Stablecoin to Heaven

The adoption of stablecoins for retail payments

Stablecoins have been established for many years in wholesale payments, almost exclusively for the buying and selling of cryptocurrency on exchanges. More recently, they are being used in retail and small business payments, for more conventional, everyday purposes. Adoption is on the rise.

For a short primer on the key features of stablecoins and how they work, go to the section at the end of this article.

Wholesale Stablecoin Usage

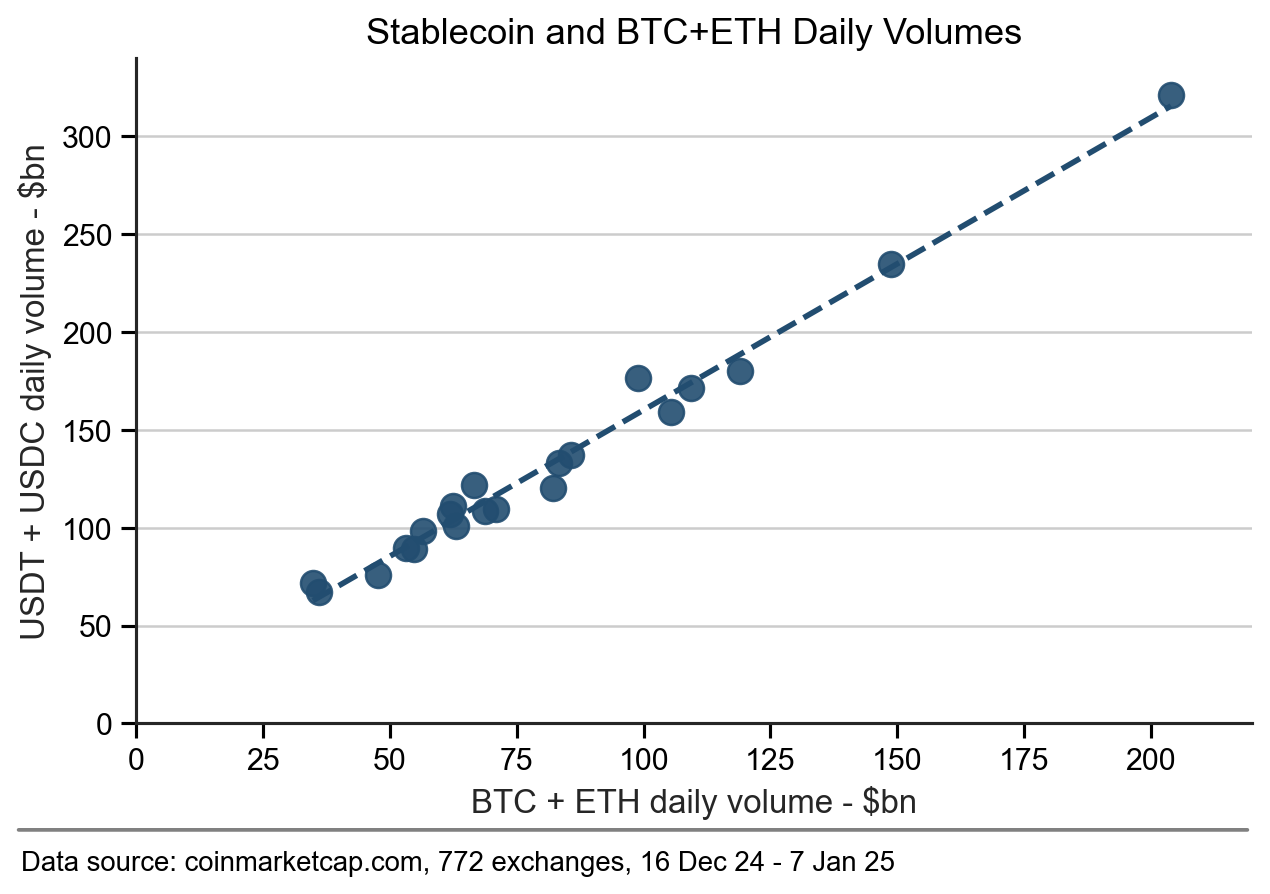

Figure 1 shows a plot of the daily combined traded volumes of the two most popular stablecoins, USDT and USDC against the daily combined traded volumes of Bitcoin (BTC) and Ethereum (ETH), the two most heavily traded cryptocurrencies. The two correlate strongly, illustrating the central role of stablecoins in cryptocurrency trading.

