The Only Way is Down

Myth or fact – are there negative externalities from reducing credit card fees?

At a recent Senate hearing on competition in the US credit card market1, Chris Callahan, co-owner of a bookstore in Cambridge, NY stated his business pays 3.8% on credit card payments, up from 2.4% in the past.

Many of his customers rely on the convenience of paying by credit card, so he has no choice but to accept them – he describes it as a cost of convenience, a silent tax he has no control over, constituting his fourth highest operating expense after payroll, rent and shipping.

It is a situation that is being played out across the 33m small businesses in the USA. As Mr. Callahan observes, main street businesses like his bookstore “cannot take it any longer”.

Interchange

At the heart of the issue are the interchange fees paid to banks that issue credit cards. This fee is one component of the swipe fee, or merchant service charge (MSC) which businesses like Mr. Callahan’s pay to a merchant acquirer on every card transaction, to process it. The other components are the acquirer’s own fee and a network fee (Visa, Mastercard etc).

While the acquirer sets its own fee (and businesses can shop around to find the best or negotiate their own, if large enough), the interchange fee and network fee are set by the networks. The acquirer has no control over them but must collect them from its customers. Thus, each component of the MSC has separate competitive dynamics, complicating competition.

At the end of this article, I provide more detail on interchange, its original purpose as an incentive and why it complicates competition.

The Credit Card Competition Act

To address this situation, US lawmakers are proposing a bill, The Credit Card Competition Act (CCCA)2 to introduce competition into the credit card market.

Banks and card networks oppose the bill and retailers support it, generating a heated debate.

In the rest of this article, I list ten claims debated about the negative externalities of credit card fees and the negative externalities of reducing them. For each, I provide analysis and a verdict on whether they are a myth or fact.

1. The card networks (Visa, Mastercard etc) are the direct beneficiaries of interchange, at the expense of retailers

Although the card networks set interchange rates, they receive no interchange themselves. Retailers fund the interchange (through the MSC) and the banks that issue cards receive all of it.

Separately, the card networks set a network fee, charged also to retailers through the MSC, which only the card networks receive. However, network fees are much lower than interchange fees, typically only 1/10th the amount for US credit cards.

