Trailblazer

The story of the UK's Faster Payments System - 18 years old in May

The UK’s Faster Payments system was the world’s first modern real-time interbank payments system. It went live on 27 May 2008 and turns eighteen this year.

Real-time account-to-account payments are ubiquitous today throughout the world but eighteen years ago they were unchartered territory - no-one knew if there was any need for them. Launching Faster Payments was a bold step into the unknown.

Why did the UK implement Faster Payments and how does it look today after eighteen years of operation?

To answer these questions, over three articles I look back at Faster Payments’ progress and consider the impact Faster Payments has made in the UK and beyond:

1. This article – the Faster Payments story since launch in 2008

2. Next week – Faster Payments volume/value growth history and forecasts

3. Third article – the impact of UK Faster Payments on the global payments industry and on UK payments

Faster Payments Origins

In the early 2000s, UK interbank payments operated on a three-day cycle and the UK banks were under pressure from the government (Office of Fair Trading) to speed them up1.

In response, the UK banks toyed with a proposal to reduce the three-day cycle to same-day or next-day but in the end opted for real-time. They saw an opportunity to re-use existing technology in place for ATM withdrawals and debit card authorisations that was real-time2. Also, they concluded that by going for real-time, they eliminated the risk of the government applying further pressure later on to speed up payments even more.

The project to design and implement Faster Payments started in 2005 and was driven by APACS3, the banking trade association for payments at the time.

Launch

The original launch date for November 2007 was pushed back to May 2008. All participating banks had to go live together but some were struggling to meet delivery milestones. This reflected the complexity of the programme and some requirements were dropped along the way to keep delivery on track.

The biggest casualties were the agency banks which historically used a sponsor bank4 to manage payments through clearing systems on their behalf. As the major banks went full throttle to meet the APACS deadlines, agency banks became a low priority. The net result was that payments from/to agency banks would be processed by their sponsor bank every two hours rather than in real-time – this situation still persists today but there are alternatives which I cover later.

Corporates were also affected by descoping. Initially, most banks planned to offer Direct Corporate Access (DCA) to Faster Payments, using Bacstel-IP5 to allow corporates to submit bulk payments directly into the central infrastructure. However, only Barclays implemented the service from the start and this was constrained by a £10,000 transaction limit6 which was too low to be of much use for many corporates.

The central infrastructure for Faster Payments was built by Vocalink who continue to operate it today (from within Mastercard, which acquired Vocalink in 2017). Vocalink was formed from Voca, which operated the batch clearing systems and Link7 which operated the ATM network. Faster Payments was built on technology similar to that used in the Link network.

The Early Days

After launch, APACS handed over management of Faster Payments to CHAPS. At the end of 2011, FPS Ltd (FPSL) was set up to manage the scheme and the contract with Vocalink, taking over from CHAPS. An interim CEO led FPSL until a permanent CEO was appointed in June 2012. The board of FPSL was made up of appointees from banks and, in line with industry best practice (PFMI principles), an independent chair and independent directors were appointed to the board in 2013.

FPSL transitioned into Pay.UK (together with Bacs and cheque clearing) in May 2018, which continues today to manage the Faster Payments scheme and contract with Vocalink.

Faster Payments was launched without fanfare8. Few banks had much idea of how it would be used or what the demand would be outside of standing orders. Although one bank made a point by making a £100 donation on the stroke of midnight on the launch date to the Disaster Emergency Committee to demonstrate money can move in real-time for crisis-response.

However, to this day, I am unaware of any consumer marketing by any bank for its Faster Payments service. Even now, 14 years after UK banks were required to use Faster Payments for online banking to meet the original PSD regulations, the vast majority of invoices and bills issued by businesses still have payment instructions that refer incorrectly to Bacs rather than to Faster Payments. The majority of the UK population seem to be familiar with the Bacs brand but have no or little knowledge of Faster Payments.

In 2008, real-time payments were so new to the industry and different to how banks previously operated, that Faster Payments took a few years to bed down properly. Although the central infrastructure operated 24/7, initially some banks connected to it only on a near-continuous basis. Participants were required to receive Faster Payments 24/7 from the start but it took a while for some to get going on the sending side. Some banks were unable to support out-of-hours processing and those that did still had overnight restrictions and downtime windows. Additionally, some used the SWIFT network to connect to the central infrastructure, locking themselves into SWIFT’s maintenance schedule, which routinely meant they had no Faster Payments connectivity for long periods over the weekend.

