Against the Grain

The slow adoption of real-time payments in North America

It is a year since I analysed real-time payments in Canada and the USA1.

As expected, progress has been slow, although a trend is emerging in business payments.

To recap, Canada has no interbank real-time payments system, although Payments Canada’s Real-Time Rail (RTR), over a decade in the making, is scheduled finally to launch in Q4 this year2. The only source of true real-time payments at the moment in the country is PayPal.

The USA is in a better position with FedNow, PayPal, TCH’s RTP, Venmo (owned by PayPal) and Zelle (there are others such as CashApp but no real-time payment volume data is available, indicating usage is likely to be low).

My preferred metric for comparing adoption of real-time payments3 by countries and over time is real-time payments per capita (PPC). It is calculated simply by dividing the total annual volume4 of real-time payments for a country by the current population size.

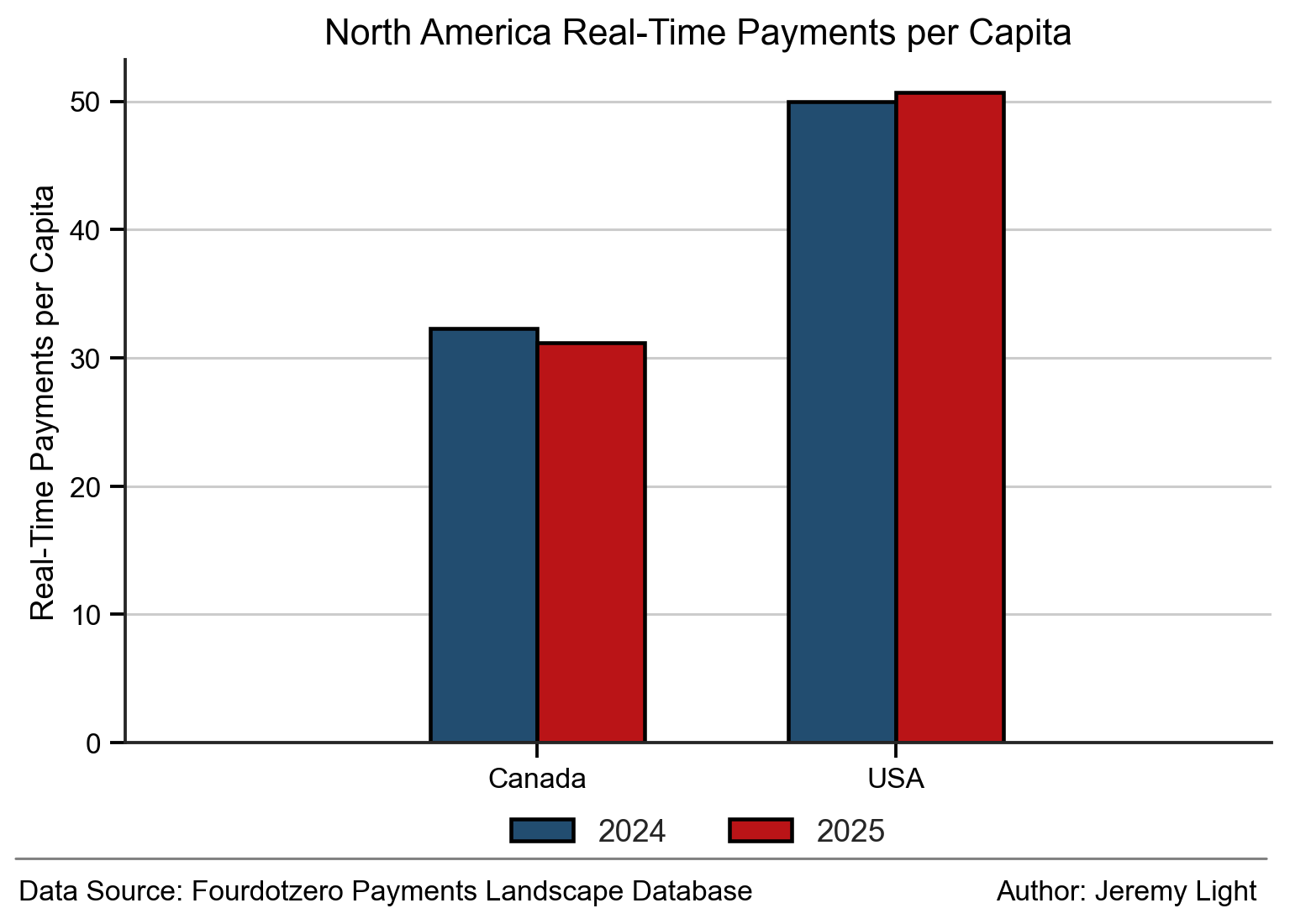

On this measure, PPC barely moved in North America in 2025 – see Figure 1.

Figure 1 – Progress of real-time payments adoption in North America

The average for North America as a whole in 2025 was 49 real-time PPC, a tiny increase over 48 in 2024. This is far below countries such as Brazil (373) and Kenya (791). The almost static state of North America’s real-time PPC between 2024 and 2025 is also in stark contrast to the growth of the leading adopters – for example, Brazil’s real-time PPC grew 25% in 2025 and Kenya’s 29%.

