Sailing to the Moon

How digital payments are skyrocketing in India due to the Unified Payments Interface (UPI)

UPI, the Unified Payments Interface, reached 131bn payments in India’s last financial year (Mar 23 – Apr 24)1, up from 22bn four years ago and, I forecast, will reach over 180bn payments in the financial year to April 2025.

Figure 1 shows the trajectory - UPI is sailing to the moon.

Why is UPI so successful and how is it driving the transition from cash to digital payments in India?

Figure 1 – the relentless adoption of UPI digital payments in India

=========================================================================

All currency figures in this article are in Indian Rupees, INR. The following exchange rates as of 5 Feb 25 will help the reader convert into other currencies:

1 GBP = 109 INR, 1 USD = 87 INR, 1 EUR = 91INR

=========================================================================

UPI was launched in April 2016 with 21 banks as part of the government’s wider digital strategy, aimed at driving financial inclusion, reducing cash reliance and creating a competitive, homegrown payments ecosystem.

2016 was also the year of India’s notorious demonetisation when overnight, 86% of the cash in circulation was declared to be no longer legal tender, creating chaos2 (and somewhat puncturing the notion that central bank money is free of risk). Whether the two were linked to give UPI digital payments a boost is unclear.

However, UPI took off rapidly with 7.1m txns in April 2017 rising to 190m in April 2018, by which time 97 banks supported UPI. As of December 2024, now 641 banks are connected and almost 17bn UPI payments were processed3 that month. For the record, cash in circulation also took off reaching 36 trillion INR today, up from around 18 trillion INR in 2016 (and from just below 10 trillion INR immediately after the demonetisation)4.

How UPI Works

UPI works by enabling any mobile wallet/app in the UPI system, bank or non-bank to initiate a payment in the wallet, paid from the user’s bank account (or credit card) to the recipient’s bank account. UPI wallets work both for online and face-to-face payments.

The payment is authorised by the user’s bank (or credit card issuer) using a UPI PIN entered in the wallet (the PIN is held at the bank, registered on wallet set up). Other security features may include device binding – the app works only on the original registered phone; phone verification – payments can be initiated only from the SIM registered with the bank; and biometrics (face or fingerprint on the phone).

A payment is addressed to a recipient’s bank account using any of: a UPI ID, phone number (if linked to UPI), bank account number + IFSC code, or QR code (linked to a UPI ID or bank account). Payments are to bank accounts only, except wallet-to-wallet payments are permissible with prepaid wallets (allowing use by the unbanked).

Payments are settled using mainly IMPS (instant payment system), or NEFT (an ACH system) for scheduled or low priority payments, or RTGS for high value payments or the card networks, including Rupay if a card payment.

You can see a UPI wallet in action in this delightful video clip (55s) posted on LinkedIn by Suresh Vaghjiani, a Fintech entrepreneur, showing a purchase for just 1 INR ($0.01), highlighting:

- Use of a QR code (633 million were in use in Dec 24, double Dec 23 – see footnote 5)

- Entry of the UPI PIN in the wallet to authorise the payment

- Real time settlement and real time audible notification to the shop owner

- Use of UPI for micropayments as low as 1 INR.

UPI’s Impact

Total retail electronic payments in India have increased from 44bn payments in FY20/21 to 165bn in FY23/24, an increase of 121bn. Almost of all of it, 109bn is due to the increase in UPI payments, which account today for 80% of all retail payments, as shown is Figure 2.

Meanwhile card payments, credit and debit, which have never had the same penetration in India as elsewhere in the world, account for just 4% of all retail electronic payments, down from 7% in FY20/215. India has mostly skipped the card generation, straight into digital wallets.

Figure 2 – the divergence of UPI payments and card payments in India

UPI is growing a significant share of electronic payments by value. NEFT, the ACH system has seen its annual value increase from 251 trn INR in FY20/21 to 391trn in FY23/24, but UPI increased even more from 41 trn INR to 200 trn INR. Consequently, as shown in Figure 3, UPI’s share of retail payments has increased from 10% to 25% by value, while NEFT’s share has fallen from 61% to 49% even though the value processed has grown.

Figure 3 – UPI’s growing share of retail payments by value at the expense of NEFT’s share

UPI payments are also accelerating the decline of cash usage. Despite the demonetisation in 2016, cash in circulation has quadrupled since then (or only doubled if the pre-monetisation level is used as the starting point).

