The Landscape is Changing

Countries leading adoption of real-time payments and laggards

Payment practitioners like to observe that consumer payment habits and preferences are local, with requirements unique to each country. Consequently, payment service providers are sensitive to country habits and preferences, to get product-market fit and adoption of their payment products and services.

But is it true that all countries are different or is it just an observation of the present and recent past?

After all, card payments are much the same wherever you go in the world, with standardised rules, branding and processing from the international card networks, among others.

And before card payments appeared in the 1960s, for centuries the world over, the only mass payment method was coins and to a certain extent, bank notes (ignoring cheques). Presumably, consumer habits when using coins and bank notes would have been similar regardless of country, with key factors being the same such as convenience, cost, access and trust (for coins: the type of metal, its purity and weight; for notes their redeemability for coins/precious metal).

My observation is that while there may be local factors such as technology and regulations, specific mainly to electronic payments, globally, there are just three payment methods that matter and each is similar in every country:

Cash

Cards (debit cards, credit cards, charge cards, pre-paid cards)

Real-time electronic payments, made using digital wallets and online/mobile banking.

These three methods are common to every country in the world, with varying degrees of relative usage.

Real-time Electronic Payments

With cash in decline and cards at, or near a peak in usage, eventually only real-time electronic payments will dominate in all countries. These are account-to-account payments where the account may be a bank account, non-bank payment/e-money account or some form of wallet account using stablecoins or other form of digital asset.

Figure 1 shows how these real-time account-to-account payments have penetrated payment landscapes in eight countries and regions around the world, presented in terms of real-time payments per capita as a normalised comparator1.

Figure 1 – real-time payment volumes per capita in selected countries around the world2

I have selected the countries and regions shown in Figure 1 as a sample of those with established real time payment systems. China is missing as I am unable to find volume data for Alipay and Wechat Pay, the two non-bank digital wallets accounting for over 90% of mobile payments in China with 2.5 billion users between them3.

In the sample in Figure 1, Thailand, Brazil and India lead the way. Countries where card payments dominate lag far behind such as UK, Australia, USA and the Euro Zone.

No correlation is apparent between real-time payments per capita and card payments per capita for each country when I plot the two. This may explain the perception that consumer payment habits and preferences are local, specific to each country. Each country has developed its payment systems separately and consumers use just what is available to them – e.g. the USA is heavily card-centric due to the high interchange incentives for banks to issue both debit cards and credit cards, with widespread rewards programmes that attract a strong following from consumers. Whereas, in Thailand for example, take-up by both consumers and merchants of Promptpay (available since 2016) is widespread due to the convenience and low/zero cost of acceptance.

Correlations Between Payment Method Usage

However, when plotting the total combined payments per capita for real-time payments and cards against cash usage for each country, there is a very strong correlation – see Figure 2.

Figure 2 – Combined real-time and card payments per capita versus cash usage4

This suggests that consumers exercise a straight choice between using either cash or an electronic alternative, but the electronic alternative they use is dictated more by what is available than by choice (with typically banks determining what is available).