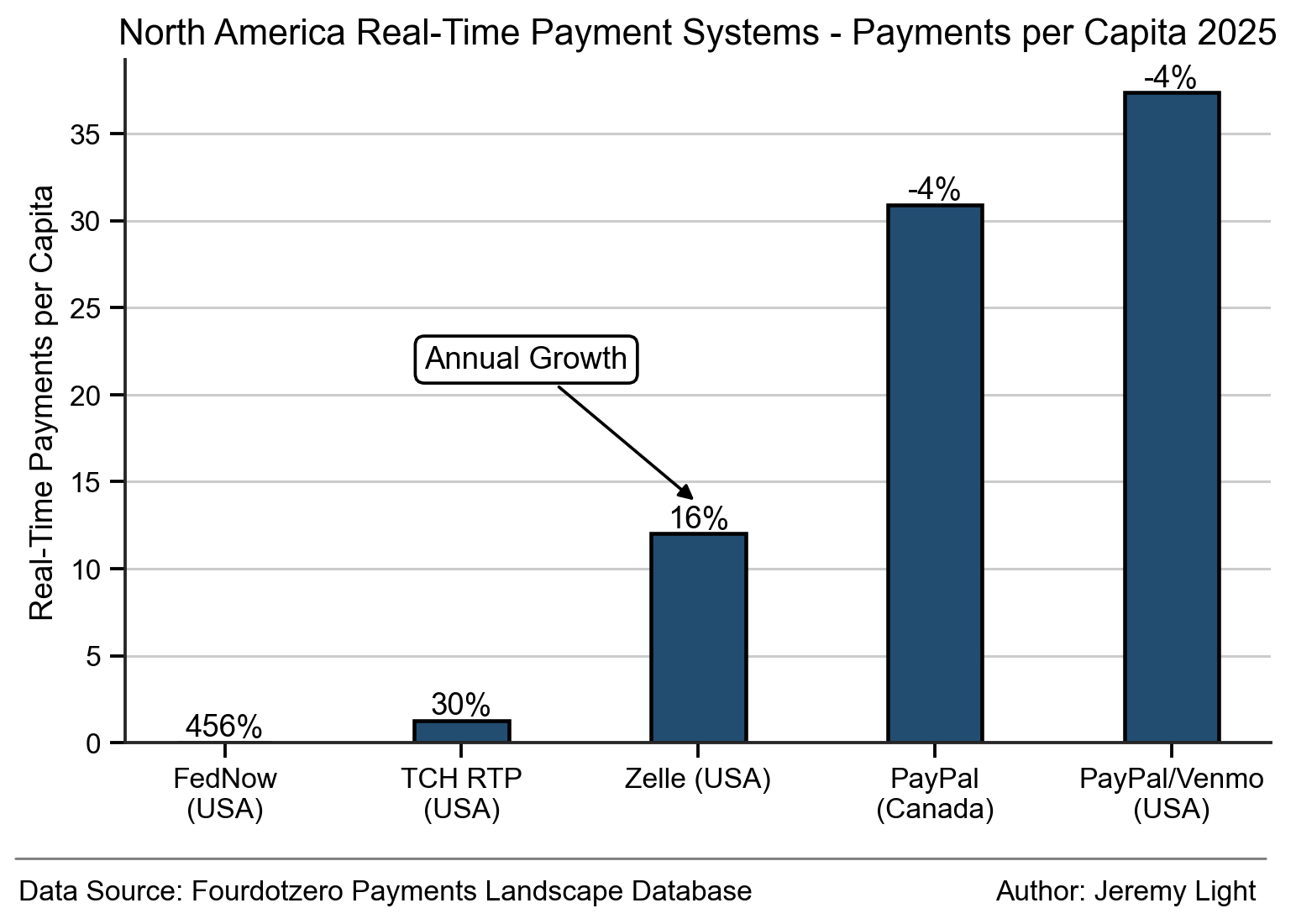

However, apart from PayPal, the underlying payment systems paint a more dynamic picture.

Figure 2 shows the real-time PPC for each payment system, together with their 2025 growth rates. PayPal dominates North America’s real-time payments but reported5 a 4% decrease in transactions in 2025 (PayPal provides no volume breakdown by country and I have estimated the proportion of payments attributed to Canada (1.3bn in 2025) and the USA (13bn) and assumed volume decrease in line with the global total).

Zelle has the next largest volume, although at 4.6bn payments in 2025, is far smaller than PayPal. Zelle volumes grew 16%6, TCH RTP grew 30% and FedNow grew 456% from a low base (it is still in the initial adoption phase having launched in July 2023).

