Turning Chinese

How the Renminbi has become a major currency for international payments

October this year marks the 10th anniversary of the launch of China’s Cross-border Interbank Payment System (CIPS).

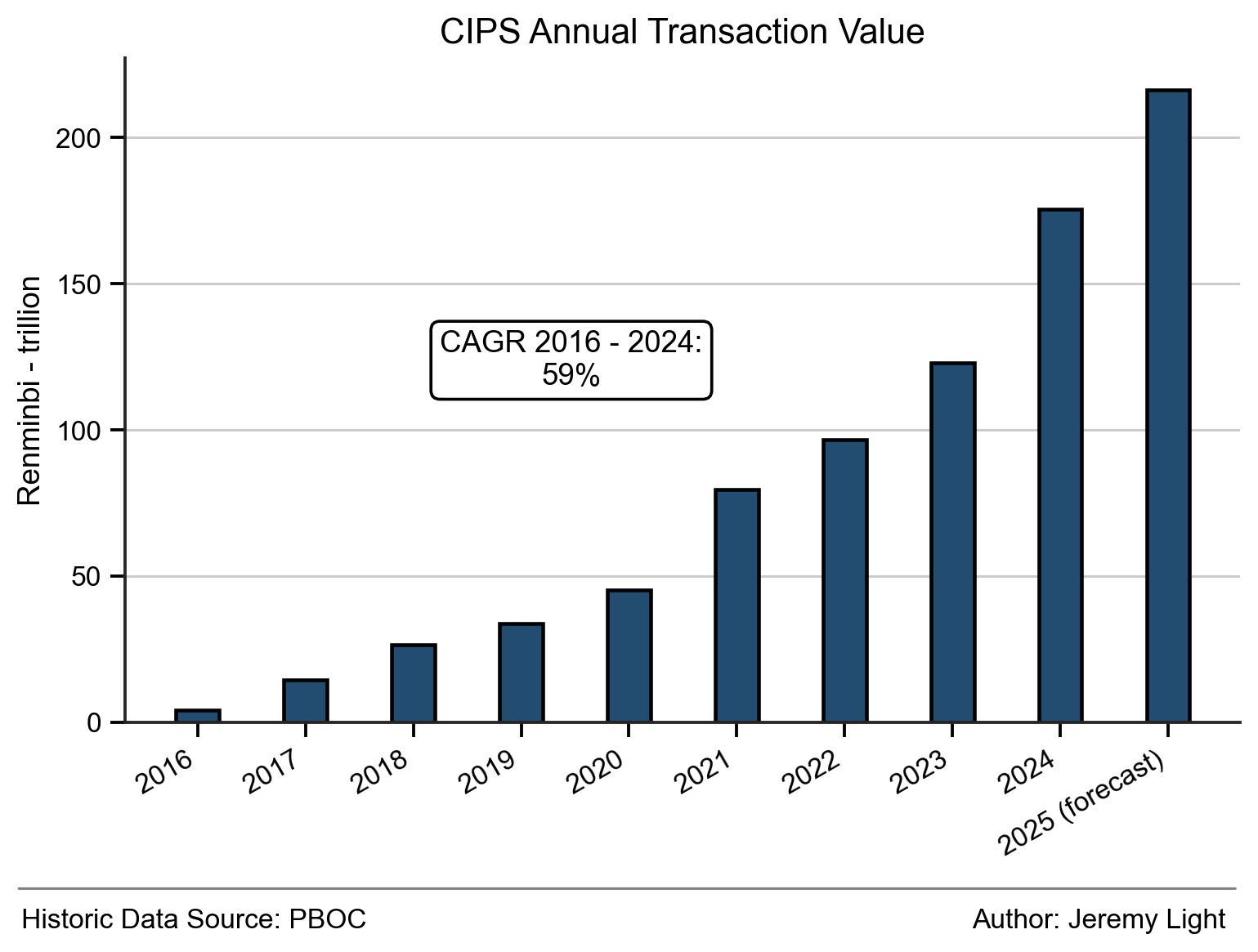

In 2024, CIPS processed RMB 175 trillion1 in payments, equivalent to USD 24.5 trillion. In 2025, I forecast that will rise to RMB 216 trillion, or USD 30 trillion. This constitutes a sizeable chunk of the cross-border payments market, estimated to be USD 195 trillion by FXC Intelligence2.