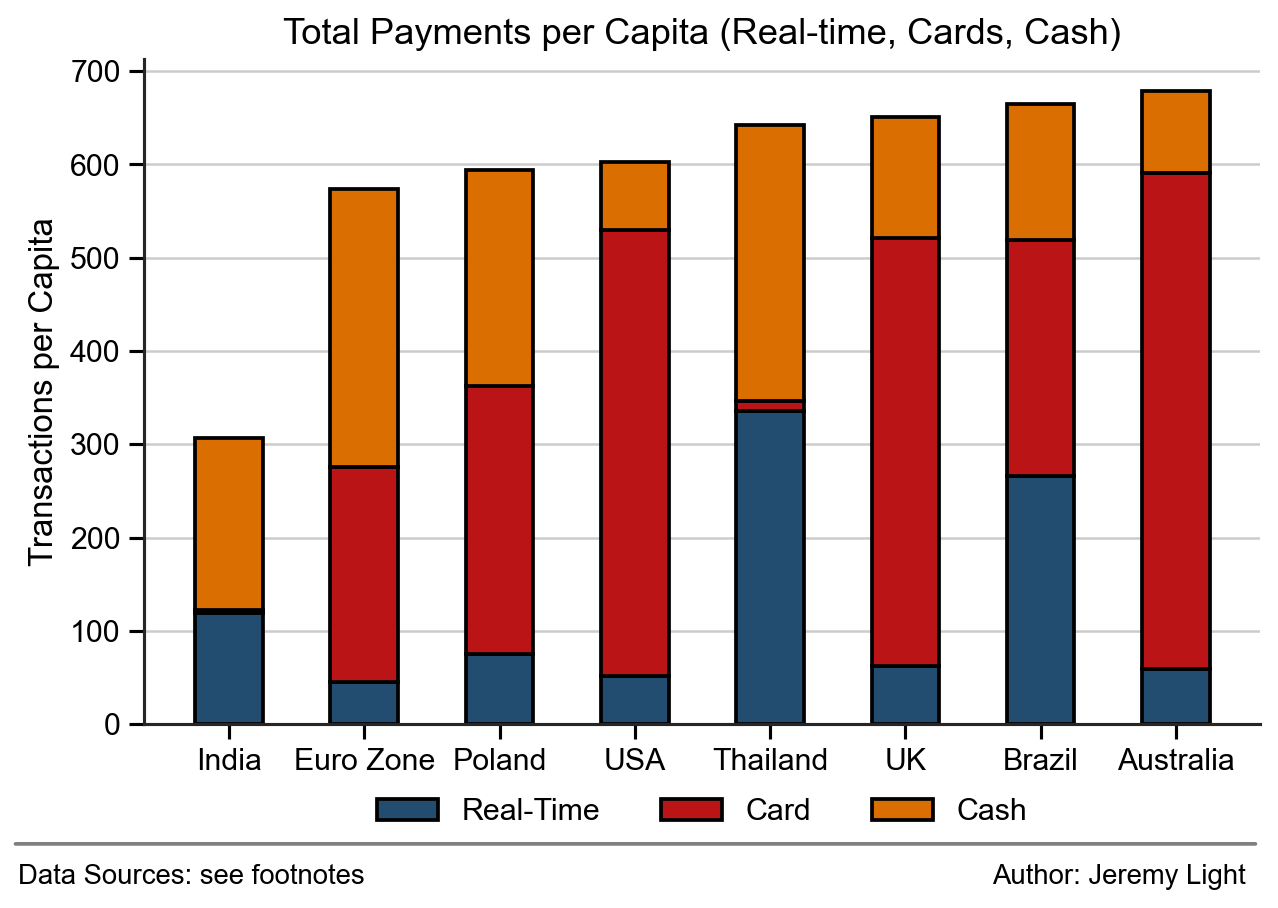

Figure 3 shows the total payments per capita combined for real-time payments, cards and cash for the countries in the sample. While there is no discernible pattern in the mix of payments in each country, the total number of payments per capita (per year) is remarkably similar, except for India, in a range of 574 – 679 payments per capita, averaging 630. This is across seven countries with a combined population of 1.1bn and a wide range of GDP per capita.

The trend line in Figure 2 reinforces this observation – extrapolating it back to the y-axis, equivalent to 0% cash usage, gives 685 payments per capita.

Figure 3 – Total payments per capita across real-time payments, cards and cash

India is an outlier - possibly due to data quality. The real-time payments and cards data provided by the Reserve Bank of India and NPCI are thorough and detailed, but the cash usage figure of 60% reported in the press may be too low5. If this is raised to 80%, India’s total rises to 614 payments per capita, in line with the other countries. It also increases the R2 (a measure of the fit with the data) of the trend line in Figure 2 from 95% to 98% and it tallies with the two-fold increase in cash-in-circulation in India since 20166 suggesting cash usage continues to be very high despite massive UPI volumes.

Indeed, in Figure 2, if the India cash usage is increased to 80% and a notional country is added to the graph with 100% cash usage and zero electronic transactions, the R2 of the trend line increases to 99% and intercepts the y-axis at 643 electronic payments – correlating nicely with the data from the other countries in Figure 3.

It looks like cash usage in India is understated, which as we shall see in the next section implies that UPI volumes, already the biggest in the world (after China, probably) have still a long way to go.

The Growth Potential of Real-time Payments

My hypothesis is that eventually, only real-time electronic payments will dominate in all countries, delivered through digital wallets (bank and non-bank).

On the assumption that this means 87% of all consumer payments are made this way, based on 1% being cards and 12% cash (both figures being the lowest in the sample, respectively for Thailand and USA), Table 1 shows the resulting real-time payment volumes to expect in each country and the multiple of current real-time volumes to get there.

Table 1 – Current and forecast real-time payment volumes

Table 1 shows also the most recent year-on-year growth in real-time volumes for each country and the number of years to get to the 87% share using this growth rate. The leaders, India, Brazil and Thailand will get there within two years or so, while the laggards, due to the dominance of the card networks will take 11 – 16 years, with the USA the last to close the door on cards.

The Path to Real Time Payments Globally

I expect that consumer payments will become similar in all countries around the world, with cards payments handing the baton to real-time, account-to-account payments delivered through digital wallets7. India, Brazil and Thailand among others are already a long way down the road towards this vision. Within two to three years real-time payments in these countries will account for almost 90% of all consumer payments. Payment volumes, already high could double from where they are today. In India’s case, the volume increase could be even higher reaching almost 800bn UPI payments annually.

This may seem far-fetched, but these countries already have remarkable real-time payment systems processing huge volumes that far exceed those in Europe, the UK, Australia and the USA – the numbers speak for themselves.

The key reasons why real-time payments will dominate is the user experience and flexibility when using them with digital wallets, which consumer love, together with the low risk of unauthorised fraud; and the low cost of acceptance which merchants love. Apple Pay and Google Pay provide a fantastic user experience for cards, but this is easily replicable in digital wallets for real-time payments, which are also much cheaper and versatile for merchant acceptance.

