Change the Game

Conversion, profitability and removing friction from the checkout process

In my consulting days, while encouraging a major UK high street and online retailer to adopt open banking, I recommended they baseline their payment acceptance costs. I suggested they check acquirer and other PSP invoices for adherence to their negotiated pricing, volume commitments and discounts. The retailer confessed they had never done this, at least within recent memory and a week or so later advised they were unable even to find their contracts!

Today, I expect this retailer and most others are far more diligent and strategic when it comes to payments.

As explained in my previous article1, retailer priorities for selecting payment methods are (or should be) incremental sales, conversion and cost, in that order. Incremental sales are about expanding the target customer base (among other factors), whereas conversion is about converting customer payment attempts into successful purchases. To maximise profitability, retailers have a multi-variable optimisation problem to solve across sales generation, conversion and costs for the payment methods they offer.

This problem is complex. As an example, it may seem, as I suggested last week, that the more payment methods offered, the greater the potential customer base, boosting incremental sales. However, a reader commented that in his experience, uniformly retailers find too many payments methods at checkout to be counterproductive. Some are even considering dropping long established methods such as PayPal for new customers, due to the cost.

This highlights that the combination of payment methods needs to be optimised as well as optimising sales with each method.

Increasingly, this combination is a mixture of card payments in various forms, account-account (A2A) network payments (where available) and open banking.

In this article I focus on the sensitivity of retailer profitability to conversion rates and on the importance of taking friction out of the checkout to improve conversion.