Figure 2 – Progress of adoption in North America’s real-time payment systems

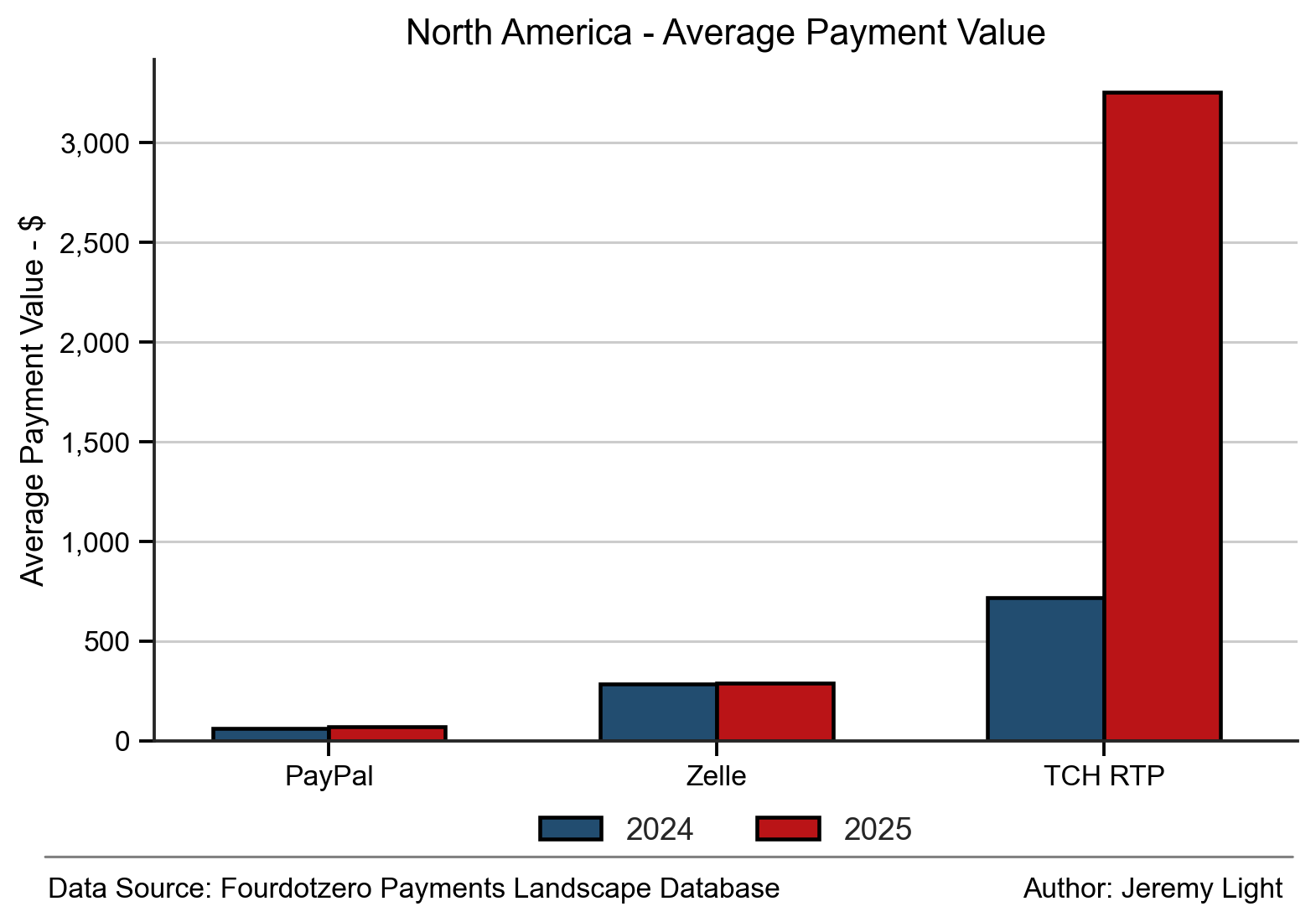

The key driver of growth in FedNow, TCH RTP and Zelle appears to be business payments. The average FedNow payment was $101k in 20257, which aside from consumer property purchases, indicates commercial and wholesale use.

TCH RTP raised its transaction limit to $10m last year and its average payment value shot up from $718 in 2024 to $3,254 in 2025, indicating a swing to commercial and wholesale use.

Zelle is used by 7.7m small businesses, whose transaction volume grew 24% in 2025, faster than Zelle’s 16% overall growth rate. Small business payments account for about 14% of the total (footnote 6).

Figure 2 shows the average real-time payment values, excluding FedNow (which at $101k would distort the scale).

Figure 3 – Average payment values in North America’s real-time payment systems

Conclusion

Banks in Canada and the USA have an iron grip on the direction of payments in North America. They have an enormous cash cow to defend in the form of their cards businesses. This is likely the reason why the slow adoption and small scale of real-time payments in the region are so divergent from elsewhere in the world. Canada is finally launching RTR later this year, a decade after it was first proposed but contrast that to Brazil. It took less than two years to scope, build and launch the highly successful Pix real-time interbank payments system.

North American banks are in no rush to adopt real-time payments at scale.

However, real-time payments are showing signs of growth for commercial and wholesale use even if growth for consumer and retail use, the sweet spot for cards, is sluggish.