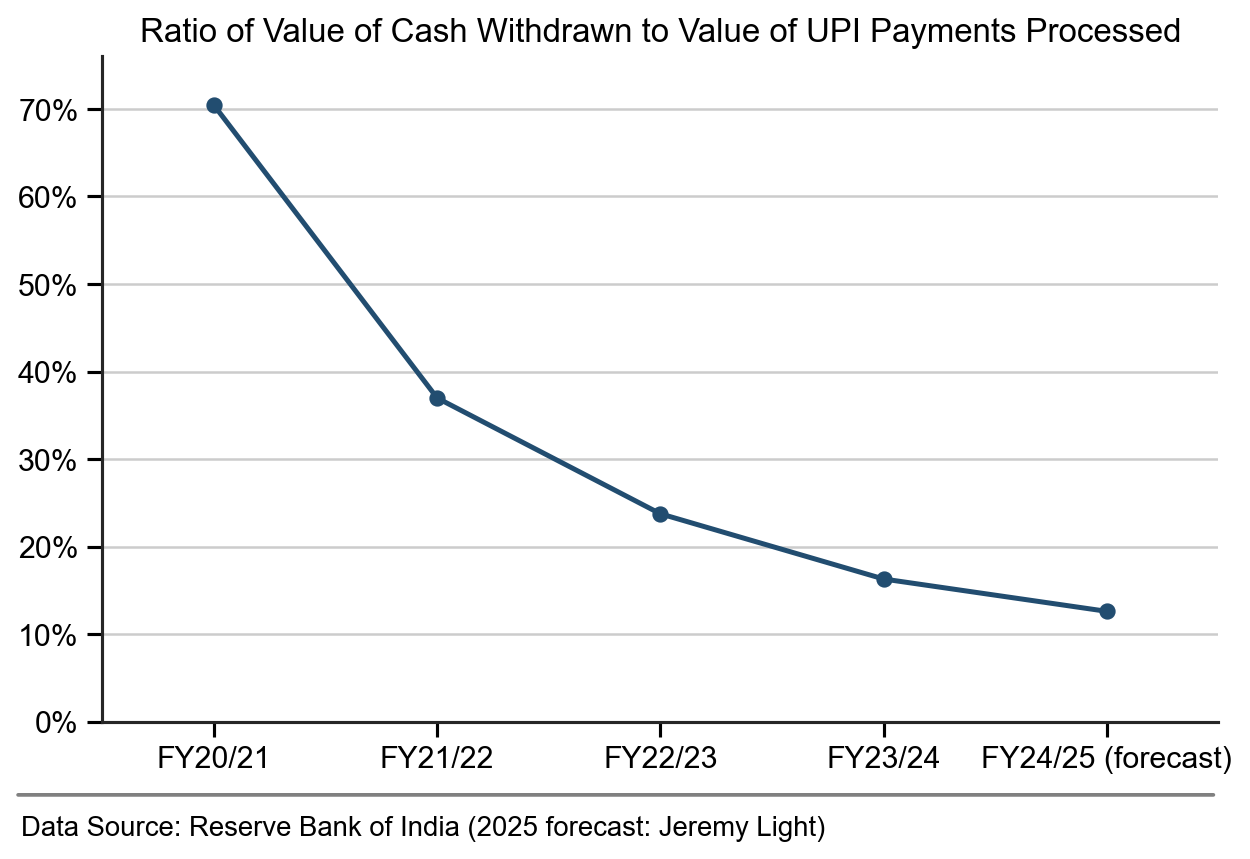

Cash use has been on the rise but, using ATM withdrawals as a proxy for cash use, these appear to have peaked at 7bn withdrawals in 2023 valued at 33 trn INR. However, the ratio of the value of ATM withdrawals to the value of UPI payments processed has declined precipitously from 70% in FY20/21 to 16% in FY23/24 and looks set to continue declining, as shown in Figure 4.

Figure 4 – India’s declining ratio of cash usage (ATM withdrawals) to electronic payments (UPI)

Whether intentional, or otherwise, India is managing successfully to transition its huge population (1.43bn people) from cash to digital payments through UPI by promoting digital inclusion, while ensuring cash is accessible for those who rely on it, especially in rural areas.

In a previous article, I explained how the digital economy is causing payments to atomise where people are making more and more payments for smaller and smaller amounts. This is very apparent with UPI, where over the past four years the average payment value for the year has dropped from 1,838 INR to 1,525 INR, while volumes have increased five-fold and in the face of inflation averaging over 5% p.a. (the same is seen in NEFT, where average values have dropped by more than a quarter while volumes have more than doubled).

Wallet Providers

The success of UPI may lead you to believe the government and central bank have executed their digital strategy with perfection. In reality, they have laid the groundwork and created the environment for success, but that success, rather than coming from banks as planned, has come almost exclusively from non-bank wallet providers, a.k.a TPACs (third party app companies).

In fact, I believe it fair to assess that the banking sector, central bank and government have been wrong-footed, even blindsided by the success of the TPACs.