The graph shows for every $100bn traded daily in BTC (66%) and ETH (34%), there are roughly $150bn in USDT (94%) and USDC payments (6%) – the difference is likely due to trading in the thousands of other coins.

Combined USDT and USDC volumes range between $67bn and $321bn per day for the sample shown in Figure 1.

As a comparison, average daily processing values in wholesale payment systems are: Fedwire $4.3trn (USA), Target2 $2.3trn (Eurozone - €2.2trn) and CHAPS $430bn (UK – £344bn).

Figure 1 – Correlation between BTC + ETH and USDT + USDC daily volumes (R^2 = 98%)

Retail Stablecoin Usage

For stablecoin use in retail, London-based (also Tallinn and Gibraltar) treasury solutions company, Orbital produces a very helpful dashboard of retail stablecoin metrics – found here: Orbital Stablecoin Dashboard. Orbital tracks on-chain and exchange activity to identify consumer and business (C2C and C2B) stablecoin payments below $10,000.

The dashboard shows that from virtually no activity in 2019, globally, retail stablecoin payments reached around $200bn in value in December 24 and 126m payments, average value $1,587, with around 24m monthly active users. Table 1 compares the figures for December 2023 and December 2024, showing strong annual growth for each measure.

Table 1 – Retail Stablecoin Usage Metrics (data source: Orbital)

Other interesting retail stablecoin metrics on the Orbital dashboard are:

1. USDT accounts for 90% of payments by volume, USDC 7.6% and cUSD 1.4%.

2. In terms of blockchains, 44% of retail stablecoin payments by transaction volume are made over the Tron blockchain, 35% on the Binance Smart Chain (BSC), 5.6% on Polygon, 3.9% on Solana, 3.4% on Celo, with the remainder on seven other blockchains including Ethereum which supports just 2.4% of retail payments.

3. Over 99% of payments are made with USD-denominated stablecoins, with Euro, Kenyan Shillings and Brazilian Real stablecoins the only other currencies recorded by Orbital.

4. 33% of payments are sent from self-hosted wallets, the rest from accounts hosted on exchanges – including 37% from Binance and 13% from OKX.com.

Retail Uses

Retail uses of stablecoins include:

- Cross-border payments, remittances and FX – C2C and C2B

- Ecommerce and cross-border ecommerce

- Payroll

My own company has used stablecoins for several years to pay overseas developers and designers in USD. We send GBP to our account at an exchange, buy USDC on the exchange and send it to the developer/designer’s wallet which it reaches within seconds. The process takes a few minutes, with immediate settlement in the recipient’s wallet. It is considerably cheaper than using a bank or remittance provider – the exchange gives spot rates (no spread) for GBP/USDC and the transmission fee is less than that charged by UK banks for cross-border payments.

The recipient can be anywhere in the world and has no need for a US bank account – all they require is an internet connection and a USDC wallet. They can choose to hold their USDC on their wallet and transact with it, or sell it on their local exchange for local currency paid into their local bank account. It is fast, convenient and flexible.

The only downside is the UK’s conservative regulatory environment which hinders innovation – consequently, many UK banks prevent payments to exchanges, or limit payments to them, for example a maximum £1,000 per payment and £3,000 total per month. However, such practices are likely to disappear, overwhelmed in time by global growth in stablecoin adoption.

Cross-border ecommerce is another area suited to stablecoins. Digital wallets are easy to integrate into online checkout flows and stablecoin payments for ecommerce are on the rise – Shopify have offered this service1 for over a year and PayPal started offering it last year.