Net Transaction Profits

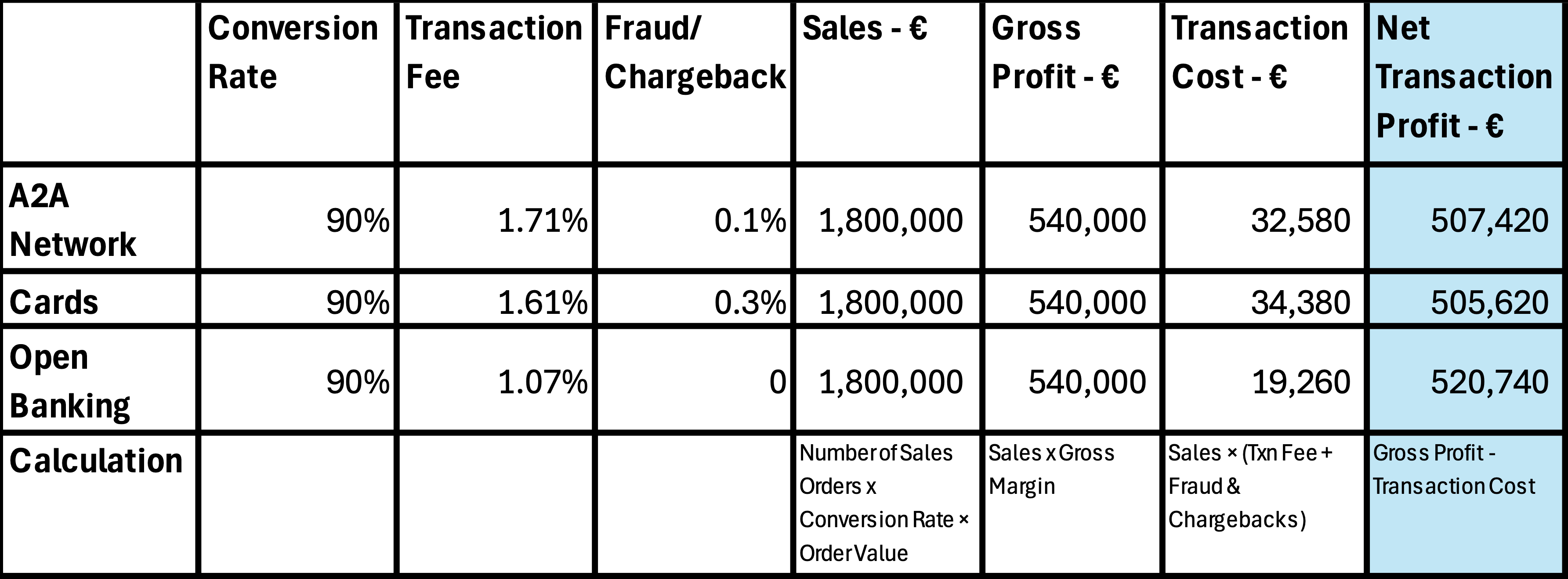

Table 1 shows the transaction profitability of a hypothetical SME retailer, assuming 30% gross margin and 50,000 checkouts averaging €40 per checkout order. The conversion rate of completed purchases to checkouts is set at 90% each, for A2A network payments, cards and open banking.

The average percentage fee rates are those I calculated in a previous article2 from published rates for a €40 payment: 1.71% for A2A networks, 1.61% for cards and 1.07% for open banking. To these I have added fraud/chargeback losses, assuming 0.1% for A2A networks, 0.3% for cards and 0% for open banking (A2A networks have lower fraud than cards due to stronger, in-built authentication and authorisation; there is no chargeback requirement in Europe for open banking3).

Table 1 – SME profitability of different payment methods assuming the same conversion rate (50,000 sales orders at checkout, €40 average sale, 30% gross margin)

Under this scenario, net transaction profit4 is highest for open banking, followed by A2A networks followed by cards. This is as expected, due to open banking having the lowest fee and no chargebacks, resulting in net transaction profit almost 3% higher than cards.

