Trapped

The GCash digital wallet in the Philippines and why AML rules needs a rethink

GCash is the leading digital wallet in the Philippines. It claims1 to have been used by 94m Filipinos (population 117m) and is accepted by 6m merchants and social sellers (I assume this to mean micro merchants).

GCash calls itself a super app, although its scope is financial services only, including savings, loans, insurance and investments as well as payments.

I am, of course, interested in its payments capabilities and usage. Across Southeast Asia there are at least 50 such digital wallets with mass domestic adoption, many are driven by e-money issuers rather than by banks.

GCash is a great example.

GCash History

GCash started life in 2004 as a SMS mobile money solution, launched by Globe Telecom, a major telecoms business in the Philippines. Over time, GCash was developed into a mobile payments app and spun out into a separate company, Mynt, now one of the country’s major fintech service providers. Key shareholders of Mynt include Globe Telecom; the Ayala Corporation, a local conglomerate; Ant Group, the owner of Alipay; and MUFG, a Japanese bank. Mynt also has apps for loans (Fuse) and investments (Ryse) and was valued at $5bn in its most recent capital raise in 20242.

Cash and Digital Payments in The Philippines

The Philippines consumer economy is cash-based. A survey3 by Visa in 2024 estimated 87% of transactions were in cash, down from 96% in 2022.

On my recent visit to the country, cash was clearly the dominant form of payment. Hotels, restaurants and shops in malls and airports accepted cards including international cards but outside these, I saw only cash transactions. One taxi driver I used in Manila was aware of Grab and GCash but accepted only cash - he had no knowledge of debit/credit cards and reacted as if he had never seen one.

At a recent conference in Manila4, the central bank presented statistics showing 35% of micro and smaller merchants (MSMEs) use digital payments, up from a very low number several years ago. MSMEs – street vendors, tuk tuk drivers etc make up over 99% of merchants in the country and are a key segment for driving adoption of digital payments.

Using the GCash Wallet

I downloaded a GCash wallet to experience using it as an alternative to cash. I registered it to my phone using a local phone number I had with a temporary SIM I had bought. The wallet gave the option to verify my identity, which I had to decline as I have no Filipino documents. However, the wallet advised I could still use it subject to a cap on the balance of 10,000 PHP (172 USD) and a monthly usage of 5,000 PHP (86 USD), which was fine.

So far, so good.