Wholesale uses for stablecoins are also likely to grow outside of trading cryptocurrencies, especially corporates with large cross-border flows. For example, Visa already uses them to settle with merchant acquirers2. Many businesses today, big and small, have overseas suppliers and customers – thus, B2B is also likely to be a major source of growth for stablecoin payments.

Future Stablecoin Adoption

Stablecoins have developed in areas where banks have been unable to provide a quality service or have faced restrictions, especially due to regulation. Stablecoins were borne out of necessity to enable crypto trading at scale, which most banks in most of the world had no appetite for or were prevented from supporting for a long time (if only by uncertainty) – as a result, stablecoins fuelled cryptocurrency adoption, which in turn fuelled stablecoin adoption.

USD stablecoins are now substantial, with at least $189bn in circulation worldwide3. From this position, they will grow following a similar path to before, flowing into the nooks and crannies of the financial system where banks are unable, unwilling or too inefficient to service or improve, for example (generally, but with a few exceptions) in remittances and B2B cross-border payments.

An example is Stripe’s $1.1bn acquisition last year of Bridge, a stablecoin company focused on Africa and Latin America. At the time, one of Stripe’s founders described4 stablecoins as the “room-temperature superconductors for financial services” and announced an intent to build the world’s best stablecoin infrastructure.

Although Stripe have given little away, their intent can be divined – Stripe operates in 46 countries5, but only four in Africa and two in Latin America. To onboard merchants in these continents using its existing cards (and open banking) services, means building banking relationships in multiple new countries and implementing new online card infrastructure with a limited shelf life. With stablecoins, Stripe can avoid this overhead and enter these markets rapidly, leapfrogging legacy technology. Even if the stablecoins are in USD for now, retailers and sellers in these continents will be more than happy to accept USD stablecoins if it is easy to do so and without needing to open a USD bank account, especially if it exposes their online businesses to a global customer base.

Non-USD Stablecoins?

A key question is whether stablecoins will develop at scale in currencies other than USD?

I believe this will take time, as most countries are served well and efficiently by their domestic banks and the need and opportunity for stablecoins for domestic payments are less pronounced. For now, retail and B2B stablecoin growth is likely to be driven by cross-border payments and cross-border ecommerce using USD as a single currency.

One exception is the USA itself - the huge cost of accepting debit and credit card payments in the USA may drive retailers there to accept stablecoins as alternatives to cards, especially given the ready availability and dominance of USD stablecoins.

Stablecoins are a fast-growing, exciting domain in payments – I will provide updates on developments at least every six months, possibly quarterly if the pace of adoption accelerates.

Stay tuned!

___________________________________________________________________________

Stablecoins – A Short Primer

Stablecoins are tokens issued on a blockchain, that are transacted between wallets connected to that blockchain. The value of the tokens is set by pegging them to the value of an underlying asset, such as a fiat currency, or a government bond.

For example, on a blockchain, for every USD-denominated token in issue, or minted, the issuer holds $1 of deposits in a segregated bank account or $1 of short-term government bonds in a custody account.

Trust

For there to be trust in a stablecoin, there needs to be evidence that the total of bank deposits and government bonds held by the issuer equals or exceeds the total value of tokens issued on the blockchain.

Additionally, holders of tokens must also be able to redeem them at any time with the issuer for the equivalent fiat currency.

However, the two largest stablecoins, USDT issued by Tether and USDC issued by Circle have restrictions on who can redeem them. To redeem USDT requires holding an account with Tether and there is a minimum redemption of $100,0006. Circle allows only wholesale providers such as exchanges, institutional traders, wallet providers, banks and large financial institutions to redeem USDC 1:1 for USD7 (and will accept deposits only from these institutions to mint USDC tokens). However, in both cases, individuals unable to redeem their stablecoin tokens directly can sell them on an exchange for USD, for payment into their bank account.

Backing assets

Typically, a stablecoin issuer such as Tether and Circle hold sufficient bank deposits to meet daily operations for issuing and redeeming their stablecoin, with the rest invested in short term government securities. With the yield on three-month US Treasuries currently around 4.3% and $189bn of stablecoins in circulation, the revenue generated by issuers runs into $ billions.