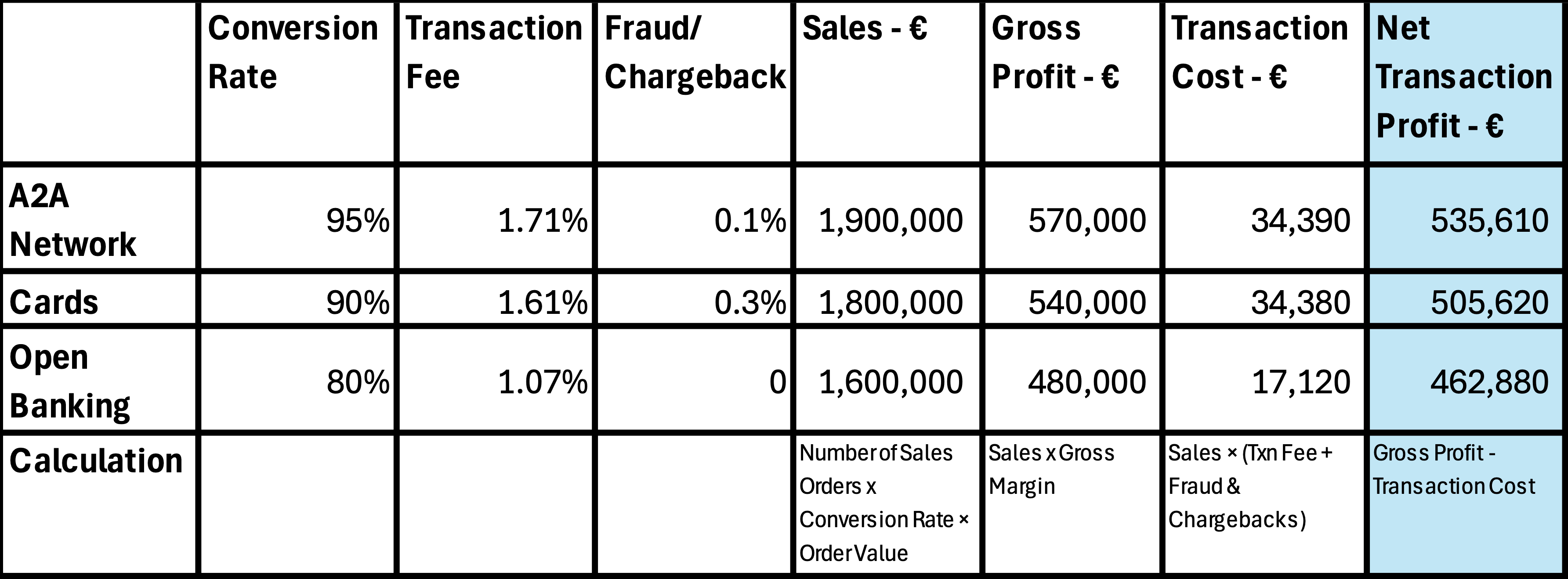

However, conversion rates can differ significantly by payment method. Anecdotally, A2A networks have the best conversion rate, followed by cards, followed by open banking. To show the impact of conversion rates on profitability, Table 2 shows figures for the same hypothetical SME as before, but with conversion rates set at 95% for A2A networks, 90% for cards and 80% for open banking – on the basis that A2A networks have good UX and very secure authentication, cards have OK-to-good UX (depending on whether a wallet/checkout product is used) but relatively weak authentication and open banking has average UX but very secure authentication5.

Table 2 – SME profitability of different payment methods at different conversion rates (50,000 sales orders at checkout, €40 average sale, 30% gross margin)

In this second scenario, the A2A network has the highest net transaction profit, almost 6% higher than cards and open banking has the lowest, over 8% lower than cards.