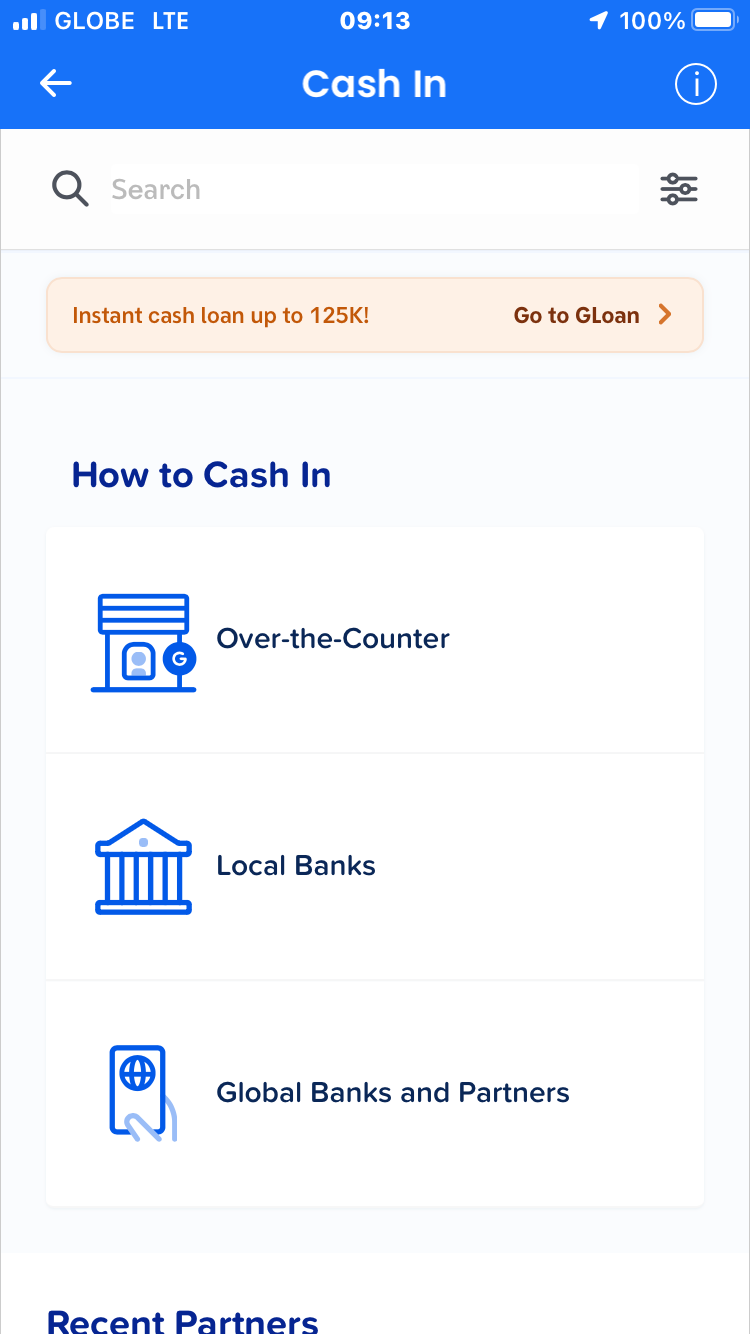

To fund the wallet there are three method types, as shown in Figure 1.

Figure 1 – GCash funding options

I was able only to use the over-the-counter method, by handing over cash to fund the wallet, as I have no local bank account (I was also unable to use my UK bank account for the third option shown in Figure 1).

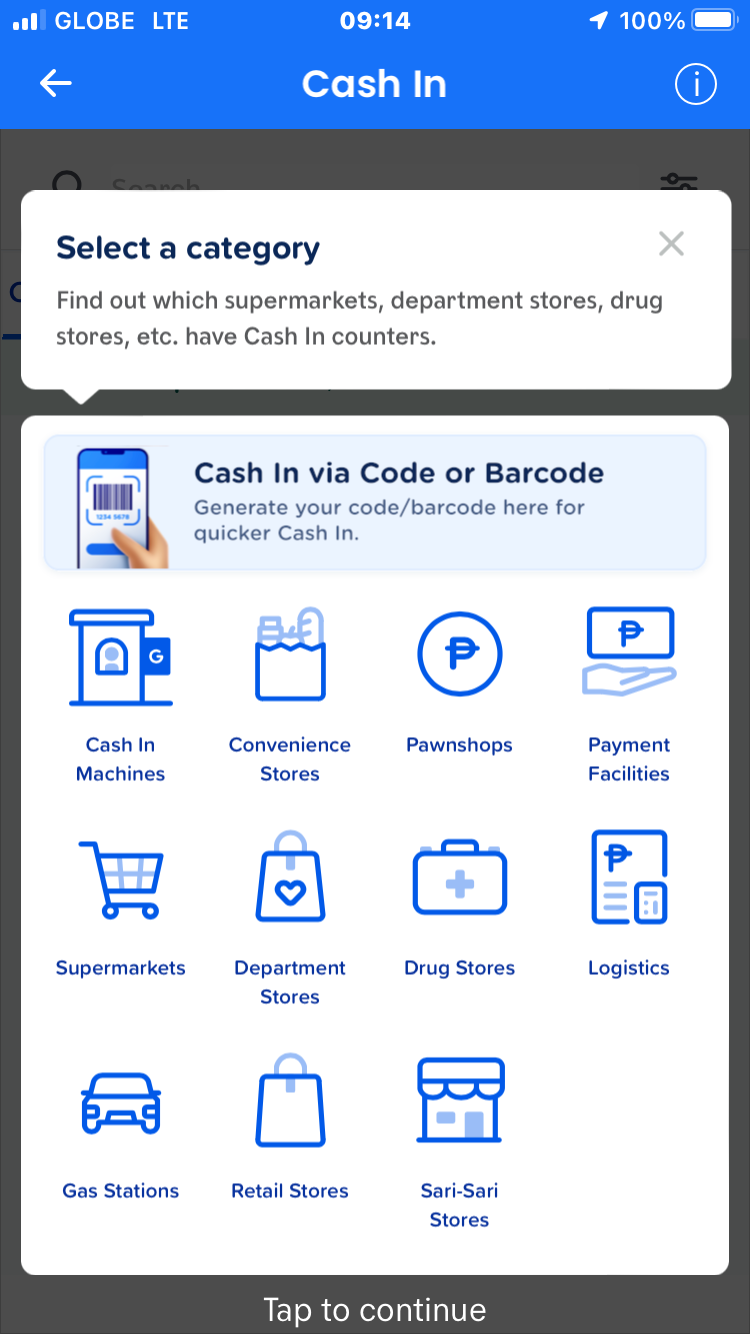

As shown in Figure 2, there are many ways and places to load a GCash wallet using cash, as to be expected in a cash-intensive economy.