Consequently, issuers are becoming major players in the US Treasuries market. For example, in its most recent reserves report8 Tether holds $96bn in US Treasuries. This is on a par with nation states such as Germany ($87bn) and Mexico ($94bn)9.

The more stablecoins are backed by government bonds, the less risky they are compared to commercial bank deposits. This was illustrated in 2023 when Silicon Valley Bank10 went under with Circle holding $3.3bn on deposit there (8% of its $40bn reserves). Before the bank was bailed out and (exceptionally) all depositors were made good, the price of USDC broke its peg and dropped to as low as $0.87 in the expectation that its $3.3bn deposits would be lost.

Paradoxically, despite negative perceptions in the past, with 1:1 backing by government bonds, stablecoins are potentially a safer form of money than commercial bank deposits – combined with their programmability and flexibility, requiring only an internet connection, this is a key factor in their ongoing success.

Blockchain Security

Security of the blockchain is a critical requirement for stablecoins. Typically, stablecoins use a blockchain such as Ethereum or Solana. Confusingly, these also have their own tokens (ETH and SOL respectively) which have nothing to do with the value of stablecoins. In these examples, smart contracts are used for issuing (minting), transacting and redeeming (burning) stablecoin tokens – in reality, such stablecoins are held on a ledger within a ledger (there may be examples where the stablecoin token is the same as the token native to the blockchain, such as cUSD on Celo, but this seems to be an exception).

The advantage of using a large public ledger such as Ethereum is the security provided by 100s of thousands of nodes validating each transaction. In theory, anyone can create their own blockchain and issue tokens on it, but without a significant number of independent actors validating transactions, the blockchain is likely to get hacked with tokens stolen and double-spent. Public blockchains provide industrial-strength security, enabling cryptocurrencies of all types including fiat-stablecoins to be issued and transacted on them.

Consequently, stablecoins can be issued on multiple blockchains. For example, USDC is issued on 16 different blockchains and USDT on at least 13. However, interoperability between blockchains is complicated, requiring expensive bridging mechanisms – sending, say USDC from an Ethereum wallet to a Polkadot wallet will work only with such a mechanism and the USDC may be lost without one (sending USDT to a USDC wallet, even on the same blockchain is also unlikely to work).

Transaction costs

The cost of a stablecoin transaction is determined by the blockchain protocol, typically a gas fee payable at the time of the transaction in the blockchain’s native token e.g. ETH for Ethereum. Gas fees are usually dynamic, depending on the level of network activity at the time of transaction.

The Orbital dashboard mentioned in the main article, displays a graph of average gas fees for USDT payments (although the data looks incomplete since 19 Nov 24). On 18 Nov 24, these fees ranged from $0.02 per transaction for BSC (the second most used blockchain for retail stablecoin payments) to $5.53 for Tron (the most used). It seems odd that the most used blockchain has the highest fees, but with average retail payment value of $1,587 (see Table 1), fees at this level are evidently acceptable to users.

Note that gas fees are paid by self-custody wallet holders. If payments are sent from an account held on an exchange, the exchange pays the gas fees for its wallet and sets its own fee charged to the sender in addition or instead of gas fees, often at a level far higher than the actual gas fee.

However, for retail stablecoin payments to really take-off, fees need to be reasonable for payments down to $50 or less i.e. no more than say $0.05 (1%) per transaction. Increasingly, fees (and blockchain transaction throughput) will become a battleground between blockchains for stablecoin payments, especially for their adoption for retail payments.

Coinmarketcap.com (as of 8 Jan 25): USDT - $138bn, USDC - $45bn, USDe - $6bn, 193 others (including non-USD and non-fiat backed) - $25bn

Stripe/Bridge: https://x.com/patrickc/status/1848393059559502177

Tether redemption: https://tether.to/ru/redeem-tethers-to-fiat-currency/

Tether reserves: https://tether.to/en/transparency/?tab=reports

Re: Tether reserves.

See note 2 to their report: "Reserves reports are not financial statements but selected financial information extracted from accounting records".