Verdict: MYTH

2. Credit card fees are inflationary

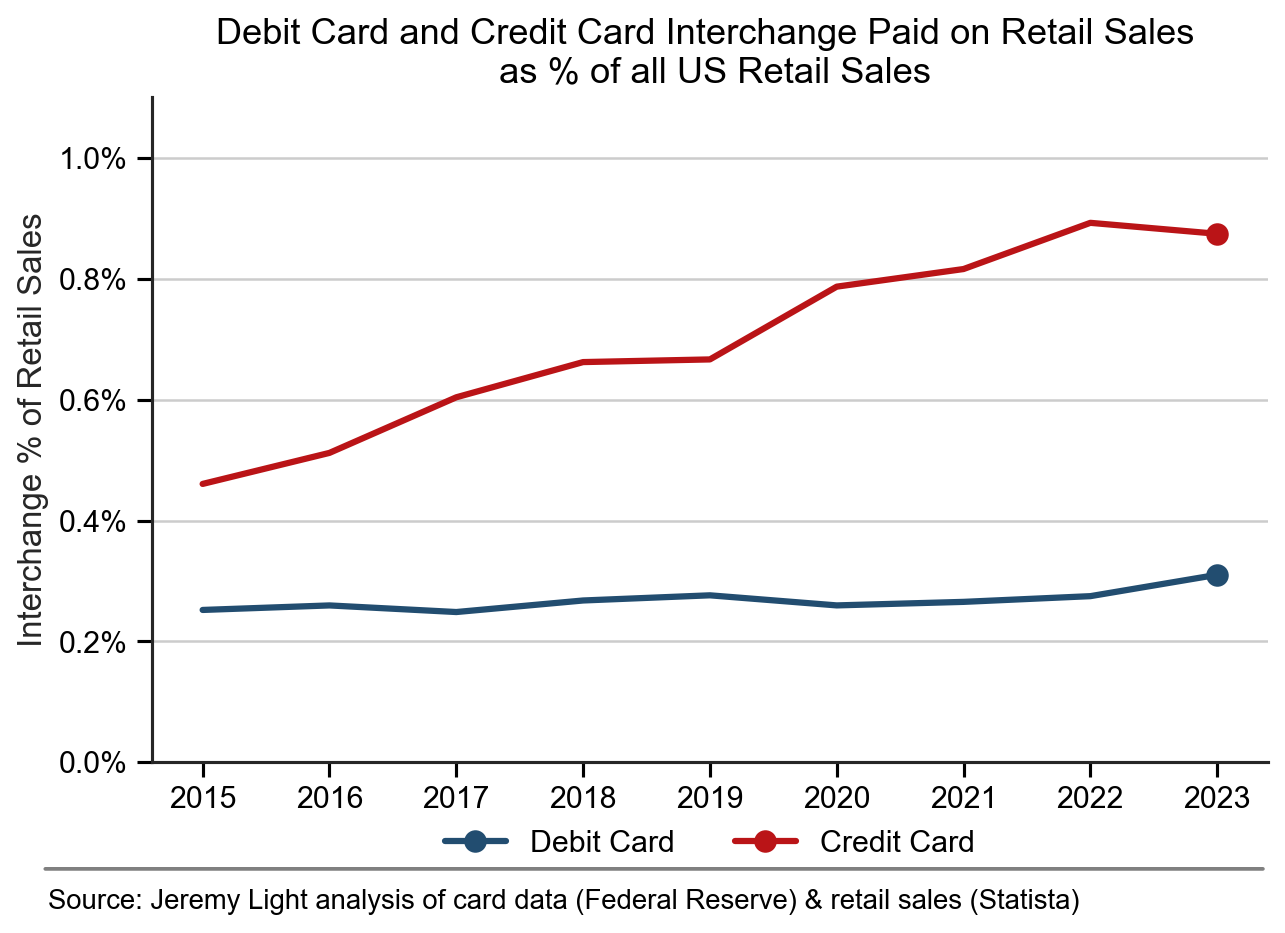

Figure 1 shows debit card and credit card interchange in retail sales as a proportion of total retail sales (paid by all payment methods) between 2015 and 2023. In the period, US retail sales increased from $4.7trn to $7.2trn3, the credit card interchange paid by retailers trebled4 and the proportion of credit card interchange in retail sales almost doubled from 0.46% to 0.87%.

Figure 1 – interchange from retail card purchases as % of all US retail sales

If all the credit card interchange paid on retail sales was added into retail sales prices, it would have added only 0.41% to prices, far lower than the 29% increase in CPI5 over the period. It is true that if credit card interchange was removed, there would be roughly a 0.9% drop in prices – but that would be a one-off occurrence.

As a percentage fee, credit card interchange in $ terms rides up with price inflation, but it has made virtually no contribution to it.

Verdict: MYTH

3. Credit card fees hinder businesses from growing

Companies grow by investing their profits back into the business – operating margins are therefore important for growth.

A low margin business such as a gas station has a net profit margin of around 2%6. If it accepts cards, it is funding on average across all its gas sales, 0.87% in credit card interchange and 0.37% in debit card interchange (see Figure 1), or over 1% of sales in interchange in total i.e. if it paid no interchange, its profits would be more than 50% higher. For a sale paid by credit card, a 2% interchange would halve any profit on that sale.

Thus, it is difficult for a gas station to grow its business - if it refuses to accept cards, it limits sales and if it accepts them, it makes tiny profits on sales where credit cards are used. This is why it is common in the USA to see gas stations offering discounts for cash.

This is less of an issue for a higher margin business, say with net profit margins of 10%, but even so profits would be higher without card interchange – card interchange eats into the margins of all businesses, resulting in less profit to reinvest for growth.

Verdict: FACT

4. High credit card interchange fees reduce merchant acquiring competition, inflating merchant acquiring fees

Table 1 compares the average credit card MSC and its components for the USA, UK and Europe. It shows each of these fees in the USA are much higher than in the UK and Europe.

It is a mistake to believe that this is because UK and European regulation keeps MSC rates artificially low. Only the interchange component is regulated, max 0.3% for credit cards. The network fee and acquiring fee components are unregulated. The acquiring market in the UK and Europe is fiercely competitive, with acquiring fees averaging 0.15%, less than half the 0.33% in the USA, suggesting the USA has a less competitive acquiring market than Europe. Network fees are also higher in the USA.