Figure 2 – GCash cash-in counter types

I headed to a local store, on the island of Palawan to fund my wallet, similar to the one shown in Figure 3. Many of these stores, known as sari-sari (typically, family-run convenience stores) are GCash agents where they earn commission by funding and defunding GCash wallets using cash.

Figure 3 – A sari-sari store on the island of Palawan that is a GCash agent for cash-in and cash-out

The wallet generated a QR code which I presented to the agent in the store who captured it on her phone and I handed over a 1,000 PHP (17 USD) bank note. The cash was credited immediately and showed on my wallet balance.

However, when I tried to use the wallet to pay for a bottle of water (60 PHP), the transaction was declined and, contrary to the registration information, the wallet requested first I verify my identity – which of course I was unable to do without a Filipino driving licence, the main form of id requested.

So, I was unable to use my GCash wallet and experience it in action. If I had been able to, it would have made paying a lot easier on my travels – ATMs and FX bureau in the country issue mainly 1,000 PHP notes which are too high in value for most cash transactions, whereas 100 PHP and 50 PHP notes are much more practical but in short supply.

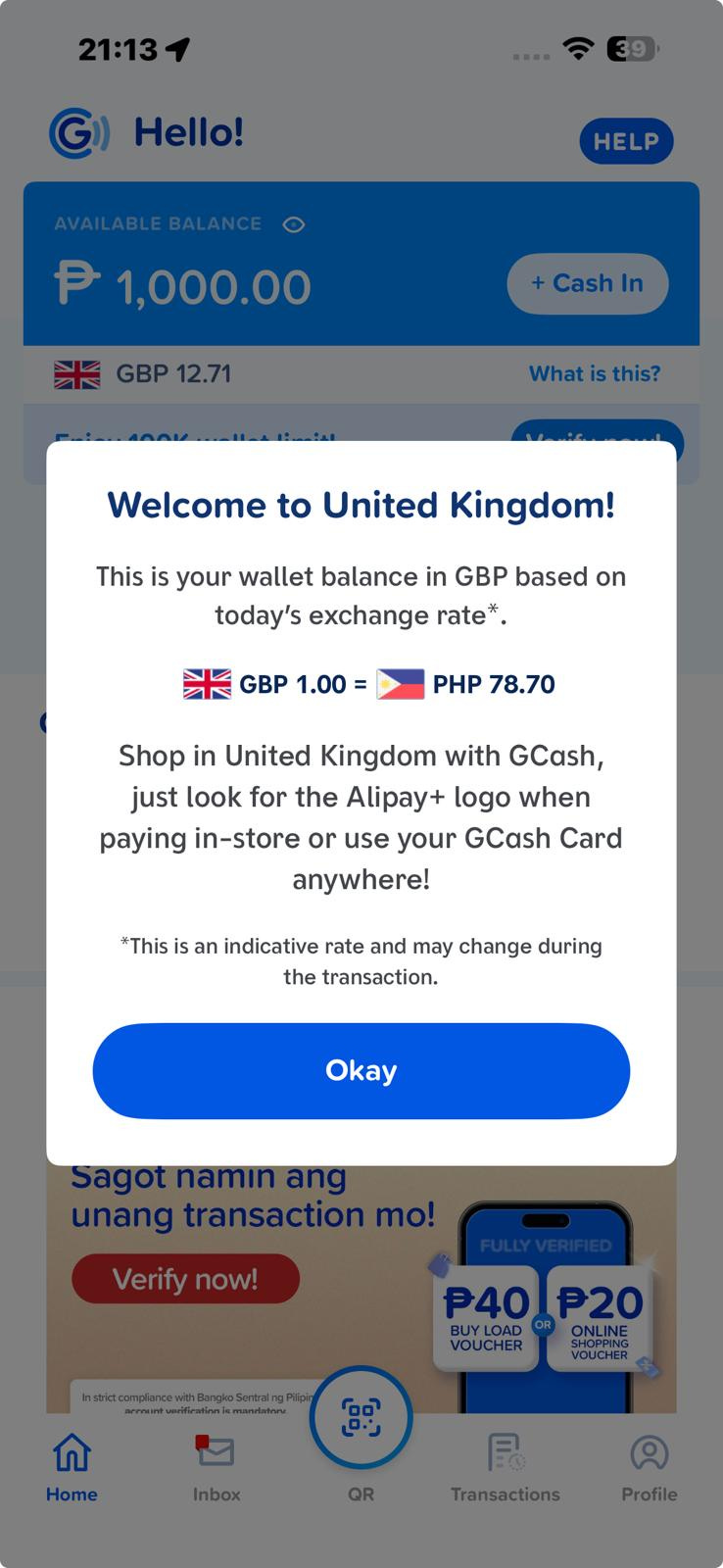

My 1,000 PHP is trapped in my GCash wallet, as shown in Figure 4, presumably forever (especially since my Philippines SIM has expired).