These factors are independent of the form of money used for payment. Although, most real-time payments today are made using bank deposits and e-money, stablecoins or CBDCs could be used in the future. However, I expect bank deposits and e-money backed by bank deposits to prevail – stablecoins are suited best for cross-border payments, while CBDCs will struggle to get public acceptance due to privacy and trust concerns (even if central banks manage to get the user experience right).

Real-time payments adoption in Europe, USA, UK and Australia will continue to be slow, but the potential growth in these countries is enormous and has still to happen. There is no sign of it yet in the UK, but Europe looks promising with the Wero digital wallet launched last year. Also, country-specific digital wallets with real-time payment are proliferating there – in addition to Blik in Poland, others are equally popular such as Bizum in Spain, Swish in Sweden and Twint in Switzerland. The USA has a healthy selection of digital wallets with PayPal/Venmo, Zelle and CashApp, but they face a long uphill struggle against cards which are heavily entrenched.

Poland is one to watch – although real-time payment volumes there are only a quarter of cards, Blik is growing strongly. It could tip the balance to real-time payments from cards, accelerating real-time payment adoption. This happened in Brazil with Pix and if it happens again in Poland, it points the way to cards being tipped elsewhere, rapidly reducing the time to full adoption of real-time payments shown in Table 1.

Conclusion

I will provide an update next year to see how the real-time payment landscape depicted here has changed. With growth rates in some countries over 50% on volumes running into billions of transactions, the global landscape is changing fast.

Overall, the data is clear – Brazil, India and Thailand (and others) are leading the way with real-time payments delivered through digital wallets and they are steaming ahead, way in front of the pack.

However, there remains significant scope for Australia, Europe, UK, USA and other countries where cards are widely used to go all-in on digital wallets and real-time payments. It is time for them to seize the opportunity.

Cash will always be in demand, albeit eventually in very limited amounts, but the days of the card networks are numbered, 15 – 20 years at most, possibly much less.

I prefer to use the number of payments as a comparator, as each payment is a user interaction to buy something or transfer funds, whereas analysis using $ values is obscured by different GDPs per capita and currency purchasing power.

Sources for the real-time payments data in Figure 1 are:

a. Eurozone: https://www.ecb.europa.eu/press/stats/paysec/html/ecb.pis2024h1~5263055ced.en.html#:~:text=In%20the%20first%20half%20of%202024%2C%2034%20retail%20payment%20systems,euro%20area%20retail%20payment%20systems

b. USA: - PayPal: https://s201.q4cdn.com/231198771/files/doc_financials/2024/ar/PayPal-Holdings-Inc-Combined-2024-Proxy-Statement-and-2023-Annual-Report.pdf

Zelle: https://www.zellepay.com/press-releases/zelle-soars-806-billion-transaction-volume-28-prior-year

- TCH: https://www.theclearinghouse.org/payment-systems/rtp

- CashApp: https://www.businessdasher.com/cash-app-statistics-and-facts/#cash-app-statistics-the-key-data

c. Australia: https://www.rba.gov.au/payments-and-infrastructure/resources/payments-data.html

d. UK: https://www.wearepay.uk/what-we-do/payment-systems/payment-statistics-overview/

e. India: https://www.rbi.org.in/Scripts/PSIUserView.aspx?Id=44

f. Brazil: https://www.bcb.gov.br/en/financialstability/pixstatistics

g. Thailand: https://www.bot.or.th/en/statistics/payment.html?keyword=promptpay+statistics

h. Poland: : https://nbp.pl/en/payment-system/statistical-data/

The sources for the cash usage data in Figure 2 are:

b. USA: https://capitaloneshopping.com/research/cash-vs-credit-card-spending-statistics/

f. Brazil https://www.cashmatters.org/blog/cash-accounts-for-22-percent-transaction-value-in-brazil

g. Thailand: https://www.cashmatters.org/blog/cash-accounts-for-46-percent-transaction-value-in-thailand

h. Poland: https://www.cashmatters.org/blog/in-poland-cash-is-used-for-39-of-pos-transactions

footnote 4 has the link for the India cash statistic. It is possible that the 60% figure is by payment value rather than volume and that by volume the % share is higher.

see previous article on payments and cash in India: https://jeremylight.substack.com/p/sailing-to-the-moon?r=axqgy

Visa and Mastercard appear to realise this and are hedging their future by being very active in account-to-account payments. Among other things, Visa owns Tink an open banking provider, is about to launch Visa A2A and the Visa Direct business is growing rapidly, passing 10bn transactions in 2024; Mastercard owns Vocalink which runs the UK Faster Payment system and which provides services to real-time payment processors around the world including the TCH in the USA and PromptPay in Thailand; it is also a shareholder in PSP (alongside six Polish banks) which runs Blik, the account-to-account digital wallet in Poland.