Table 1– credit card merchant service charge (MSC) and its components, expressed as an average percentage of total transaction value in different countries/regions (sources: CSMPI7 USA and EU, PSR/my analysis UK)

It is reasonable to conclude that by regulating interchange, the non-competitive component of the MSC, a competitive acquiring market has developed in the UK and Europe; while in the USA, much higher interchange rates have seeped into higher network and acquiring fees, indicating a less competitive market.

This is a problem especially for small businesses who lack the scale to negotiate acquiring fees and pay high acquiring fees on top of high interchange and network fees (Table 1 shows average rates which include rates for very high-volume businesses which get lower fees).

As a result, small US businesses can pay very high MSC fees in total, like the 3.8% paid by Mr. Callahan, which is a huge drag on any business. In comparison, a similar small business in the UK can pay (Revolut8) as low as 0.86% in-store and 1.6% online for an average $43 (£34) card transaction.

Verdict: FACT

5. High swipe fees for cards deter innovation in alternative payment methods

In the USA, the main alternative payment methods that compete with cards are PayPal (including Venmo) and Zelle. However, their market penetration is only a small fraction that of cards. See previous article.

High card interchange rates encourage innovation in card-based solutions – it guarantees an immediate revenue stream which is why many Fintechs innovate around cards. For example, while Zelle is an account-to-account payment system, its parent company (EWS, bank-owned) launched the Paze digital wallet this year to compete with other wallets such as PayPal – rather than using the Zelle system, Paze is a digital wallet for credit cards and debit cards.

Elsewhere, where card fees are low, alternative payment methods to cards have developed strongly – for example, in Europe: Bizum, Blik, iDEAL, MobilePay, Swish, Twint, Vipps; in Asia: Alipay, Paytm, PhonePe, Promptpay, Wechat.

Verdict: FACT

6. Reducing credit card fees will lead to a loss of reward benefits

The source of funds for rewards programs are interchange revenue and net interest margin on revolving credit balances.