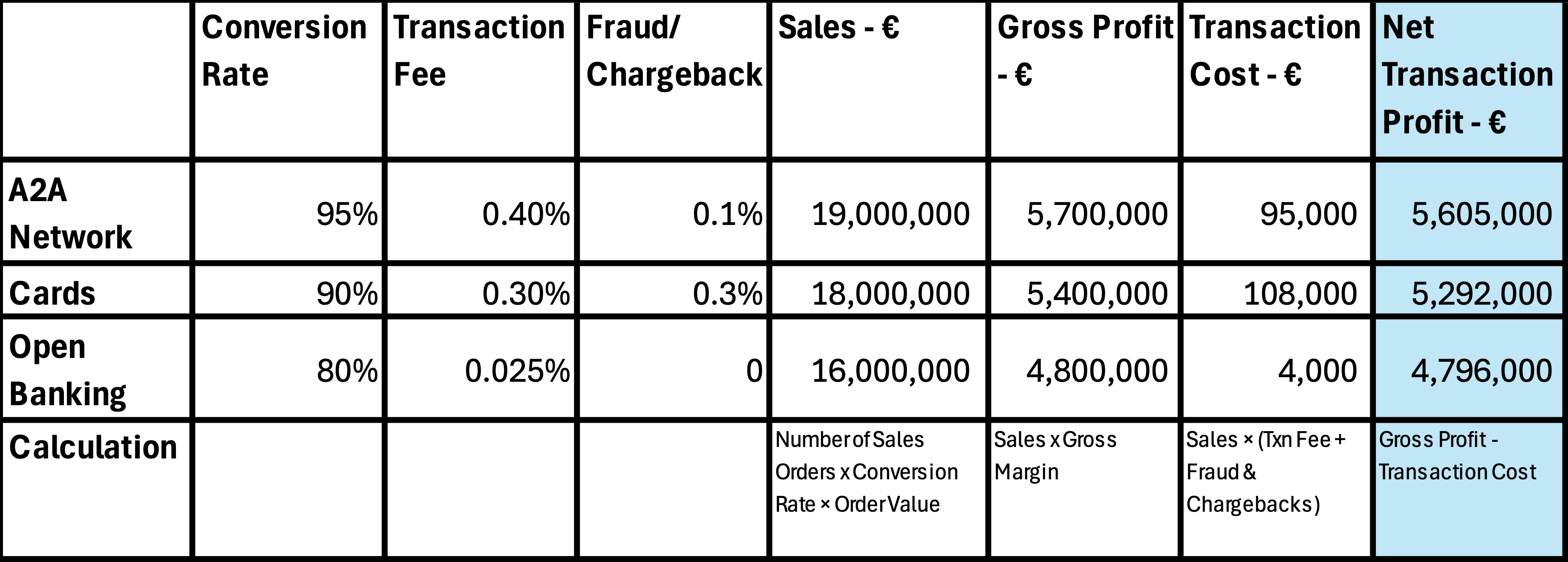

Tables 1 and 2 use fee rates based on published transaction fees (previous article, footnote 2). High volume retailers negotiate much lower fees which are rarely in the public domain, however their profitability is just as sensitive to conversion rates, as shown in Table 3. For this I have used a 0.3% transaction fee for cards (the European regulatory maximum 0.2% debit card interchange + 0.1% margin6), 0.4% for A2A networks and 0.025%7 for open banking. As a high-volume retailer, the total of checkout orders is increased 10x to 500,000 but all other parameters remain the same as for Table 2, including the €40 average sales order.

Table 3 – High-volume retailer profitability of different payment methods at different conversion rates (500,000 sales orders at checkout, €40 average sale, 30% gross margin)

Again, in this third scenario, the A2A network has the highest net transaction profit, 6% higher than cards and open banking has the lowest, over 9% lower than cards even though the open banking transaction cost is far below the others.

These three scenarios illustrate that net transaction profit is more sensitive to conversion rates than to transaction costs. Gross margin on a sale varies by sector in retail but, as in this example, it usually far exceeds transaction fees, so a payment method which enables higher conversion leading to higher sales is generally more important than a payment method with lower fees.