Figure 4 – my GCash wallet with the trapped 1,000 PHP (the screenshot was taken in the UK where I assume the wallet displayed the GBP-equivalent balance because it detected its location)

This requirement to verify my identity is undoubtedly to meet AML/CTF regulations, which, given the mixed messages with the limits in the GCash wallet, have probably been tightened recently in the Philippines.

My experience shows the absurdity of these regulations for low value payments and how they impede consumers and their adoption of digital payments. Whereas a bank note can be used freely and without interference by anyone to make purchases and transfers (as is right and proper), as soon as it is put into a digital wallet it is subject to restrictions – why, for what purpose?5

At the conference I attended recently in Manila, KYC and onboarding complexity were cited as one of five barriers6 to MSMEs and consumers adopting digital wallets – it is easy to see why.

Alipay+

In my article two weeks ago on payments in Singapore7, I observed how visible Alipay+ is in the city with its role in allowing different payment methods from across Southeast Asia to be accepted there. I concluded that Alipay+ is one to watch for cross-border interoperability of domestic payment systems.

This is also evident with GCash which has a partnership with Alipay+. When I opened my wallet in the UK, it advised that GCash is usable in the UK, wherever the Alipay+ logo is displayed, as shown in Figure 5.

Figure 5 – GCash wallets are usable in the UK at merchants displaying the Alipay+ logo

I am unable to find a list of outlets in the UK which accept Alipay+ but I understand they are mainly in London and tourist areas. I had always assumed Alipay+ was targeted at tourists from China but it is clear that its scope is much wider, covering tourists from across Asia and Asians working abroad.

Conclusion

Cash is the most widely used payment method in the Philippines and is likely to remain so for some time. Despite this, digital wallets are used extensively and are accepted by 35% of MSMEs (although I only observed them accept cash). The most popular wallet is GCash, which the majority of the adult population appear to have. However, it is unclear how often GCash wallets are used and no transaction figures are published.

My own attempts to use GCash were thwarted by being unable to verify my account. This highlighted the fact that if digital wallets are allowed to be used anonymously without customer due diligence checks, like cash, for low value transactions and low balances, adoption and usage would be far higher. This would pose little-to-no money laundering risk, as the sums are tiny compared to actual money laundering which runs into trillions of dollars per year (2% - 5% of global GDP according to the UN8).

Still, with tailwinds from government financial inclusion objectives9, a large land mass spread across 7,641 islands with very few bank branches and a large diaspora of Filipinos working around the world who can use GCash locally through Alipay+, GCash looks to have a bright future10.

About GCash: https://gcash.com/about-us

APSCA next generation payments conference, Manila February 2026 - https://www.apsca.org/events/ngp2026/info

Regulators might argue that low balance digital wallets can be used to launder cash into the banking system unless due diligence is done to verify the user. However, it is a spurious argument as the due diligence could be done at the point of transferring funds from digital wallets to the banking system.

The other four barriers are high cost, no immediate value or incentives, low digital literacy and poor connectivity/infrastructure.

UN money laundering estimates https://www.unodc.org/unodc/en/money-laundering/overview.html#.

The whole approach to anti money laundering has been a failure for decades – it is notable that FATF, a non-government organisation that recommends AML rules and practices which most countries adopt, measures how well their recommendations are implemented and their effectiveness rather than how effective they are at preventing money laundering. For example, FATF assesses the UK (https://www.fatf-gafi.org/en/countries/detail/united-kingdom.html) to be compliant or largely compliant on its 40 technical requirements and to be highly effective or substantially effective in the 11 outcomes FATF desires. However, the UK’s NCA estimates money laundering runs at £100bn per year in the UK, yet in 2023/24 there were only four prosecutions and one conviction for it (https://www.spotlightcorruption.org/corruption-and-economic-crime-enforcement-tracker/money-laundering-tracker/).

I am always wary of those promoting financial inclusion. Most assume it to mean pulling the unbanked into the banking system, which is unethical if people are encouraged to borrow to fund consumption (rather than to borrow to build businesses) or are duped into paying fees for banking services. However, if financial inclusion means the ability to send and receive digital payments, with or without a bank account – digital inclusion, as is the case with GCash, I am all for it.

Mynt is planning an IPO for GCash, possibly this year: https://business.inquirer.net/573257/gcash-parent-mynt-keeps-ipo-option-open