CIPS receives very little press coverage but I am sure this will change when people realise how enormous CIPS has become. In a world that is increasingly multi polar and with dollar hegemony for international trade under threat, CIPS is now a major force in international payments.

CIPS

CIPS is a RTGS system operated by the People’s Bank of China (PBOC) to clear and settle cross-border payments in RMB. CIPS has 176 direct participants and 1,514 indirect participants, located in 121 countries covering Asia, Europe, Africa, North America, South America and Oceania3.

Uses for CIPS in international payments include:

1. Cross-Border Trade Settlements in RMB – e.g. exporters/importers in Malaysia, Indonesia and Thailand settling trade invoices with Chinese partners using RMB.

2. Commodity Transactions Settled in RMB – e.g. China’s oil purchases from Russia paid in RMB.

3. Belt and Road Initiative Financing – e.g. infrastructure loans in RMB to African nations.

4. Offshore RMB Clearing Banks - e.g. banks such as HSBC (Hong Kong) settling RMB transactions between offshore corporate clients doing business with China.

5. E-commerce & Retail Payment Platforms – e.g. international sellers on platforms like AliExpress, JD.com and Shein receiving cross-border payments that settle ultimately in RMB.

6. Central Banks and FX Reserves Management – PBOC currency swaps with central banks (e.g. in Argentina, Pakistan, the UAE) to settle RMB inflows and outflows.