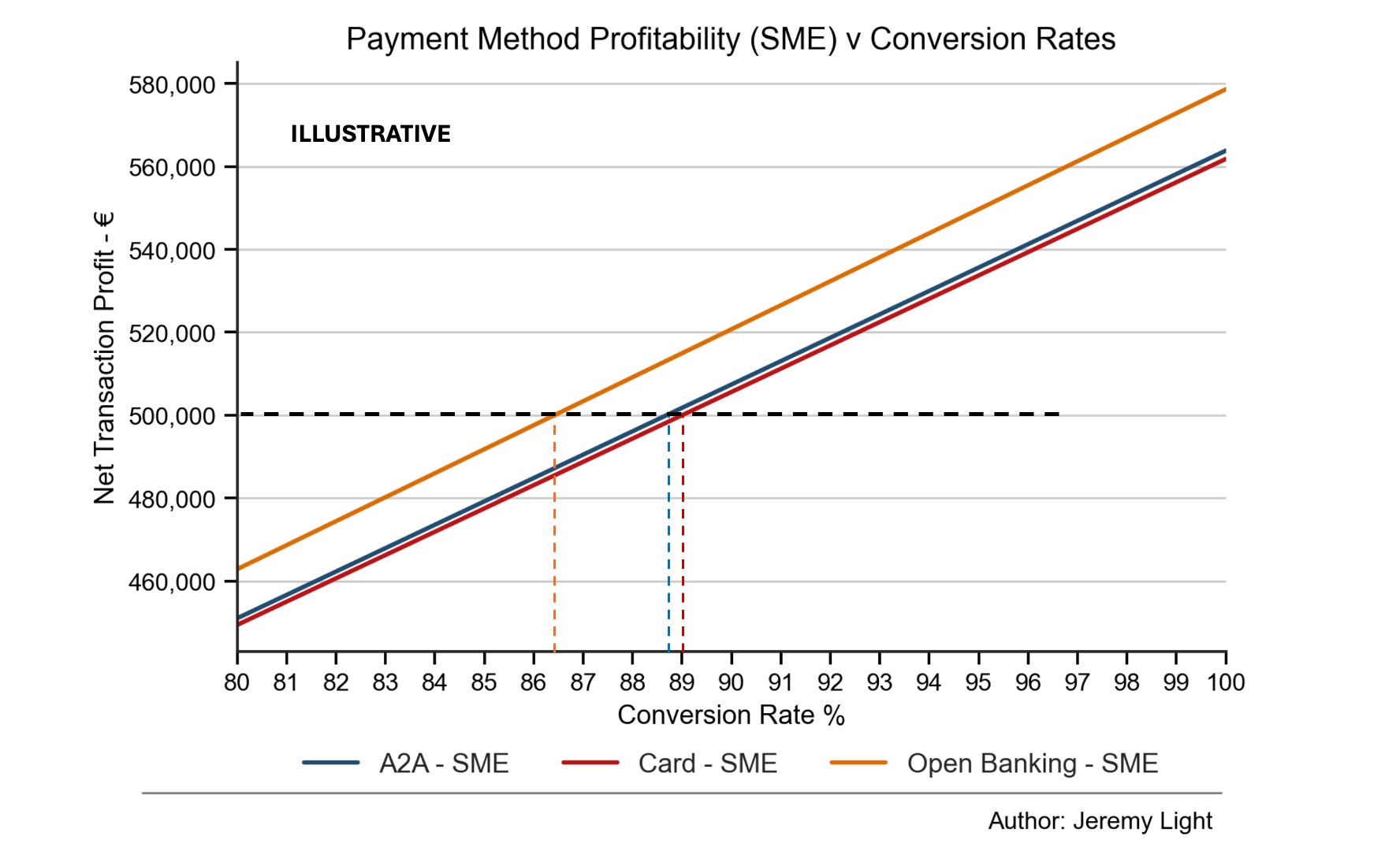

Figure 1 illustrates this sensitivity in a different way. It shows the net transaction profit for each payment method for the hypothetical SME for the spectrum of conversion rates from 80% to 100%.

The graph demonstrates the importance of keeping conversion rates high. It also shows that for a given level of net transaction profit – €500,000 in this case, open banking achieves it with a conversion rate several percentage points below A2A networks and cards. In retail that is an important difference where every percentage point of conversion and every € of profit are hard-won. Open banking configured for high conversion is a very powerful combination - expect to see PISPs make considerable efforts to achieve this.

Figure 1 – SME transaction profitability versus conversion rates

Taking Friction Out of the Checkout

The highest converting checkouts are those with the least friction – both authentication friction and UX friction (typing, screens, redirects, account creation). The choice of too many payment methods can also add friction at checkout, especially on mobiles.

Rewards and loyalty points are powerful incentives for consumers that usually supersede any frustration with a poor UX but where there are no incentives, consumers are likely to choose the payment method with the easiest and fastest checkout. In Europe, rewards and loyalty tend to be on credit cards which account for less than 20% of card payments, so easy checkout is the priority for most retailers.

Based on the reader comment from last week, payments products such as Shop Pay (from Shopify), Link (from Stripe) and Apple Pay/Google Pay/Samsung Pay seem to be winning out. They have in common the ability to accelerate checkout through persistent checkout data, including stored payment credentials. Amazon Pay also has this capability but is less commonly seen, as unlike the others, Amazon is an arch-rival for many retailers. Apple Pay etc have the additional accelerator of biometric authentication (FaceId/TouchId) and they all use card tokenisation to protect the card credentials they store.

Persistent checkout data enables a payment product to recognise and remember the customer details without requiring much, if any effort from the customer. Card-on-file and address-on-file have long been an example of this, making it unnecessary to re-enter card details (except perhaps a CVV code) or delivery addresses. Products such as Shop Pay and Link take this a step further by storing consumer payment and delivery details for use across all the retailers in the Shopify and Stripe networks respectfully and retrieving them automatically on recognising the consumer at checkout through their email address and/or device id.

These products are still very card-centric, leading retailers to optimise for cards. However, retailers need increasingly to consider open banking which is gaining traction. Open banking checkout has higher friction than other methods as it requires bank selection at checkout, a redirect to a bank, followed by the bank’s UX which is outside the retailer’s or its PISP/PSP’s control and often unsuited for a checkout flow.

However, open banking has always had a head start on cards, as it was designed to avoid entry of payment credentials. Its checkout UX is improving and the number of retailers using it is growing e.g. in the UK, eBay and Amazon offer open banking through Truelayer (Pay by Bank). I researched it for this article by using it to buy on eBay. Despite the redirect (which defaulted to my bank – Truelayer appears to be using persistent checkout data), the checkout was slick and quick.

