Got a Lot o' Payin' to Do

Micropayments, agentic AI, payment atomisation and exponential volume growth

Seven years ago, I wrote two articles on the atomisation of payments:

https://www.finextra.com/blogposting/14575/the-atomisation-of-payments-part1

https://www.finextra.com/blogposting/14608/the-atomisation-of-payments-part-2

My theme was the acceleration of electronic payment volumes due to emerging new business models enabled by technology. These allow us to pay in the moment, at the point of need causing payments to atomise – the transition from lower volumes of higher value transactions to higher volumes of lower value transactions. For example, buying items online everyday instead of shopping weekly or monthly in a store, paying in installments rather than with a single payment or getting paid daily instead of monthly.

I showed how payments volumes were likely to expand 25 times or more in the future, resulting in trillions of new payments.

So, seven years on, how is it going?

Atomisation in the UK

Using the UK as an example, total volumes have increased from 39bn payments in 2017 to 48bn1 in 2023, with I estimate 51bn payments in 2024. That is a CAGR of 4% - much higher than UK GDP growth, but unexciting and well below the 11% CAGR I estimated in 2017 was needed to get to a trillion UK payments within 30 years (2047).

However, looking below the surface, focusing on the payment methods driven by technology and new business models, the picture is different.

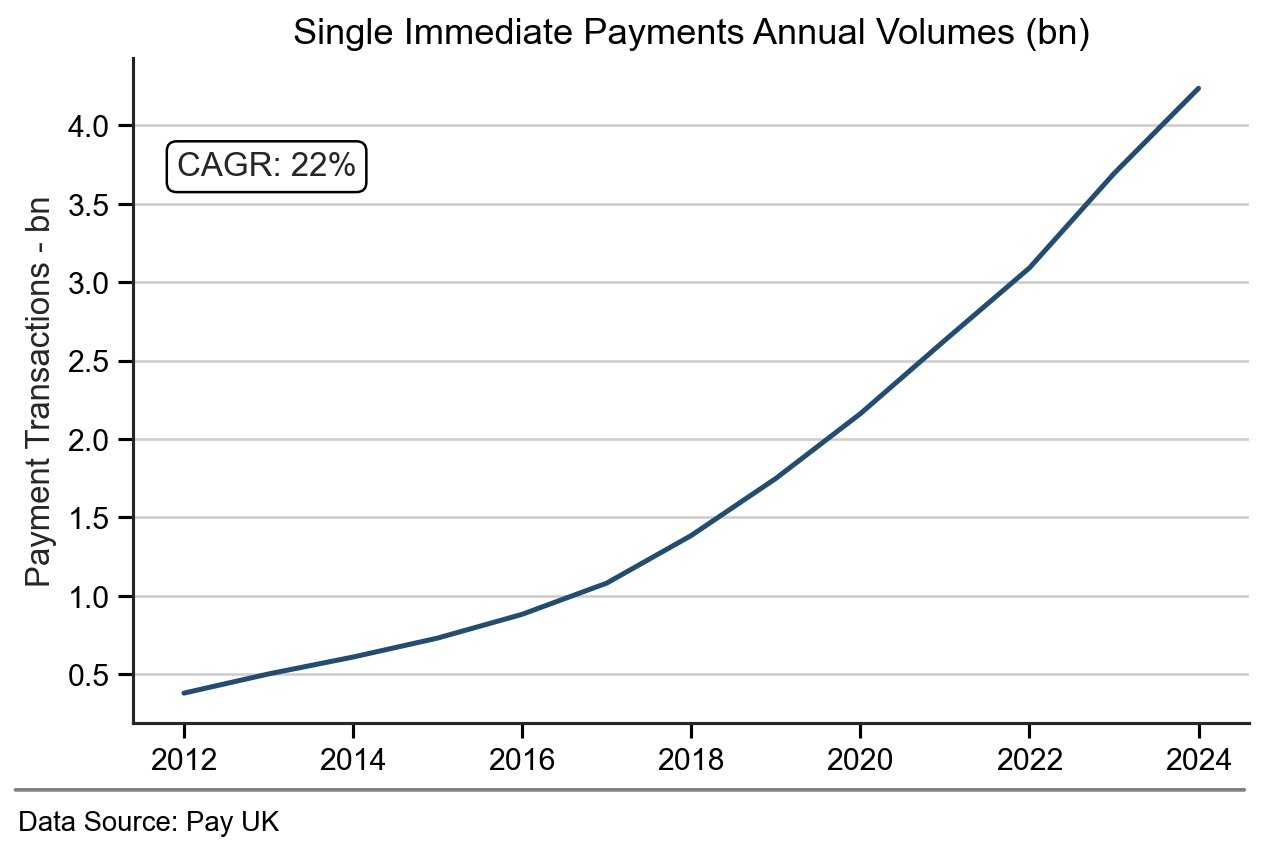

Figure 1 shows the volume of single immediate payments processed by the UK’s Faster Payments System (FPS). Volumes are growing exponentially at a CAGR of 22%, rising from 1.1bn in 2017 to 4.2bn payments last year.