Gradually, scheme rules and infrastructure improved and progressively banks upgraded their systems and processes (e.g. for liquidity management to prefund settlement accounts efficiently). It was probably around 2011/2012 that Faster Payments became properly 24/7, real-time for most users.

As Faster Payments matured, the transaction limit was raised, first from £10,000 to £100,000 in 2010, to £250,000 in 2015 and to £1m in 2021 where it remains today.

The Faster Payments New Access Model

Over 18 years the Faster Payments system has matured with incremental enhancements - governance and rules have been tweaked (e.g. the limit changes), overlay services9 such as Confirmation of Payee and Request to Pay have been enabled and financial crime solutions such as the anti-money laundering Mule Insights Tactical Solution (MITS) and Corporate Fraud Insights have been added.

However, the Faster Payments architecture and scheme rules are fundamentally the same today as at launch.

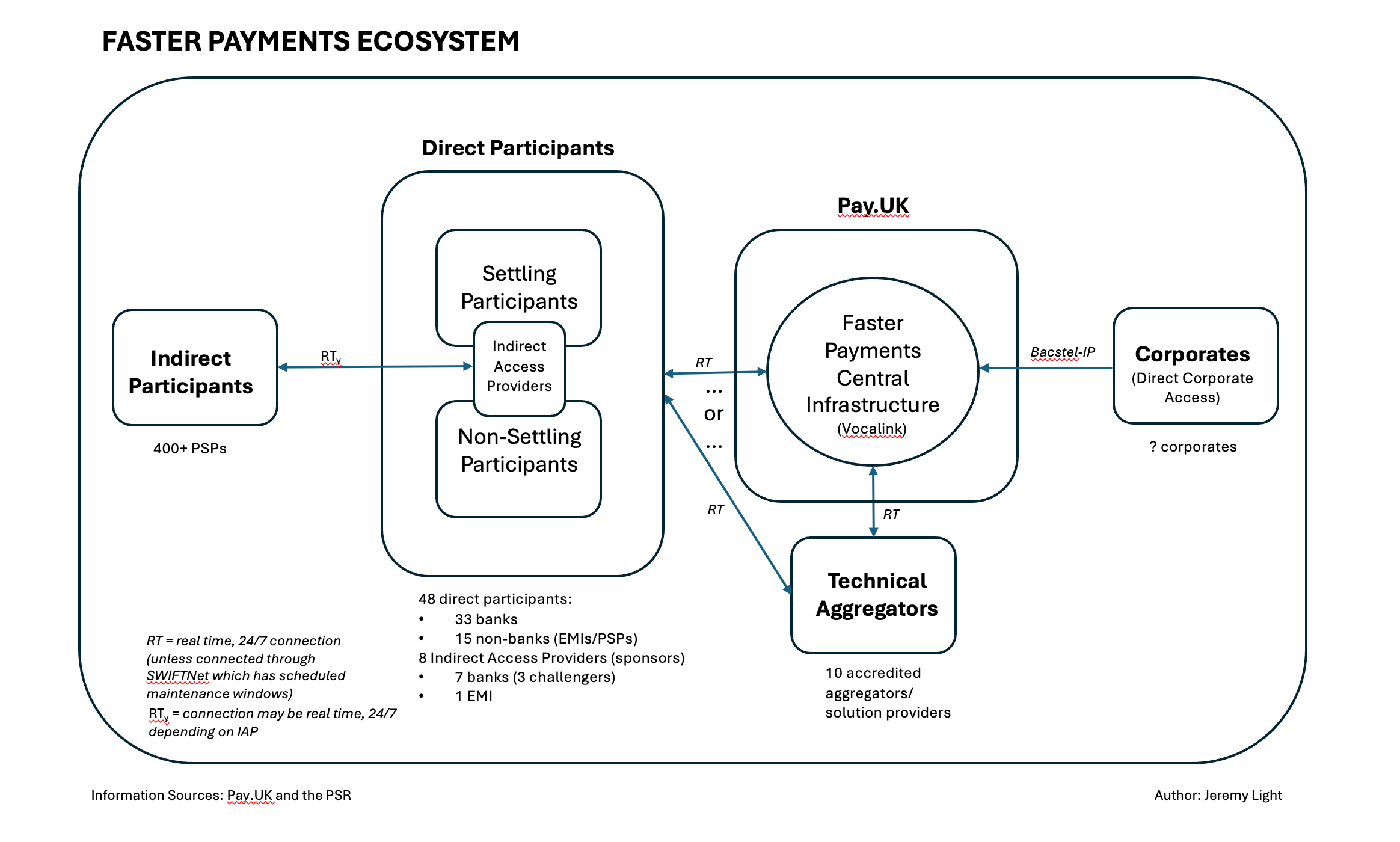

One key development which has had the biggest impact on adoption and usage is the New Access Model, developed to provide a level playing field for PSPs wishing to offer real-time payment services.

In its early days, there were just four sponsor banks10 that provided indirect access to Faster Payments. This was a core business for them, established over many years for access to the BACS, CHAPS and cheque clearing systems. The batch operations and technology needed for these systems were unsuited to Faster Payments real-time operations. However, none offered a real-time service to PSPs, only a two-hour service, the maximum time delay allowed by the scheme.

Faster Payments opted for a competitive model where PSPs requiring real-time payments could connect directly to the central infrastructure using technical aggregators instead of through a sponsor bank. The PSP would still need a bank to settle on its behalf but this could be any bank with a settlement account at the Bank of England, rather than one of the established sponsor banks. The idea was a technical aggregator could process transactions for multiple PSPs giving scale economies, allowing them to offer a lower cost per transaction than a sponsor bank. At the time, FPSL estimated a PSP with 1.4m to 13m real-time payments per year would benefit from using a technical aggregator instead of directly connecting itself.

It worked!

FPSL set up a Vendor Participation Programme in 2015 to encourage vendors to develop access solutions and a PSP Participation Programme to encourage PSPs to find and use a technical aggregator. FPSL had a target of three accredited vendors by the end of 2015 and 12 new PSPs by the end of 2016. Today there are ten accredited vendors 11 and 38 new (since 2014) directly connected PSPs12.