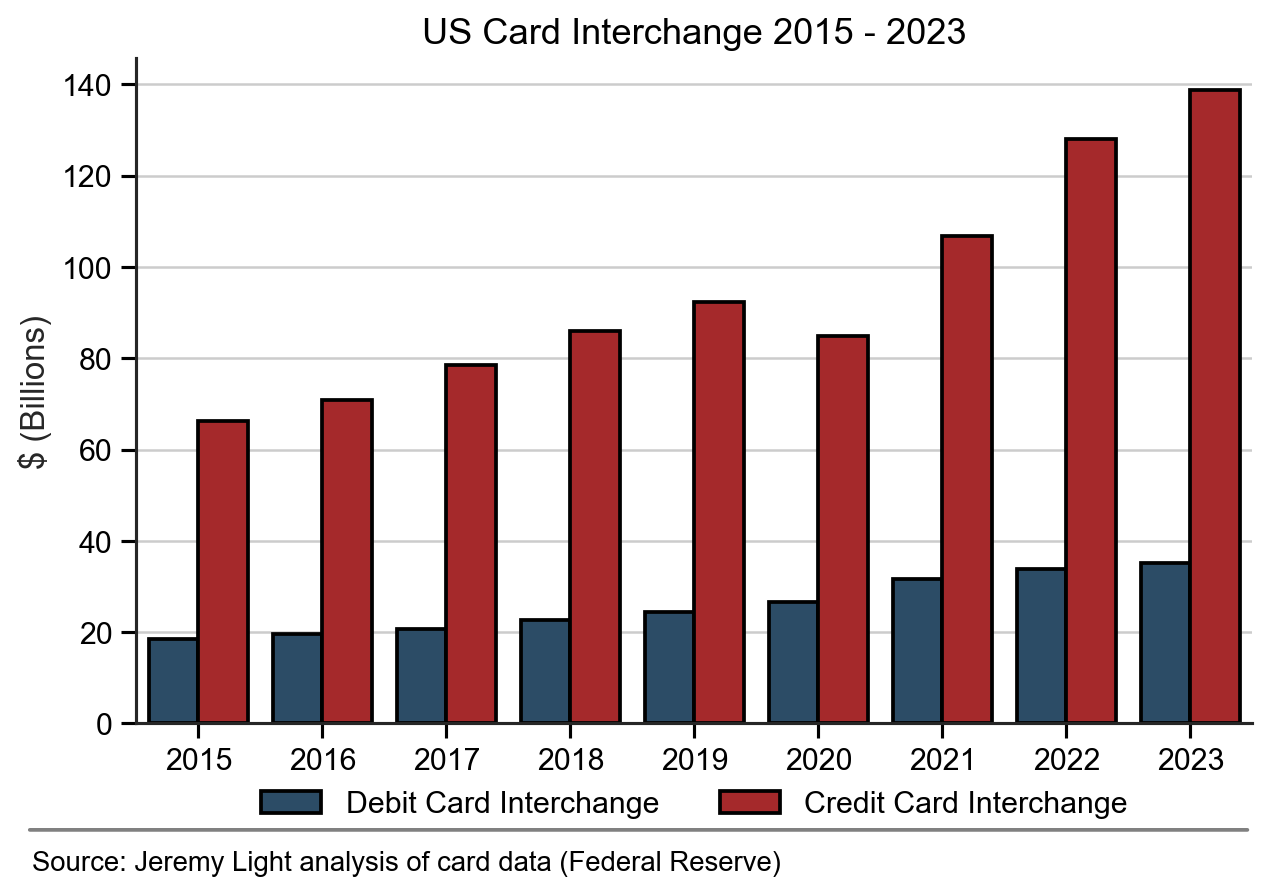

I estimate in 2023, US card issuers received $35bn in debit card interchange and $139bn in credit card interchange9, which has more than doubled since 2015 – see Figure 2.

There is plenty of interchange revenue to fund credit card reward programs, much less for debit cards which have far fewer and less generous rewards programs than credit cards.

Figure 2 – US interchange

One estimate10 puts the annual costs of US rewards programs at $41bn, which is just 29% of the $139bn in credit card interchange revenue. Competition would have to be fierce to drive down interchange to a point where credit card rewards programs would be threatened, by at least 50%, which is unlikely. Figure 2 also shows that credit card interchange in 2023 was over double that in 2015 when rewards programs were as embedded in American society as they are today.

Verdict: MYTH

7. Allowing retailers to choose a network will give consumers less choice in how they pay

Under the CCCA, retailers may accept Visa, Mastercard and other brands such as Discover and Amex unless they choose otherwise, as is the case today. It is unlikely that retailers will refuse to accept Visa or Mastercard as doing so will prevent them selling to a large percentage of potential customers. A retailer choosing to route payments to a non-affiliated network should cause no change to a consumer’s choice of card they use.

Verdict: MYTH

8. Consumers will see no benefits from reduced credit card fees as retailers will pocket the savings

Retailers can pass benefits to consumers from reduced credit card fees in the form of reduced prices, improved service, a better range and quality of products or business expansion – there is no law of economics or retail that says prices must be reduced when costs fall. Supply and demand are the drivers of price.

Retailers could, of course pocket the savings to increase their margins – where credit card transactions cause low margins, as in the gas station example, that is to be expected. Since all retailers benefit from any reduction in credit card fees, in a competitive market, all else being equal, any excessive margin increases will get competed away.

Verdict: MYTH

9. Consumers have lost out from similar debit card regulation in 201011

Figure 1 shows that debit card interchange paid on retail sales as a proportion of all retail sales (paid by all payment methods) has remained constant in a range between 0.2% - 0.3% between 2015 and 2023. Although retailers bear the cost of interchange, indirectly it is paid by consumers – thus the two-network requirement and fee cap introduced by the Durbin amendment has benefited consumers indirectly by keeping a lid on debit card interchange.

As explained in point 6, rewards programs on debit cards are less generous than on credit cards as there is less interchange revenue to fund them. By limiting debit card interchange, almost certainly the Durbin amendment has prevented debit card rewards programs from developing, implying that consumers have lost out.

However, even though rewards programs are engrained in US culture, their net benefit to consumers is questionable. While the collection of interchange is uniform with each card transaction, the use of the rewards varies depending on individual consumers – some benefit more than others.

This is borne out by a Federal Reserve study12 which estimated “an aggregate annual redistribution of $15 billion from less to more educated, poorer to richer, and high to low minority areas” through reward programs.

Verdict: MYTH

10. Using multiple networks to route card transactions exposes consumers and retailers to security risks

All payment networks must be secure otherwise they get fined by regulators and will go out of business – compliance with standards such as SOC 2, ISO27032, ISO27001, PCI-DSS is a pre-requisite for any network. There is no reason to believe routing to multiple networks introduces security risks – on the contrary, it improves resilience.