CIPS Growth

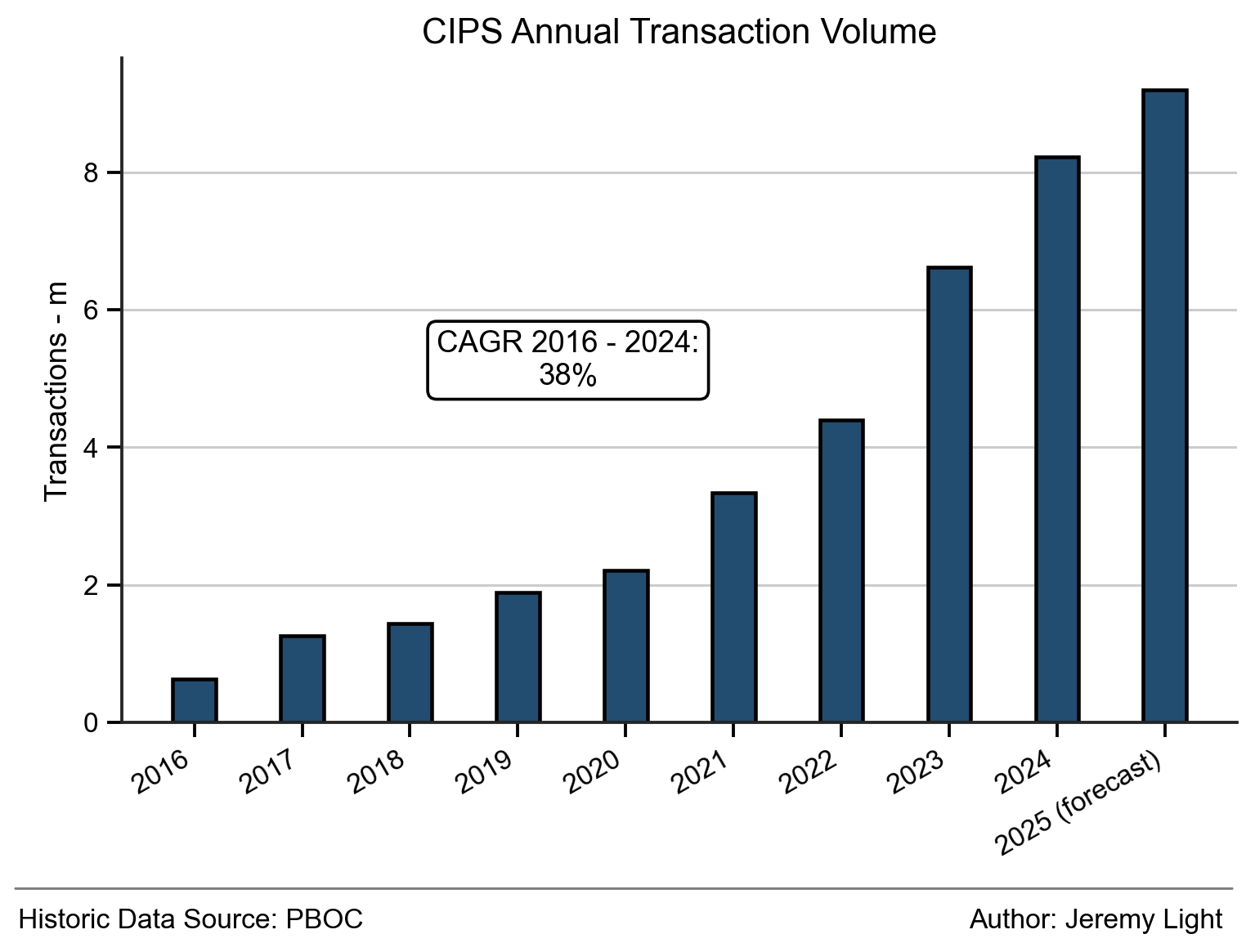

CIPS volumes reached 8.2m transactions in 2024, with an average transaction value of RMB 21m (USD 3m). As shown in Figure 1, transaction volumes have grown at a CAGR of 38% between 2016 and 2024.

Figure 1 – CIPS RMB cross-border payment volumes

Figure 2 shows how at the same time the value of CIPS transactions have grown at a CAGR of 59% between 2016 and 2024, reaching RMB 175 trillion (USD 24.5 trillion).

Figure 2 – CIPS RMB cross-border payment values

Growth in 2025 so far is well down on the historic trends – volumes in Q1 2025 were up just 2% on Q1 2024 and values were up 9% (see footnote 1). Even so, I forecast volume growth of 12% in 2025 to 9.3m transactions compared to 24% growth in 2024 and value growth of 23% in 2025 to RMB 216 trillion compared to 43% in 2024.

RMB on SWIFT

Historically, the majority of international payments by value have been made using the SWIFT network. SWIFT is a bank cooperative based in Belgium under the supervision of 10 central banks led by the central bank of Belgium, although its usage is dominated by the big US banks.

SWIFT is a messaging system, unlike CIPS which is a centralised RTGS clearing and settlement system. With SWIFT, clearing and settlement is conducted by individual correspondent banks through accounts they have with each other under bilateral agreements. SWIFT is used to send payment instructions between banks to move funds into and out of those accounts.

Whereas CIPS is used for RMB payments only, SWIFT can be used with any currency. Around 48% of international payments by value on SWIFT are in USD and just 2.9% in RMB4, down from 4.7% in December 2023.

As illustrated by the report in footnote 4, RMB payments on SWIFT are closely watched as an indicator of the internationalisation of the Renminbi, with SWIFT publishing a monthly RMB tracker5.

However, it seems few have noticed that with the ascendancy of CIPS, SWIFT is becoming irrelevant for RMB payments.

Conclusion

CIPS is a major source of international payments making the Renminbi a major international currency.

CIPS has grown strongly since its launch ten years ago which is likely to continue. One caveat is the accuracy of the data published by PBOC6 but China is the world’s largest exporter and it is reasonable to require payment in their own currency, so the published figures are plausible.

FXC Intelligence (footnote 2) forecasts international payments to reach USD 320 trillion in 2032. For 50% of this value to run on CIPS, CIPS needs to grow at only 27% CAGR (by value) compared to the 59% CAGR over the past eight years – it is well within reach of the Renminbi to replace USD as the dominant international currency.

CIPS seems to have gone unnoticed by payments and trade commentators, who instead focus on USD international payments, SWIFT and on other initiatives such as the mBridge7 cross-border CBDC project – however, CIPS has reached a size where it can no longer be ignored.

It must be time for the world to pay attention to CIPS and its impact on international payments.

PBOC Payment Report 2024: http://www.pbc.gov.cn/en/3688110/3688259/3689026/3706133/5188172/5649949/2025040114593718714.pdf

FXC Intelligence cross-border payments market size https://www.fxcintel.com/research/press-releases/new-data-cross-border-payments-market-now-worth-over-194tn-and-is-forecast-to-reach-320tn-by-2032

CIPS participants https://www.cips.com.cn/en/2025-07/07/article_2025070716092330204.html

SWIFT RMB tracker: https://www.swift.com/products/rmb-tracker

as an example, in the same report (footnote 1), figures suggest there are ten bank accounts for every person in China…

Project mBridge - no longer supported by the BIS but continued by the remaining participants including the PBOC: https://www.bis.org/about/bisih/topics/cbdc/mcbdc_bridge.htm