The Other Side

Retailer and business demand for payment methods

Historically, payments have been a supply-driven business – banks produced payment instruments such as bank notes, cheques and cards, while consumers and businesses used them in the way banks designed.

Today, payments have become a demand-driven business, with payment providers needing to meet the requirements of their customers – retailers and businesses, rather than the other way round.

Payment methods are core to how businesses get paid and collect funds. Selecting and integrating payment methods has become a strategic consideration for many. Therefore, it is essential for payments practitioners to understand the payment needs of retailers and businesses and the strategic payment decisions they are making.

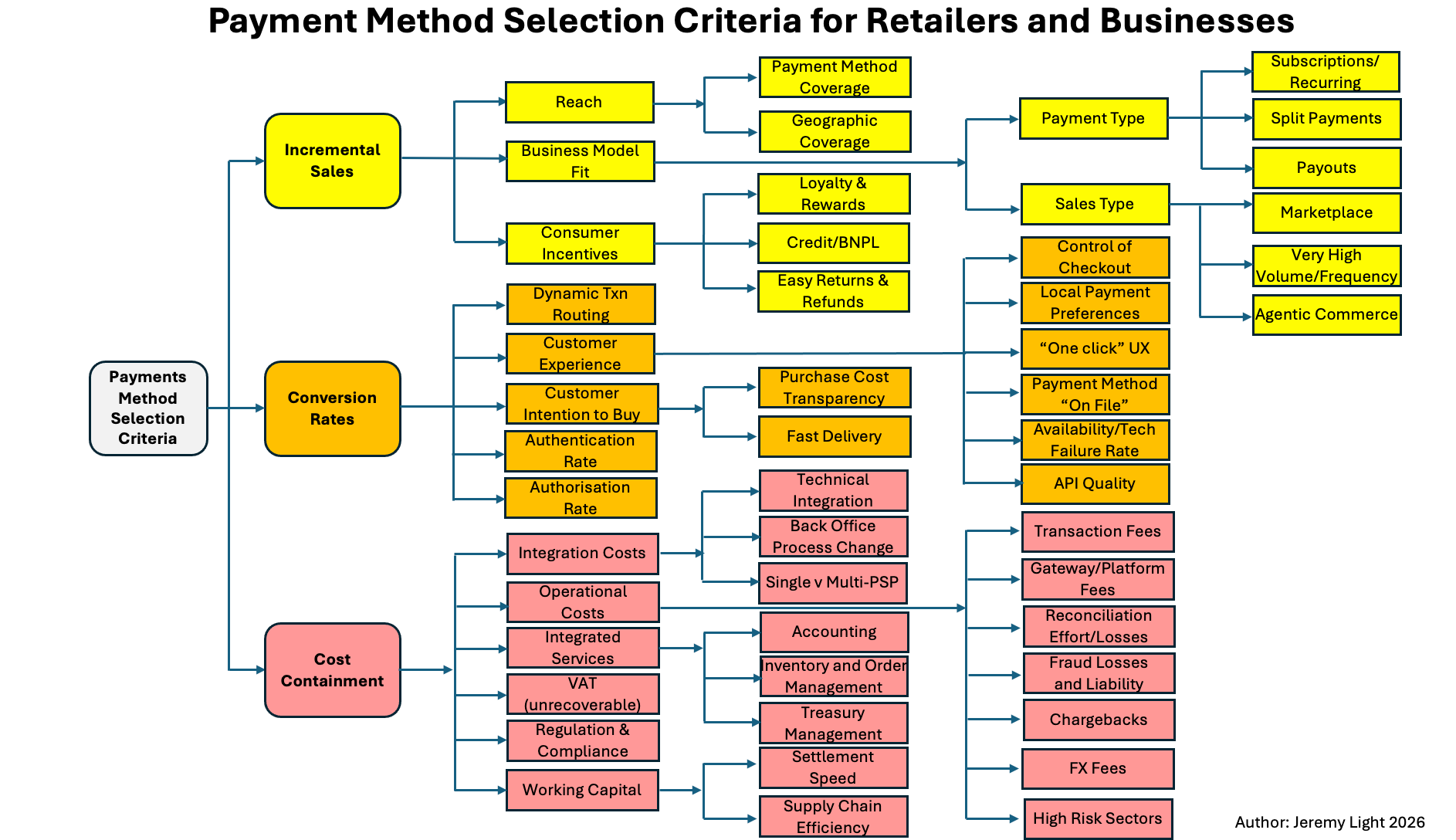

The three key criteria retailers and businesses use when selecting payment methods to offer their customers are, in order of importance:

1. Incremental Sales

2. Conversion Rates

3. Cost Containment

For many retailers and businesses, payments are a multi-variable optimisation problem across sales generation, conversion and the cost of operations and operational fit. This optimisation problem is unique to individual retailers and businesses to solve. Typical criteria they consider are shown in Figure 1.

Figure 1 – typical retailer/business criteria for selecting payment methods

The diagram is illustrative and readers can probably add many other criteria1. However, it serves to show the complexity of the choices for retailers and businesses to get paid and why payment provider and payment method selections are strategic considerations.

Incremental Sales

Obviously, sales are the lifeblood of any business. Sales are complete only once payment is made and anything that makes payment easier or more convenient has the potential to increase sales.

Retailers adopted credit cards at scale in the 1960s and 1970s, boosting sales. Cards allowed consumers to make purchases when they lacked ready cash on their person, especially important for high value items. American Express built its premium cards business on this basis.

Another example is PayPal, which in the early days of ecommerce enabled retailers to sell more online, especially low value items. Instead of a clunky card process, which consumers tolerated for higher value items, PayPal made it easy to pay with just an email address - no 16 digit numbers, CCV codes and no dates to enter.

Retailers picked up PayPal’s APIs and embedded them on their websites as an alternative checkout. Often there was a separate PayPal button placed above the card checkout, or on individual product pages making it very convenient to pay – retailers gained incremental sales and PayPal’s customer base expanded. However, as ecommerce has grown and new payment methods and slick checkouts have appeared, PayPal is less differentiated in enabling incremental sales than it used to be, which may account for its current struggles2.

Another example is contactless cards which cause consumers to spend more than they would with cash3, a key incentive for retailers to accept them.

Today, with a proliferation of payment methods, it is rare for a new payment method on its own to boost incremental sales. BNPL is probably the most recent example. However, the more payment methods a retailer offers and the more relevant they are to the preferences of their target customers, the more sales it is likely to make. The greater the geographic coverage of those methods, again, the more sales – both online (provided the retailer has the necessary distribution capability) and in-store for travellers e.g. retailers anywhere in the world who accept Alipay+’s Silkpay can be paid by over 1.6 billion users using 20+ e-wallets, mainly from across Asia4.

Other factors influencing incremental sales are incentives enabled by the payment method and business model fit, such as subscriptions or support for different sales types such as very high volume/frequency sales for events and concerts.

Conversion Rates

Conversion rate measures how effectively a payment method turns intent into a completed purchase. It is calculated as:

conversion rate % = total successful payments/total payment attempts

There can be many reasons why a payment attempt fails – a card is declined due to insufficient funds, is flagged as fraudulent or the expiry date is past, or the consumer abandons the checkout process due to frustration with the UX, or is unable to receive an OTP or the connection fails.

Retailers pay huge attention to conversion rates, as do payment service providers. The logic is easy to understand - if a conversion rate increases from say 80% to 90%, that is a 12.5% increase in sales just due to the efficacy of the payment method and its role in the checkout process, far outweighing cost considerations such as fees. The reverse is also true when conversion rates decline.

However, I am a little sceptical on reading too much into absolute conversion rates. Whenever I have had a declined payment, I almost always persist with the purchase with another card or payment method – it seems odd to want to buy something then give up entirely i.e. cart abandonments which lower the conversion rate may still lead to a subsequent purchase. Additionally, the buyer’s intent is unknowable. I sometimes go through checkout without buying, just to find out the final price with all extras included, especially for flights and hotels, I expect others do too.

Declines due to positive fraud hits should be excluded from the conversion rate. However, it is impossible for a retailer to identify false positives among issuer declines (although it gets to know about the fraudulent payments the issuer fails to decline). Retailers can see the number of checkouts started and completed but only their PSP/acquirer has metrics on the reasons for failed payments. Even then, for cards, the PSP/acquirer has very little additional information from issuers on their decisions.