In parallel, FPSL worked with the Bank of England (BoE) on its proposal for non-bank PSPs to open settlement accounts, so that PSPs could prefund their real-time payments directly at the BoE rather than through a settlement sponsor. This gave PSPs full control over their intraday liquidity management and eliminated settlement dependency on other banks.

Adoption of this proposal was deferred from 2014 but in 2018 Transferwise (now Wise) became the first non-bank to get a settlement account, on 13 April 201813. As a result, as shown in the heading diagram, there are two types of direct participants – settling participants who have a settlement account at the BoE and are directly connected to the central infrastructure; and non-settling participants who are directly connected but use another bank with a settlement account to settle on their behalf.

Neither the BoE nor Pay.UK publish a list of non-banks with settlement accounts but Pay.UK does publish a list of direct participants (footnote 12) which contains 15 non-banks (EMIs and payment institutions). I expect that many of these may have settlement accounts at the BoE, including Modulr, an EMI which also is the only non-bank providing indirect access services to other PSPs.

One restriction on opening settlement accounts was the limited availability of “go-live” weekends using the BoE’s RTGS system which holds the accounts. With the new RT2 RTGS implemented in April last year, this constraint should disappear and the opening of settlement accounts should accelerate.

Overall, the New Access Model was a success and has enabled a more level playing field for PSPs. A vibrant ecosystem is in place (see the heading diagram) where bank and non-bank PSPs have competitive offerings for real-time payments, with a set of accredited vendors competing to enable those offerings.

Conclusion

In 2008, launching Faster Payments was a leap into the unknown. Real-time interbank clearing systems may be common across many countries now but most have been implemented in the past ten years with the benefit of learning from the early adopters14. In contrast, the UK’s Faster Payments had a blank sheet and was driven by government pressure rather than by a vision.

However, it has worked out well.

Faster Payments is still operating after 18 years using an architecture and rules that are much the same as at launch and volume is still growing at over 10% annually. This is a testament to the strong product-market fit it achieved from the start and which continues today.

To my knowledge, Faster Payments has had only one serious outage15 in otherwise continuous operation, 24 hours a day for 18 years. This is a testament to the robustness and reliability of the design of the central infrastructure built and operated by Vocalink.

I’ll cover key learnings in a later article but one learning is that the traditional topologies for indirect access to clearing that have served multiple ACH and RTGS systems in many countries for decades are unsuitable for high volume, real-time, 24/7 clearing. Direct access is necessary.