Verdict: MYTH

***************************************************************************

Incentives and the Interchange Fee

The original purpose of the interchange fee in the 1960s was to incentivise banks to issue credit cards to grow the card networks. Banks were rewarded for encouraging their customers to use a credit card, receiving a welcome new revenue stream from interchange – it worked spectacularly.

The original incentive for retailers to accept credit cards was incremental sales. It made it easier for consumers to pay and to borrow, if needed, to make a purchase, boosting sales. Evidently, this also worked, with retailers accepting cards at scale.

Since interchange is an incentive13 to use a network, competition serves only to increase the fee – for example, if Visa encourages a bank to issue Visa cards with an interchange of 2%, Mastercard can win over the bank by setting its interchange higher at 2.5%, at zero cost to them, as the retailer bears the cost. The only limitation on the rate is retailers may start refusing cards or surcharging for them if too high. Networks tend to set interchange for each card product (standard, gold, corporate etc) and the typical ranges published14 suggest that 3.3% is an upper limit.

However, for retailers, cards no longer generate incremental sales – today, with 77%15 of retail sales made by card, retailers have no option but to accept cards.

The retailers’ incentive has gone while the card issuers benefit still from the interchange incentive even though they no longer need incentivising. The market is saturated, with US consumers having an average of three credit cards each16.

Further, rewards programs may incentivise Americans to enrol for new credit cards with no need to do so and to spend more than they can afford – as a result, US credit card debt is $1.17tn dollars up from around $765bn at the beginning of 2021 (go to 1:42:00 in the Senate hearing video in footnote 9).

The interchange fee complicates competition, as acquirers are unable to negotiate it with networks. Also, retailers are unable to negotiate it with acquirers and retailers are unable to choose the network which sets the interchange, as this is determined by the card a customer presents to them. This dynamic will still exist if the CCCA passes, as card issuers are likely to choose a second network with the highest available interchange rates.

MSCs are sometimes quoted as ‘interchange++’ to separate out the acquirer’s fee component which large retailers can negotiate, but even so they can negotiate only the acquirer’s portion of the MSC, rather than all of it.

In summary, competition is unable to drive down interchange, instead, it drives it up.

Finally, card networks are in a bind even if they want to reduce interchange – they are unable to collude for anti-trust reasons, but if one moves on its own, there is a risk their card issuers will shift their cards to other networks.

Please message me if you have questions or comments.

Also, I would be delighted to receive your suggestions for future articles.

Senate hearing 19 Nov 24: https://www.c-span.org/video/?540086-1/hearing-improving-competition-credit-card-market#

The Credit Card Competition Act: https://www.congress.gov/bill/118th-congress/senate-bill/1838/text. A bill to give retailers a choice of two or more card networks to process a credit card payment, with at least one having no affiliation with Visa or Mastercard.

Assumes (my estimate) 20% of retail sales were paid by credit card in 2015 and 37% in 2023, with an average interchange rate of 2.36% (source CMSPI – footnote 7), giving $22bn of credit card interchange in 2015 and $63bn in 2023 (assuming the interchange rate was constant over the period – it is likely to have increased a little, but no data is available)

US inflation calculator: https://www.in2013dollars.com/us/inflation/2015?endYear=2023&amount=1

I estimate average debit card interchange is 0.79% from Federal Reserve Reg ii reporting data, applied to $4.5trn of debit card value and assumed 2.36% (source CMSPI – footnote 7), credit card interchange applied to $5.9trn credit card value in 2023

Senate hearing: 1:04:00 https://www.c-span.org/video/?540086-1/hearing-improving-competition-credit-card-market#

Durbin Amendment - Dodd–Frank Wall Street Reform and Consumer Protection Act 2010

Who pays or your rewards?: https://www.federalreserve.gov/econres/feds/files/2023007pap.pdf

Some networks call interchange a “reimbursement fee” to compensate issuers for growing the network. Some stress that it is merchant acquirers who pay interchange rather than retailers (but retailers bear the cost).

Based on analysis of the findings of the Feds Consumer Choice report https://www.frbservices.org/binaries/content/assets/crsocms/news/research/2024-diary-of-consumer-payment-choice.pdf