Africa

Africa's world class sovereign payment systems and infrastructure

A year ago I covered real-time account-to-account (A2A) payments in Africa, showing how countries in the continent have payment systems that are among the best in the world1.

In this article I provide an update on developments since then and real-time payments growth in 2025.

Africa’s Four Payments Pillars

To recap, there are four pillars to real-time payments in Africa:

1. Mobile-money services provided by telcos e.g. M-PESA in Kenya

2. Real-time interbank clearing e.g. PayShap in South Africa

3. Interoperable real-time interbank clearing and mobile money e.g. TIPS in Tanzania

4. Cross-border real-time clearing e.g. GIMAC in the CEMAC region (a region of six countries in central Africa which share the same currency, the CFA franc).

Mobile-money is dominated by telcos such as Airtel, MTN, Orange and Safaricom but there are at least 60 such services across Africa’s 54 countries.

Real-time interbank clearing is available in 35 countries2.

Developments Over the Past 12 Months

The big theme I highlighted and explained last year continues – connectivity.

Connectivity between telcos and interbank clearing, within and across Africa’s borders. Leading to wallet-to-wallet, wallet-to-bank, bank-to-wallet and bank-to-bank real-time payments.

The expansion of real-time A2A interbank payment systems also continues. Notable developments in the past year are:

1. Algeria – launch of QR code payments on the Baridi Pay app (14 Jun 25).3

2. West Africa – launch of the PI-SPI regional instant payment platform (30 Sep 25) by BCEAO (Central Bank of West African States).4

3. The Gambia – launch of BANTABA 2.0, the interoperable version of the existing real-time payments system, connecting banks, telcos, microfinance institutions, fintechs and payment service providers (15 Dec 25).5

4. Ethiopia – launch of the EthioPay instant payments platform (19 Dec 25).6

5. Kenya – partnership between the Pesalink instant payments system and the Pan-African Payment and Settlement System (PAPSS) for cross-border payments within Africa and for regional financial integration (26 Feb 26).7

6. Mozambique – launch of the METIX instant payment system, interoperable with banks and telcos (16 Mar 26).8

7. Burundi – launch of the BurundiPay instant payment system, interoperable with banks and telcos (23 Apr 26).9

Mobile Money

The GSMA provides an annual report on mobile-money services which is worth a read10. It states that in 2025, global mobile money transaction volumes were 125bn, a 16% increase on 2024 (108bn). Africa accounts for the majority of these, 92bn, 74% of the world’s total, also a 16% increase on 2024. Active (30-day) accounts were 341m, a 19% increase on 2024.

Mobile money transactions include cash-in and cash-out transactions for the deposit and withdrawal of cash from agents. I estimate from telco and country data, that cash-in/out transactions account for 15% - 20% of mobile money transactions, resulting in perhaps 76bn – 78bn mobile money payments across Africa. Almost all these are real-time, A2A payments and most are likely to be between wallets.

However, it is difficult to reconcile the GSMA’s figures exactly with the mobile money volumes aggregated bottom up published by individual countries. I have taken mobile money figures from central banks and telcos in 13 countries, with a combined population of 743bn, which total 110bn payments. M-PESA alone, in Kenya (population 59m) processed 44bn payments in 202511.

The key message is that mobile money payments have been adopted at scale across Africa and dominate the payments landscape, while continuing to grow at 15%+ annually.

Real-time Interbank Payments

The volume of real-time interbank A2A payments are much lower than mobile money payments – many more Africans have mobile phones (mainly feature phones which use USSD technology for mobile money transaction) than have bank accounts.

I have researched instant payments data for ten countries in Africa with a combined population of 567m people. In aggregate, these countries account for 15bn instant A2A payments, 12% of the total, although this figure is skewed heavily by Nigeria’s NIPSS system with 13bn payments12 in 2025.