For now, open banking is perhaps best suited for repeat-users and high value purchases. In particular, it is becoming popular with businesses which collect payments to fund accounts, such as bank transfers for pension top ups, stock broking accounts, FX and remittance services, digital asset exchanges and, ironically, credit card issuers for card repayments. With collections, although there is no sale to consider, feedback from PISPs is clear that while open banking’s low transaction costs are attractive to their business customers, take up of open banking is increasing due to improving UX and lower friction.

This bodes well for open banking commercial variable recurring payments (VRPs). These will alter the equation at checkout with a frictionless UX (no redirects except on set up) and very secure authentication. VRPs will also lead to products with persistent checkout data including the consumer bank, consent and delivery details stored by PISPs for invisible use at checkout. The UK should eventually get a VRP scheme and Europe already has one with SPAA. Indications are the UK VRP scheme will have reasonable, fixed transaction pricing making VRP payments cost effective and competitive for payments for any amount, even as low as £5 ($6.65/€5.73).

Very soon, VRP payments will have strategic significance for retailers and businesses.

Conclusion

Payments and their effectiveness in enabling sales are important to retailers and businesses. In the UK, Europe, USA and other Western countries, much of retailer focus has been on optimising card payments with new features, such as persistent checkout data, card tokenisation and biometrics which have appeared in payments products to reduce friction at checkout and improve conversion.

At the same time, those countries with A2A networks – the Netherlands with iDEAL, Poland with Blik, Sweden with Swish, etc have made inroads to cards and have demonstrated that different payment methods can co-exist at scale.

Retailers and businesses need now to optimise the combination of payment methods they offer, including open banking and, where available, A2A networks, as well as cards. Cost is a factor between the different payment types but far more important are their conversion rates, driven higher by lower friction UX and lower friction authentication.

With different uses and conversion rates for different payment methods, retailers and businesses need a multi-acceptance strategy and they need to optimise transaction volume across each payment method offered to maximise total profit.

Almost a decade after I first started to engage with retailers on open banking, open banking is still finding its feet. However, with VRPs, open banking may change the game entirely at checkout and with it, the optimal combination of payments made available to consumers.

Never has it been more important for retailers and businesses to treat payments strategically than it is today.

Previous article on retailer payments: https://jeremylight.substack.com/p/the-other-side?r=axqgy

Article on the fees retailers pay in Europe: https://jeremylight.substack.com/p/the-price-you-pay?r=axqgy

According to the UK’s Open Banking Ltd, open banking fraud is 0.013% by volume, which reduces to 0.0034% when APP fraud is excluded (APP fraud comes from scammers and is irrelevant to legitimate retailers). UK Finance reports that overall card fraud is 0.06% by value, 18 times higher than open banking (assuming the card fraud rate by volume rate is similar to that by value). Therefore, open banking has little need for a chargeback mechanism, unlike cards. OBL: https://www.openbanking.org.uk/insights/financial-crime-in-open-banking-2025-update/ UK Finance: https://www.ukfinance.org.uk/system/files/2025-05/UK%20Finance%20Annual%20Fraud%20report%202025.pdf

The SME’s full net profitability requires deduction of other non-transaction costs – administration, property etc which are independent of the payment method, so net transaction profitability is a reasonable metric to compare payment methods here.

In Europe, secure customer authentication (SCA) applies – cards use 3DS to meet this SCA requirement, whereas for A2A networks and open banking SCA is embedded/native to the banking flow and inherent in the bank app authentication. For cards, SCA is a bolt-on and using 3DS means authentication and authorisation go through three independent filters – acquirer, network (Visa etc) and the issuer, which share little of their own analysis with each other, increasing the chance of a false decline and decreasing the conversion rate. For practical reasons some card transactions are exempt from 3DS, further impacting the effectiveness of card authentication/authorisations.

As this is an illustration, for simplicity I have ignored credit cards (they have a regulatory maximum interchange of 0.3% in Europe but account for less than 20% of card transactions).

In discussions with several PISPs I understand that high volume retailers can pay as little as 1€c per transaction, equating to 0.025% on a €40 payment.

Jeremy,

Nice post. What would a cash payment look like using these criteria?

John