Given these unknown factors, conversion rates are best used relatively rather than absolutely. Profitability is sensitive to changes in conversion rate and this is where retailers focus – their objective is to increase the conversion rate they measure without increasing fraud.

However, these unknown factors also mean it is difficult to compare conversion rates meaningfully between different payment methods. The conversion rates of each have different dependencies – card conversion rates are pulled down by failed authentications and authorisations, while open banking rates are pulled down by poor UX (redirects to bank apps). Again, it is the relative difference between conversion rates that is important e.g. if a retailer sees the gap between its higher cards conversion rate and lower open banking rate narrow from say 10% to 7%, that may imply it is getting more repeat customers using open banking.

Generally, overall conversion rates are typically somewhere between 80% - 97%, with account-to-account (A2A) network rates the highest, followed by cards followed by open banking. As an example, in India there are reports5 UPI (an A2A network) achieves 92% - 96% and that the operator guideline for PSPs to achieve is 95%.

There is no standard for measuring conversion rates and there are multiple measures used by different parties, such as payment completion rates, authorisation success rates, session conversion rates. Consequently, it is impossible to make proper apples-to-apples comparisons between rates published by different organisations.

The value in conversion rates lies in how they change over time, experienced and measured by individual retailers and businesses.

Cost Containment

Containing costs is important to any business’s profitability. When analysing payment costs, it is easy to focus on comparing just the fees, usually transaction fees, that different payment methods incur. However, as Figure 1 shows, payment fees are just one cost item among many that need to be managed.

It shows why full stack platform providers such as Adyen and Stripe are popular – one connection gives retailers and businesses access to a multitude of payment methods, ancillary services and geographies. Transaction fees may be higher than connecting directly to a payments network but the total cost of running payment operations may be lower, for both large and small businesses. If the platform provider and its capabilities have a good operational fit with the business and allow it to focus on growing sales and improving conversion rates, while keeping costs contained and predictable, it is a relatively easy decision for the retailer or business to make.

Conclusion

From a retailer’s perspective, payment transactions fees are just one consideration in their adoption of a payment method. More important are how a payment method, or a set of payment methods, generate incremental sales and how they help convert buyer intent into a completed purchase without hindering it.

Consequently, payments is a strategic consideration for many retailers and businesses. Payments are a key factor in optimising sales generation, conversion and costs. Many retailers and businesses solve for this by offering multiple payment methods, often using full stack platform providers. Transaction fees may be higher from these providers but one connection gives access to a choice of payment methods and value-added services.

With open banking and A2A networks on the rise, it is the combination of these payment methods with cards at checkout that are top-of-mind for retailers and businesses. I’ll cover this combination next week and show how sensitive retailer and business profitability is to their adoption and to conversion rates.

Other criteria I have identified but unable to fit on the diagram are: orchestration, device optimisation, scheme fees, scheme rules, time to connect/integrate, discounts at checkout, data entry at checkout, PSD2 / SCA requirements, KYC / AML obligations, lock-in risk, analytics and customer/sales insights

Netherlands survey on contactless spend: https://www.sciencedirect.com/science/article/pii/S0167268124001100

UPI success rates: https://productgrowth.in/insights/fintech/upi-payment-success-rates/ (I am unable to find the source information for the rates quoted nor find NPCI guidelines on them)

Hi Jeremy — author of productgrowth.in and thank you for flagging the missing sources in the post. I've just refreshed the article with april figures and also shared the breakdown of the 92-96% range. Since there are no public numbers available, i study the industry for my clients and that helps create these ballpark figures.

Fully agree with your broader point that conversion-rate comparisons across A2A / cards / open banking are messy without standard definitions.

Appreciated the citation. Cheers :)

Jeremy this may be the first time we don't align completely. The CMOs I've spoken with said uniformly that "increased optinoality [of payment methods] does not equate to increased conversions" in fact the opposite is true. Top conversion priorities amoung the MRC retailers I've spoke with are #1 ShopPay, #2ApplePay and #3Link. Many are actually contemplating taking off PayPal checkout for new customers (making it avail only to past users) due to cost. Just sharing.