This raises an interesting question on the current appetite in the USA for stablecoins. These transact in real-time and adoption of stablecoins at scale means adoption of real-time payments at scale. This seems at odds with the current trend. Additionally, in 2025, the total value of real-time payments across the US systems in Figure 2 was $4.6trn. This level of activity would require just $25bn - $30bn of circulating stablecoins (based on historical stablecoin volume and market cap data), less than 10% of all stablecoins today and a drop in the ocean of dollar liquidity in North America.

This suggests stablecoins in North America are destined for the commercial and wholesale sector, which is also where real-time payments activity is increasing.

How long the consumer and retail sector in the region can hold out and continue against the grain of rapid worldwide real-time payments adoption, remains to be seen.

June 2025 article on real-time payments in North America: https://jeremylight.substack.com/p/its-a-matter-of-time

Real-Time Rail Canada: https://www.payments.ca/systems-services/payment-systems/real-time-rail-payment-system

I define real-time payments to be transactions which result in the real-time transfer of funds from sender to receiver with immediate availability of funds in the receiver’s account. This includes bank account payments and non-bank stored value account payments (e.g. PayPal). It excludes cards and for now, ignores digital assets and stablecoins.

I use volume rather than value as it is indicative of adoption and usage (“every transaction is an interaction”). Dollar value comparisons are less useful, except for high value payment systems and RTGSs. Dollar value comparisons are also more complicated, requiring FX calculations and inflation adjustments.