in initial public offerings

• UPI Global - make QR code payments at participating merchants abroad, directly from an Indian bank account.

UPI Features

• 123pay – pay-by-voice with no internet connectivity by calling “Karo”, an IVR (interactive voice response), including a merchant call back facility and in-person using proximity sound-boxes (with multiple regional languages); also allows payments with feature phones

• e-RUPI – pay using UPI by redeeming vouchers distributed by the government and by private organisations, such as for healthcare, education, employee benefits, skills training, agriculture subsidies, government handouts, school meals, subsidised transport

• Credit Line on UPI – pay by drawing down on a pre-approved credit line

• Hello UPI – pay using voice inputs, with multiple regional languages, to conversationally control the payment flow on smartphone apps, feature phones and IoT devices

• UPI ATM – use UPI to make deposits and withdrawals at ATMs on the National Financial Switch (NFS) ATM network

• UPI Cash Point – use UPI to withdraw cash at authorised local shops and agents (there appears to be no cash-in capability to deposit cash at a shop or agent into a UPI wallet, unlike other countries such as Kenya and the Philippines with a similar service)

• UPI Circle – enable secondary users (e.g. family members without a bank account) to make payments from a primary UPI account

• UPI Lite – make payments below 1,000 INR (11 USD) without entering a PIN, including using NFC for offline payments to another phone (Lite X – limit 500 INR) and Tap & Pay at point-of-sale using NFC (requires a PIN for payments above 1,000 INR)

• UPI New Enhancements – support for multi-signatory bank accounts (business accounts, joint accounts) using requests in UPI apps which require approval before a payment is initiated

• UPI Number – set up of an 8 – 10 digit number as an alias to the alphanumeric UPI id, making UPI easier to use on feature phones and enabling interoperability with other service providers e.g. by using mobile phone numbers as identifiers

• UPI Reserve Pay – as an alternative to paying upfront for purchases, money is reserved (max 10,000 INR/108 USD per purchase) for up to 90 days and withdrawn by the merchant when the goods or services are delivered

• User Onboarding on UPI – onboarding onto a UPI wallet using a debit card linked to a bank account or a Aadhaar card (digital id) linked to a bank account.

UPI Lite is particularly interesting with its use of NFC for tap-and-pay and person-to-person payments. Like many other countries in Asia, Africa and Latin America, UPI’s growth has been driven by the use of QR codes at point-of-sale – currently, there are 745m QR codes registered4 with UPI, up from 633m in December 2024. However, NFC is starting to gain traction as an alternative to QR codes, a trend that is appearing elsewhere in the world (outside of western economies where NFC/contactless is used extensively already for card payments).

Fraud on UPI

With billions of payments per week, you would expect fraud using UPI to be quite high in terms of absolute numbers of fraudulent payments. The Reserve Bank of India (RBI) publishes fraud figures for domestic payments as a whole (footnote 4) - 263 thousand fraudulent payments in February 2026, one in every 92,435 payments (0.001%), valued at 3.8bn INR (41m USD). I suspect that UPI payments are a large contributor.

In absolute terms, these figures are high but relative to the volume of payments, they are lower than many countries including the UK, where 0.009% of Faster Payments payments are fraudulent5. They are also on a generally downward trend - three years ago, one in 47 thousand payments in India was fraudulent compared to one in 92 thousand in February this year.

Even so, as of this month, to combat fraud, the RBI requires all electronic payments to use two-factor authentication6, which will have an impact on the user experience. Whether it affects user UPI adoption, volumes and UPI growth rates and whether wallet providers will compete on the slickness of the user experience, remains to be seen.

Conclusion

From nothing 10 years ago, UPI has grown to account for 86% of all electronic payments in India, processing 23bn payments per month.

Cash is still used throughout India and UPI has potential to grow significantly higher if it continues to displace cash. UPI payments per capita reached 156 in 2025, which is far below Kenya at 613 and Thailand at 485 in 20247. It is quite possible that UPI will reach 700bn – 900bn annual payments within three to four years and a trillion payments soon after.

With over 91 different UPI wallets to choose from, over half from non-bank TPAPs, NPCI has created a vibrant and competitive ecosystem, albeit one dominated by Phone Pe and Google Pay. This has led to the creation of a range of innovative new services and features, including the ability to use UPI internationally.

The growth of services and features around UPI looks unstoppable and I am sure that over the next 10 years there will be a lot more to come.

UPI articles: Feb 2025 - https://jeremylight.substack.com/p/sailing-to-the-moon

Aug 25 - https://jeremylight.substack.com/p/indian-upi?r=axqgy

TPAP market share limit: https://coingeek.com/india-delays-upi-market-share-cap-deadline-by-2-years/

Listed from NPCI’s website: https://www.npci.org.in/product/upi

RBI Payment System Indicators: https://www.rbi.org.in/Scripts/PSIUserView.aspx?Id=57

UK Payments Fraud: https://open.substack.com/pub/jeremylight/p/take-the-money-and-run Also see Figure 3, domestic payments fraud rates in India: https://jeremylight.substack.com/p/que-qr-qr-whatever-will-be-will-be

RBI’s Authentication Mechanisms for Digital Payment Transactions Directions, 2025 - Etedge March 2026”: https://etedge-insights.com/industry/bfsi/upi-payments-mode-change-april1/

Real-time payments per capita index 2024: https://jeremylight.substack.com/p/mirror-mirror-on-the-wall-who-is?r=axqgy