48% of UPI volume is initiated through the PhonePe wallet, part of the Flipkart e-commerce group in India, owned by Walmart in the USA. Another 37% is initiated through the Google Pay wallet.

In the top 10 wallets ranked by volume, there are only two bank apps which between them account for 1.2% of UPI volume. Overall, there are 34 TPAC wallets accounting for 97.4% of UPI volume and 48 bank wallets accounting for just 2.6% of volume. Figure 5 shows a table of the top wallets, using December 2024 data provided by NPCI, the operator of UPI (and other payment systems)6.

Figure 5 – UPI wallet providers, bank and non-bank and market share

The success of the TPAC wallets is due to a great UX and ease-of-use, far better than bank apps; cashbacks and incentives in the early days; and critically, TPAC wallets are linkable to any UPI bank (641) covering most of the banked population, whereas bank wallets are linkable usually just to the bank, restricting its use to their customers only. UPI also supports prepaid wallets which gives the unbanked access to UPI.or the unbanked.

However, this TPAC success must be a concern for the RBI, the central bank. First, the market is dominated by two US-owned companies rather than India-owned. Second, the banks are no longer in control of retail payments. Third, there are no UPI transaction fees on UPI bank transfers payable to TPACs or banks to generate revenue (although retailers must love it), so there is likely a question mark on how sustainable UPI is in the long run (I will cover UPI fees in a later article). Additionally, UPI has disrupted government plans for financial inclusion – it had introduced a payment system, AePS for the unbanked using the Aadhaar digital id, but AePS is barely used, superseded by UPI for digital payments.

The RBI has taken action to limit TPACs’ UPI share to 30%, but has delayed enforcing it for the second time for another two years7. It is difficult to see what PhonePe and Google Pay can do to reduce their transaction share without causing severe disruption (perhaps a digital demonetisation is on the horizon?). Interestingly, RBI has given the go ahead to Whatsapp, another US business (Meta) to open up its UPI wallet to all its 500m users in India, which will likely boost its share (currently just 0.4%)8.

Lessons for Other Countries

UPI provides useful insights on how to transition from a cash-based economy to digital payments:

1. Governments and central banks may create the environment for digital payments, but should stick to enabling infrastructure on which the private sector can build applications

2. UPI is a success because it is a platform for others to develop products, rather than a product itself

3. Banks on their own are ill-suited for creating customer facing wallets, proven by 641 banks with 2.6% share of UPI volume – this is best left to third parties (which can be bank owned such as Zelle in the US, Wero in Europe) to focus on getting the UX and customer proposition right, as proven by PhonePe and Google Pay with a combined 85% share of UPI volume

4. Digital wallets need to be bank-agnostic and work with any bank to maximise their customer-base

5. Digital payments present an ideal opportunity to build homegrown payment services led by Fintechs, but Big Tech will make a land grab unless prevented. India has avoided the Visa/Mastercard duopoly only to let in another duopoly of US-owned companies. To avoid competition and market problems when digital payments scale, Big Tech needs to be kept out or limited from the start

6. Digital payments have no need for digital id – UPI proves that, with over 283bn payments made in the past four years without digital id. Further the AePS payment system in India designed to use the Aadhaar digital id system is a flop (just 392,000 payments were made with in FY23/24, footnote 5)

7. To facilitate the transition from cash users to digital payments, a digital payment system needs to be usable with or without a bank account. UPI wallets are interoperable whether linked to banks, cards or are prepaid (with some restrictions – bank-linked wallets may send only to other bank-linked wallets, prepaid wallets can send to prepaid and bank-linked wallets).

Two weeks ago I wrote an article on how countries are developing payment visions and strategies, emphasising they need to be bold to be relevant for the digital economy. UPI provides powerful insights and lessons to inform these strategies.

NPCI, UPI’s operator, itself has a bold strategy to expand UPI to other countries9 with at least 10 already connected – for those outside India, look around you, UPI may be with you already.

The Reserve Bank of India’s statistics are published by accounting year March to April

India demonetisation 2016: https://www.bbc.co.uk/news/world-asia-india-37974423

UPI Statistics: https://www.npci.org.in/what-we-do/upi/product-statistics

RBI Payment System Indicators: https://www.rbi.org.in/Scripts/PSIUserView.aspx

NPCI UPI Ecosystem Statistics: https://www.npci.org.in/what-we-do/upi/upi-ecosystem-statistics

Finextra UPI Market Share Cap Deadline: https://www.finextra.com/newsarticle/45297/india-delays-upi-market-share-cap-deadline

Finextra UPI Whatsapp: https://www.finextra.com/newsarticle/45256/whatsapp-pay-made-available-to-all-indian-users

India Briefing UPI International: https://www.india-briefing.com/news/global-acceptance-of-india-unified-payments-interface-upi-tracker-26183.html/