Figure 1 – Growth in Single Immediate Payment (UK) Volumes

At the same time, the average value (inflation adjusted to 2024 money) of a single immediate payment has fallen from £1,147 in 2017 to £696 last year, see Figure 2.

This is atomisation in action – increasing payment volumes and decreasing payment values.

Figure2 – Decline in Single Immediate Payment Average Values

Single immediate payments cover a wide of range of payments, including salary payments, bill payments, business-to-business payments, online banking payments and open banking payments. Consequently, the graphs reflect a wide range of payment values, from £0.01 up to £1m (the FPS limit).

Narrowing payment values down to below £20 ($24) and including cards, statistical analysis shows low value payments are made in very high volumes in the UK and have been growing at a CAGR of 31% since 2020.

As shown in Figure 3, in 2024 I estimate there were 15bn UK electronic payments below £20, a three-fold increase from 5bn in 2020 (note – the data is inflation-adjusted as the UK has experienced high inflation over this period. £20 was needed to buy the same goods in 2024 as £15 would have in 2020).

Figure 3 – The Rapid Rise in Low Value UK Payments (Cards and Single Immediate Payments)

I am sure many readers will recognise this increase from the ballooning number of entries and pages in bank statements and credit card statements today compared to the past.

Payment atomisation is indeed happening, although slower than I believed in 2017.

We are still at the early stages.

Micropayments

One area I am convinced will grow into a major source of new volume is micropayments. These have been touted for decades but have failed to take off so far – mainly because the fixed fees retailers pay for card transactions make selling uneconomic at scale below £20 and there have been few alternatives.

This could change, with a major catalyst being the digital creator economy – sized at $200m in 2023, it is forecast to rise to $600bn in 20362. Currently, it is very difficult for creators today to monetise their content (art, articles, videos etc) without using platforms such as Youtube and this one, Substack, where they face the double-whammy of platform fees and high payment fees, which in total can reach over 20% for low priced content; or they have a dependency on ads on which they no control and which contaminate their content.

Subscriptions are a common way to monetise online content, but these optimise profits for the platforms rather than maximise audiences and revenue for the creators. They may even inhibit the creator economy, especially where consumers are fatigued by subscriptions. In response, creators are seeking ways to avoid the “rented land” restrictions of platforms. Pay-as-you-go alternatives3 allow them to do just that - as they become viable and available, micropayments will take off at scale.

Agentic Payments

Another potential source of high-volume atomised payments are “agentic payments”, where AI agents transact with each other, independent of humans. This is appearing regularly in trend forecasts for 2025 with a number of start-ups4 emerging, although I am unsure it will be as practical or ground-breaking in the immediate future as some suggest. In particular, consumers like to be in control and I believe handing over control of everyday payments to a bot will be a hard sell.

More promising is its use where it is impossible or impractical for humans to make payments themselves - e.g. a bot that finds the cheapest electricity to buy continuously 24/7, or to curate a daily feed of the most interesting/relevant news and current articles for £1/$1 a day. Also promising are business-to-business payments, for example royalties paid directly to the copyright owner every time a piece of music is played, a film watched, a photo used or a digital painting displayed; or in supply chains where insurance and carriage costs are itemised and charged over time down to SKU level instead of by container shipment.

However, such uses are more about automating purchasing decisions and processes than paying. They will require development of new services designed for automated consumption, a far bigger challenge than automating payments. As an example, I included the smart meter scenario in my articles in 2017, expecting meters to pay for electricity automatically, sourced from the cheapest supplier at any given time. Seven years on, smart meters in the UK are widespread, but they do little more than send a meter reading to a single supplier once a month. There is a long way to go.

Conclusion

In conclusion, payment atomisation is happening, but it continues to be “under the radar” in the payments industry, as a gathering, but unseen force. Few are aware of it or planning for it, but as is always the case with persistent exponential growth of more than a few percent, it will be upon us and a major dynamic within the payments industry very quickly – driven by digital business models and technology, soon by micropayments, later perhaps by automated AI agents.

UK Finance (and a predecessor, Payments UK) annual UK payment reports

This is the core capability of the company I co-founded, Fourdotzero https://fourdotpay.io/

Intriguing as always Jeremy.

Excellent piece Jeremy. I've just submitted a paper on "R2R" (robot-to-robot) payments to JPSS and I mentioned micropayments in that. If I get a chance to revise the paper following referee's comments I'll add in a reference to your observations above.