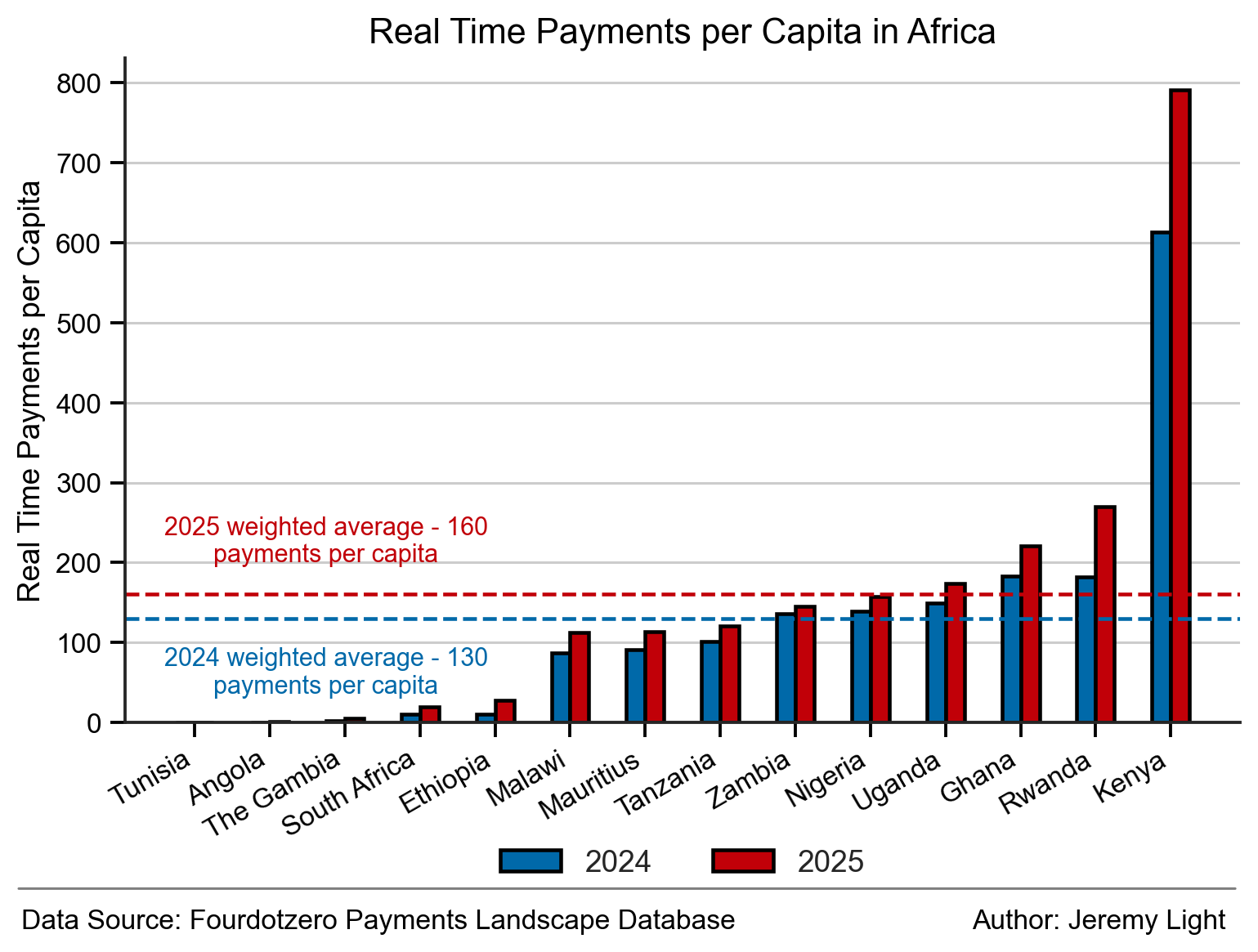

Real-time Payments per Capita

Combining mobile money and interbank A2A real-time payments for 14 countries, last year I estimated the real-time payments per capita (PPC) across these countries averaged 119 in 2024. Through updates and refinement of the data, I have revised this 2024 figure upwards to 130. For 2025, I have calculated it to be 160, a 24% increase.

Figure 1 shows the real-time PPC for 14 countries (with a combined population of 783bn, 2.2% higher than 2024) which have published volume data. Kenya at 791 real-time PPC has the highest by far, a 29% increase on 2024. Second is Rwanda, at 270 real-time PPC which has beaten Ghana into third place, at 221 PPC

Figure 1 - Real-time payments per capita in 14 countries in Africa, including on-us bank payments, interbank payments and mobile money payments

The total universe of real-time A2A payments covered by the countries in Figure 1 is 126bn payments. This is a 26% increase over 2024. Some countries are growing at much higher rates, in particular Angola, Ethiopia, The Gambia and Tunisia.