As its eighteenth birthday nears, it is clear Faster Payments needs an upgrade to meet the needs of the digital economy.

However, without doubt it is correct to say Faster Payments has been a true trailblazer in real-time payments.

Addenda - added 22 Mar 26

A practitioner at the heart of a sponsor bank’s Faster Payments (intense) programme in 2008 (and prior) has provided this interesting clarification:

“The indirect model (from the existing 4 sponsor banks) was in the competitive space, and access via a sponsor was done in several ways. My bank offered SWIFT MT103 which gave near real time speed on a 24/6.66 basis (SWIFT maintenance window for 6 hours every Sunday) and as an alternative, Standard18 file upload/download whereby each agency bank could select which hour(s) they wanted to receive credit information - so could be hourly 24/7 or any frequency down to 1 per day. Also sponsor banks offered access via their own direct channels with real time advices etc. The biggest issue was that (at the time) very few agency banks could handle more frequent files than daily as their back end platforms were designed to consume daily Bacs files and not real time. So capability was provided by (some) clearing/sponsor banks but not consumable due to legacy infrastructure at the agencies.”

I expect that all Faster Payments sponsors, or Indirect Access Providers use settlement accounts at the BoE, therefore they are settling participants in the Faster Payments scheme. However, since no information is published on direct participants who use settlement accounts, I have shown IAPs straddling both settling and non-settling direct participants in the diagram above.

However, payment speed was mostly invisible to consumers (there was no internet or mobile banking) apart from standing orders (recurring payments for rent, mortgage, subscriptions etc) where payments deducted from an account were credited to the receiver three business days later. Banks were perceived to be taking advantage by holding onto consumer funds and often, consumers were caught out missing payment due dates by up to seven days (over weekends and holidays). Direct debits and credits (payroll, bill payment etc) also took three days to process (and still do with Bacs) but the debiting of the sending account and crediting of the receiving account take place at the same time on the third day.

Use of the CHAPS RTGS system was also discounted. Although a same-day payments system, it was unsuited to high volumes of transactions (due to technology constraints and liquidity management complexity) and is cost effective only for high-value payments.

APACS has morphed over time, first into the Payments Council, then Payments UK which has been combined since with other associations into UK Finance.

Sponsor banks are also termed Indirect Access Providers (IAPs) by UK regulators.

Bacstel-IP was launched in March 2003 to allow corporates to submit direct debit and direct credit files created in their ERP and AP systems directly into Vocalink.

Banks also set their own limits within the scheme limit – I recall that at launch, Abbey National had a limit of just £1!

The LINK scheme is a separate company to Vocalink – Vocalink operates the ATM infrastructure for LINK, which manages the scheme rules and use of the network.

In part because two months earlier in March 2008, the widely publicised debacle at Terminal 5’s opening at Heathrow had just occurred and no one in the Faster Payments programme wanted to repeat a “T5 moment”.

The Paym mobile payments overlay service was also launched using Faster Payments in April 2014 but was withdrawn in March 2023.

The long-established sponsors were Barclays, HSBC, Lloyds and NatWest; there was a fifth sponsor bank, Co-op but the regulator was concerned by their operations and requested the bank to withdraw from the agency market.

Faster Payments accredited vendors: https://www.wearepay.uk/what-we-do/third-party-assurance/technical-aggregator-solution-providers-and-consultants/

Faster Payments directly connected participants (there were 10 in 2014, 38 new since, 48 in total): https://www.wearepay.uk/what-we-do/payment-systems/faster-payment-system/payment-system-participant-list/

Bank of England non-bank settlement accounts - https://www.bankofengland.co.uk/news/2018/april/non-bank-psp-access-to-the-payments-system-announcement

Other early adopters were China (IBPS – 2010), India (IMPS – 2010) and Poland (Elixir Express – 2012).

Faster Payments outage 2018 - https://thepaypers.com/payments/news/faster-payments-outage-cause-still-unknown-as-companies-asses-damage

Great piece Jeremy - it was my privilege to be the first CEO of Faster Payments Scheme Limited - did you notice that the FPS company name had Scheme in the singular yet Bacs had the word Scheme in the plural - a (naughty) but conscious decision I made!

Thanks Jeremy. A great trip down memory lane.