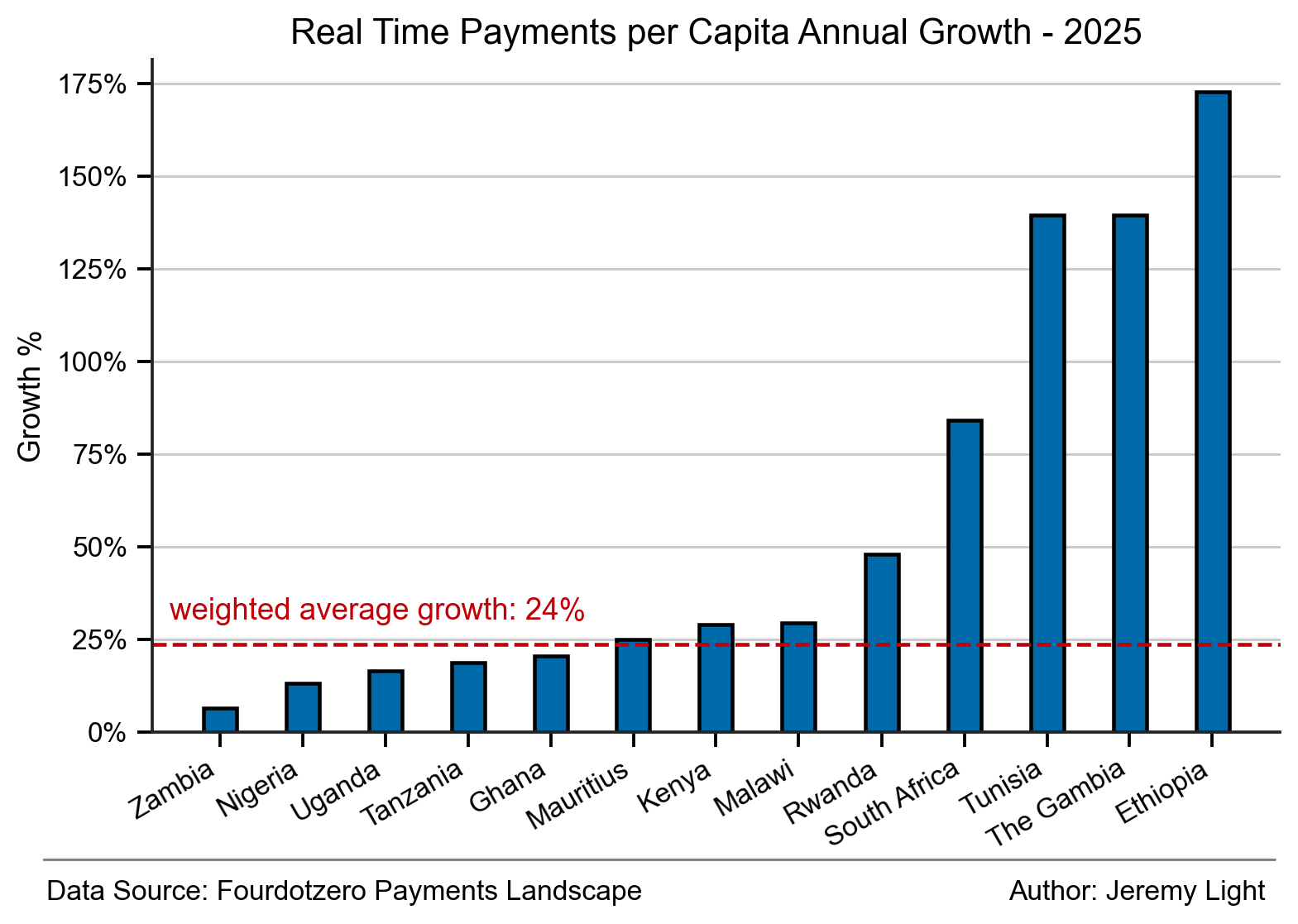

Figure 2 shows the real-time PPC growth rates for the 14 countries, excluding Angola (for clarity - its real-time PPC grew over 1,000% from a very low base in 2024 and was still only 1 PPC in 2025).

Figure 2 - Real-time payments per capita growth in Africa (Angola excluded from graph – 1076%)

Figure 2 illustrates the capacity for real-time payments growth in Africa, with even Kenya, already the largest real-time PPC by far, growing volume at 31% (PPC 29%) a full 18 years after M-PESA launched.

Conclusion

It is easy to think that mobile money is an African solution to meet the needs of relatively low income, cash-intensive economies with poor infrastructure and that it is of marginal relevance to the rest of the world.

That may have been the case a decade or more ago but today, mobile money is the backbone of digital payments systems that are thriving across Africa and driving world-leading payment innovation. Interoperability is increasing between mobile money services and with the growing number of real-time interbank payment systems. This is leading to the emergence of a highly connected and resilient payment system across Africa.

The payments landscape in Africa is uniquely African and sovereign to Africa – built for African countries, by Africans and by African companies. It is fast becoming as advanced as any in the world and its highly connected, wallet-to-wallet/wallet-to-bank architecture is likely to be replicated in many future payments systems across the world. Anecdotally, Africa is also becoming a leader in stablecoins for consumer use - expect to see these develop along with interoperable digital wallets across the continent.

Last year I observed that the future of real-time A2A payments, bank and mobile money, in Africa looked very bright. A year on, it is looking even brighter. The volumes in almost all the 14 countries in Figure 1 are growing strongly – if they matched the real-time PPC of Kenya, an extra 500bn annual digital payments would be generated, a five X increase.

It is only a matter of time.

Momentum in real-time payments in Africa: https://jeremylight.substack.com/p/nothings-gonna-stop-us-now

Although I believe Sudan’s EBS real-time clearing system is switched off currently.

GSMA The State of the Industry Report on Mobile Money 2026: https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/wp-content/uploads/2026/04/The-State-of-the-Industry-Report-2026_English.pdf

Calculated by prorating across Safaricom’s FY25 and FY26 figures: https://www.safaricom.co.ke/images/Downloads/FY26-Investor-Presentation-7TH-May-2026.pdf

I used a 15.5% growth over 2024 volume to estimate NIBSS 2025 volume: https://nibss-plc.com.ng/nigerias-payment-revolution-how-nibss-cbn-are-building-africas-most-robust-digital-infrastructure

Thank you for the article! FYI - USSD not USDD